Oil Empowers the Poorest Nations, But at What Cost?

(Bloomberg Opinion) -- India is considering an ambitious net-zero emissions goal for 2050. This would portend trouble for oil producers: India accounts for 60% of projected demand growth through 2040 . The counterpoint is that the status quo also portends trouble, rendering such projections meaningless.

Oil’s future lies largely in the hands of the world’s up-and-comers. Demand from non-OECD countries surpassed that of developed economies in 2013. Yet emerging markets must balance raising living standards with the risk of getting flooded, scorched or otherwise scarred by climate change. As the oil industry defends itself against defunding, it argues its products, while adding to emissions, are also vital in elevating conditions for the planet’s poorest. This recasts oil as a flawed but necessary tool in promoting economic equity.

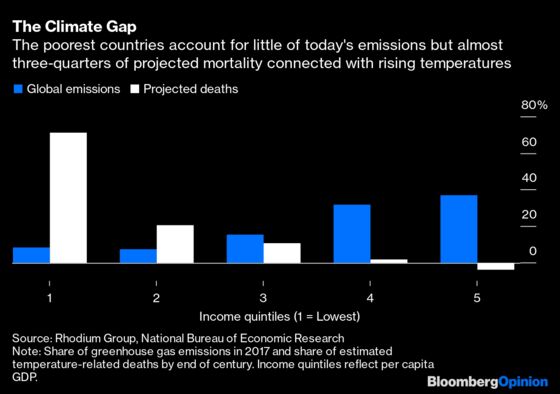

The catch: The poorest will catch it hardest when it comes to climate change.

Climate change supercharges the extremes of weather. For example, the average temperature in the U.S. in the two decades leading up to 2019 was 3% higher than for the period between 1950 and 1980. That sounds minimal. However, the number of days the average American experienced temperatures above 90 degrees Fahrenheit jumped by 23% . Warmer temperatures also make the atmosphere more of a sponge and, by melting ice caps, raise sea levels, leading to bigger and more frequent floods, storms and, by changing patterns of rainfall, droughts and wildfires. While Texas’ recent freeze can’t be conclusively linked with climate change, there is a strong argument that faster warming in the Arctic weakens the polar vortex that normally blocks frigid air from plunging south to the Gulf Coast.

Climate Impact Lab aims to quantify the effects of climate change. It estimates this will cost the U.S. 1.2%-1.4% of GDP per year, and rising, by around the end of this decade . To put that in perspective, if the pandemic cost 6%-10% of GDP in 2020, then the economic cost of climate change equates to a Covid-19 style disruption every 10 years, rising to every five years by mid-century.

And like Covid-19, climate change is as regressive as it is destructive.

Emerging economies lack the resources of their wealthier peers to cope with disasters. Many also lie around or within the Tropics, so they start warmer than the global average. Some, such as India, are prone to a combination of high heat and humidity, which limits the body’s ability to cool itself via sweating, raising the risk of heat stroke. This is especially bad for workers toiling outside, such as in agriculture, or in facilities with inadequate ventilation or cooling.

One way to think about this is via the counterfactual: The American South, where the penetration of air conditioning, especially from the 1950s onward, coincided with the reversal of a century of net population outflows, heralding the rise of the Sunbelt . As climate change progresses, the number of people exposed to severe heat stress is increasing, with parts of South Asia and the Middle East particularly at risk .

Here’s where those oil projections come into question. “Countries for whom climate change will matter most are the same countries expected to deliver most of the growth in oil and gas demand,” says Trevor Houser, a partner at Rhodium Group, co-director of the Climate Impact Lab and author of a recent essay on the unequal impacts of climate change.

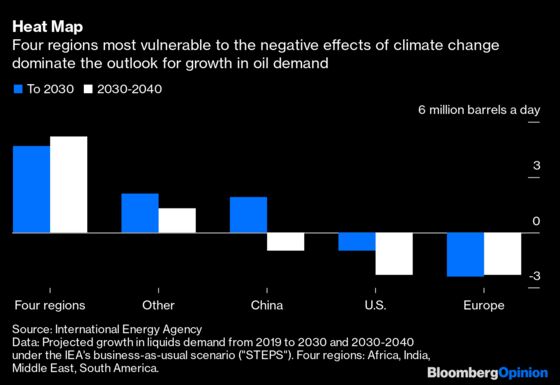

Oil demand growth over the next two decades is tied overwhelmingly to four of the most vulnerable regions: India, the Middle East, Africa and South America.

If the U.S. is feeling the economic drag from climate change already, it’s a fair bet these four regions will suffer worsening economic effects from here. Using a simple analysis tying oil demand to underlying GDP assumptions, relatively small impacts on economic growth have significant outcomes . For example, say climate change effects cut average GDP growth for the four regions by 0.25% per annum in the 2020s rising to 0.5% in the 2030s. This shrinks their projected oil demand growth by 300,000 barrels a day this decade and 1.5 million barrels a day the next. That is equivalent to wiping out all the anticipated growth from South America in the 2020s — and flipping global oil demand growth in the 2030s from positive to negative.

There is an inherent injustice in emissions to date reflecting the earlier industrialization of the developed world, meaning emerging economies cannot take that same path without risking the future for everyone. Worse, they will likely be hit hardest by higher temperatures, flooding, drought, disease and all the other impacts of climate change. Relying on air conditioning under the current energy paradigm would merely compound the problem in a vicious circle.

Countries such as India of course must balance access to reliable energy sources, and the positive impact this has on living standards, with the risks to those living standards that come with some choices. Nature doesn’t do fairness, and the apparent cheapness of fossil fuels belies the climate debt they continue to build up and which is falling due already.

A growth model for the oil business predicated on vulnerable countries sticking with business as usual is less empowering than advertised. It’s also unlikely to pan out.

Source: World Energy Outlook, 2020 (International Energy Agency). Projections as per Stated Policies Scenario for 2019-2040.

Average impact of six models published since 2012, as per "The Economic Impact of Global Warming" (Oxford Economics, November 2019).

Source: Rhodium Group.

The range reflects moderate-emissions (RCP 4.5) and high-emissions (RCP 8.5) scenarios. RCP stands for Representative Concentration Pathways, modeled measures of the greenhouse effect.It's important to note that these figures represent annual averages of climate-related shocks which tend to be lumpy in their impact, with some years better or worse than others. Moreover, the figuresexclude the compounding effects of shocks in prior years. Measured on a cumulative basis, the impacts would be even higher.

Source: "The End of the Long Hot Summer: The Air Conditioner and Southern Culture" by Raymond Arsenault,Journal of Southern History(November 1984).

Source: "The emergence of heat and humidity too severe for human tolerance" by Colin Raymond, Tom Matthews and Radley Horton (Science Advances, May 2020).

"Global non-linear effect of temperature on economic production” by Marshall Burke, Solomon Hsiang, Edward Miguel (Nature, October 2015).

I use the IEA's GDP growth assumptions and oil demand projections under its business-as-usual scenario to calculate implied oil intensity for each region (ie, barrels of oil per dollar of GDP). Holding those constant, I then adjust the GDP assumption to imply a new figure for projected oil demand.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2021 Bloomberg L.P.