(Bloomberg Opinion) -- It is 75 years since the developed world signed up for a new version of the gold standard at Bretton Woods, and almost 50 years since that peg to gold was abandoned. Since then, the world has muddled through with a system anchored to the oil price, and relying on faith in central banks. That is, until now.

Easy monetary policy has delayed the denouement for more than a decade, but if there’s a clear message from the extraordinary market events of the last few weeks, it’s that the current financial order no longer suffices to maintain the stability we’ve grown accustomed to expect. With no sense yet of what that new order might be, and a dearth of global leadership needed to summon it, it’s safe to assume markets and economies are in for a rough period. The coronavirus crisis is just the start.

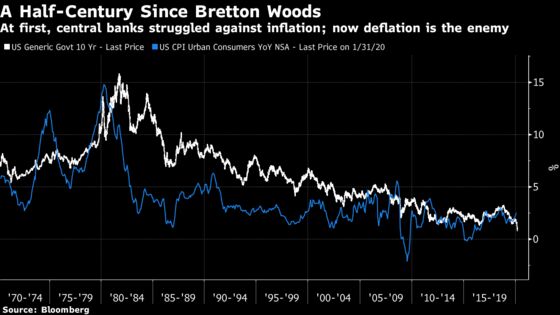

To see how we arrived at this point, it’s best to trace the history. After the war, the developed world agreed to the Bretton Woods accords, which tied all currencies to the dollar, which was in turn pegged to gold. This loose version of the gold standard survived until 1971, amid generally stable markets and low economic volatility. It foundered in 1971 when Richard Nixon ended the gold peg, which he felt had become too great a burden for the U.S.

For the next decade, the world was no longer anchored to the dollar, but to oil. With the tie to gold gone, oil producers needed to hike prices to keep their buying power constant. This they did. In dollar terms, oil suffered two immense shocks during the 1970s, which plunged the world into stagflation. But in gold terms, the oil price ended the decade more or less where it had started; oil producers had protected themselves against the falling purchasing power of the dollar:

This ‘Oil Standard’ era ended in the early 1980s, at a point when markets — and everyone else — had lost faith in the ability of central banks to control inflation. Paul Volcker arrived at the Fed (as the result of a virtual political accident when President Jimmy Carter moved Volcker’s predecessor to the Treasury Department), and set about raising rates more than anyone thought he would dare. This provoked a recession, and eventually convinced everyone that central banks could control inflation after all. That started a long secular bull market in bonds as yields started a gradual fall.

Meanwhile, Ronald Reagan and Margaret Thatcher brought their new unapologetically free-market approach to economic management, the Soviet Union collapsed, and China embarked on economic reforms. Volcker’s victory over inflation ushered in a quarter-century of triumph for a broadly laissez-faire model of globalization anchored by trusted central banks:

That foundered in the financial crisis of 2007-09. The immediate fear in the wake of the Lehman Brothers bankruptcy was that a balance sheet recession would come in its wake, bringing with it deflation. This time, in other words, the fear was that central banks wouldn’t be able to prevent deflation, rather than the inflation that they had struggled to control a generation earlier. Briefly, bond markets signaled that inflation in the U.S. would average less than 0% over ten years.

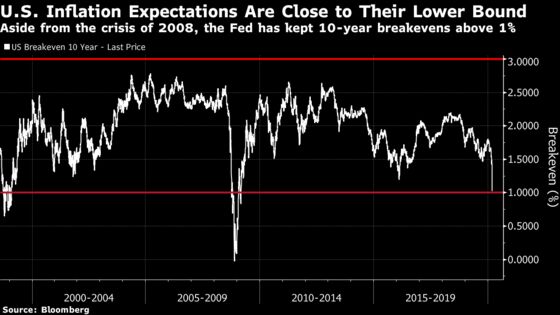

That was the first time that inflation expectations had breached the Fed’s target to keep inflation between 1% and 3%, which has been in place for many years now. The response was a massive program of quantitative easing asset purchases (QE) to keep longer bond yields low, while cutting short-term rates virtually zero. For a decade, this was enough to keep inflation within its range — but 10-year inflation expectations on Monday dropped below 1%. This time, central banks have little or no ammunition left.

Meanwhile, the ratio of oil to gold (which can be seen as a measure of confidence in central banks to safeguard the currency) has plunged after remaining remarkably stable through the market slings and arrows of the last half century. So far this year, it has halved, bringing it to a post-Bretton Woods low. The volatility of the measure in the last few days, a product of the oil price war unleashed by Saudi Arabia, is exceptional:

Now that there is no confidence that central banks can avert deflation, the central case for buying stocks has also eroded. For the post-crisis decade, the U.S. has managed to stay distinct, thanks in part to the privilege of the world’s reserve currency, and in part to the superior success of its corporate sector. It has done this even as Japan and Western Europe have sunk into negative interest rates, and emerging markets have stagnated. In both regions, stock markets have remained in a long-term bear market, stuck below the highs they set before the crisis (or in Japan’s case, stuck below a high set on New Year’s Eve, 1989).

In the U.S., investors were guided by a different logic: TINA (for There Is No Alternative). They held to the theory that low bond yields left no alternative but to buy stocks. Equities looked expensive compared to their own history, and their profits were stagnant, but low bond yields still justified buying them. The market has now abandoned that argument as well, finally accepting that bond yields this low only make sense if a drawn-out deflationary recession lies ahead, which would be terrible for stocks. TINA is vanquished:

Stocks’ dividend yield is now much higher than the yield on a 10-year Treasury bond. But now, this is taken as a negative sign, and the stock market has continued to sell off. This makes a telling contrast with the last time stocks were this cheap relative to bonds, in March 2009 — the beginning of the great rally in the stock market. This time, the twin shocks of the epidemic and the oil price have shredded confidence.

If a decade of desperate easy monetary policy by central banks was enough to avert the need to hammer together some new global financial order, markets are now indicating that this moment can no longer be delayed. With confidence lost in central banks, that new order looks almost certain to involve the kind of fiscal expansion that has been out of vogue since the 1970s, possibly even including helicopter money. Extremely low bond yields signal to governments that we will be able to finance such spending very cheaply. Ideally, any new order would involve new international agreements to avoid the damaging effects of the trade, oil and currency conflicts of the last few years.

And needless to say, the political environment doesn’t look conducive to finding agreement on anything so ambitious. The world will find itself to a new version of Bretton Woods in time, but it will take volatility, trial and error. At some point, some latter day Paul Volcker will emerge and guide us to a new model that will work. For the time being, it would be wise to brace for economic and market disruption to match what was experienced at the end of the 1970s and the beginning of the 1980s.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

John Authers is a senior editor for markets. Before Bloomberg, he spent 29 years with the Financial Times, where he was head of the Lex Column and chief markets commentator. He is the author of “The Fearful Rise of Markets” and other books.

©2020 Bloomberg L.P.