Oil’s Dividends May Not Withstand Covid and Climate

(Bloomberg Opinion) -- An oil major’s dividend is its solemn pledge that it will deliver no matter the vagaries of the market. But no one planned on those vagaries including negative oil prices. So can Big Oil maintain its dividends? Should it?

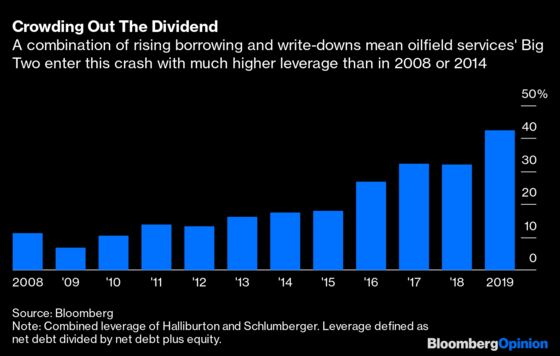

As so often in this business, oilfield services provide early warning. Announcing quarterly earnings, Schlumberger Ltd. slashed its dividend by 75%, its first cut in at least four decades or so. The stock actually jumped 9% that day. Meanwhile, Halliburton Co. held off cutting but also made it clear it would have no qualms doing so if necessary. Its stock didn’t jump, but did close in the green despite oil closing with a minus sign in front of it that day.

Those positive reactions may have had something to do with this:

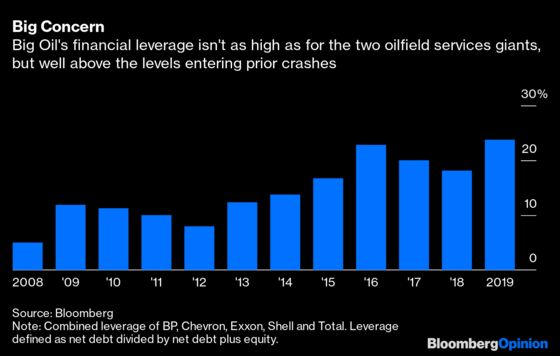

Aggregate indebtedness at the big five Western oil majors — BP Plc, Chevron Corp., Exxon Mobil Corp., Royal Dutch Shell Plc and Total SA — has also jumped since 2014. And as a group, they only just covered capital expenditure and dividends from operating cash flow in 2019, when Brent crude oil averaged $64 a barrel. So while they aren’t quite in the same boat as the services firms, they’re getting uncomfortable.

More importantly, investors have gotten uncomfortable already.

There is a strong case to be made that having a progressive dividend in such an inherently volatile business as oil is asking for trouble. Big Mining acknowledged as much back in 2016, when BHP Billiton Plc, for example, switched away from progressive dividends to tying its payouts to a percentage of (fluctuating) profits.

A dividend that erodes the balance sheet, thereby raising the risk premium, stops being a down-payment on value and ultimately becomes a drag on it. Put another way, above a certain level, dividend yields indicate the market isn’t paying up for promises of more — so maybe just stop promising.

Oil majors have ridden out prior downturns, usually leaving dividends untouched, through a mixture of borrowing, selling assets and cutting costs. But the seams have split at various points. BP temporarily suspended dividends after the Deepwater Horizon disaster (a decade ago this month), and both Royal Dutch Shell and Total instituted scrip dividend programs — whereby investors take new stock rather than cash — in the previous oil crash. Shell’s annual dividend per share, meanwhile, has been flat since 2014, the last year of triple-digit oil prices.

Moreover, the implacable issue of climate change stokes expectations of peak demand, making promises of ever-rising dividends look even more incongruous. So why not use the shock value of negative oil prices to reset dividend policy?

Psychology is a big factor. The dividend is a fixed point to cling to in a changing world. It’a also the last bond of trust between the sector and investors. Big Oil’s capex boom saw capital employed for the big five jumping by half even as earnings dropped by almost half over the past decade, trashing returns.

Viewed in that light, the dividend is an insurance policy against doing stupid stuff. “Dividends and debt prevent undisciplined companies from being more undisciplined,” says Doug Terreson, oil analyst at Evercore ISI. If management doesn’t have a loose billion or so lying around, they’re less likely to blow it on an ill-timed acquisition or mega-project. “The bottom line is that it’s not that dividends are too high for Big Oil, it’s capital discipline that is too low,” Terreson adds.

As it is, consensus forecasts for 2020 have the five majors generating almost $29 billion of free cash flow. That factors in big cuts to capex budgets already, yet would cover barely half of last year’s dividend payments. Sure, this is a plague year. But the damage done to the global economy and the glut of barrels building up in storage mean recovery could take a while, and structural changes to demand may have accelerated. Even if oil prices were to rise strongly in 2021 for whatever reason, the already-delicate math would demand budgets remain on a tight leash. Remember, regardless of Covid-19, Exxon was having a hard time convincing investors of the wisdom of its enormous, counter-cyclical spending boom.

The growth-plus-dividends paradigm that defined the majors’ equity pitch for the past two decades is ending.

On that front, it’s worth noting the stock with the lowest yield of the group, Chevron Corp., enjoys that position in large part because it has shifted messaging and cash-flow priorities toward payouts (plus it has a good balance sheet). The company even walked away from a takeover battle last year, and looks far better for it compared to the nominal winner, Occidental Petroleum Corp.

The same goes for another large oil and gas producer outside the group, ConocoPhillips, which explicitly frames its payout policy as a way of dealing with a future of lower but more volatile oil prices. If investors aren’t willing to put a big multiple on oil earnings 10 years out, then Conoco’s approach is to offer them something tangible they might value in the interim. It also weights those payouts more toward buybacks, giving itself wiggle room in a tight spot such as now. This isn’t Big Mining’s payout ratio approach, but closer to it in spirit.

One important aspect to this concerns mergers and acquisitions. Two decades ago, the majors led consolidation amid another crisis. Those deals were about taking out costs but also gaining scale for new mega-projects. We are now at another natural point for restructuring the industry. This time, though, empire building will be met with disinterest, if not outright shareholder activism. Any deal will have to not only enhance return on capital but also dividend coverage. The biggest advantage the majors hold is their lower cost of capital at a time when hurdle rates for this business are rising. So any deals should be mostly paid in stock — which then adds to the payout obligation. Alongside earnings accretion, synergies-to-dividends could become a useful multiple.

We aren’t likely to see any shift in dividend policy in the immediate future; like everyone else, the majors will want to see how things shake out in the months ahead. If the Covid-19 crisis lingers and yields remain elevated, though, the pressure on more indebted companies to reset could mount quickly, especially as the larger issue of climate change isn’t going away. Muddling through the cycle doesn’t work quite so well if the overall arc is beginning to bend downward.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.