(Bloomberg Opinion) -- Representative William Seitz declared several years ago the Ohio State Legislature was not prepared to continue its “march up state mandate mountain.” He was voicing opposition to renewable and energy efficiency standards he had described as Stalinist, which, even with the healing power of time, comes across as a tad overwrought.

Guess what, though: It turns out Seitz isn’t against mandate mountains altogether. It’s just a question of which mountain he chooses to climb.

Seitz co-sponsored House Bill 6, which passed Ohio’s august body and was swiftly signed by Governor Mike DeWine on Tuesday. Among other things, the bill will provide subsidies to nuclear power plants and two old coal-fired plants while weakening the state’s alternative-energy portfolio standard and energy-efficiency benchmarks. In short, it delivers substantial blows to the Stalinist scourge of encouraging wind and solar power and more efficient use of electricity in general, while providing a handout to struggling conventional generators.

And struggling they are. The Davis-Basse and Perry nuclear plants, both on the shore of Lake Erie, are at risk of shutting down within a couple of years without support, according to their bankrupt owner, FirstEnergy Solutions. According to BloombergNEF’s model, the two plants tend to be loss-making and are projected to be $161 million in the red this year. So the support from HB6, worth up to $150 million a year from 2021 through 2027, looks very handy.

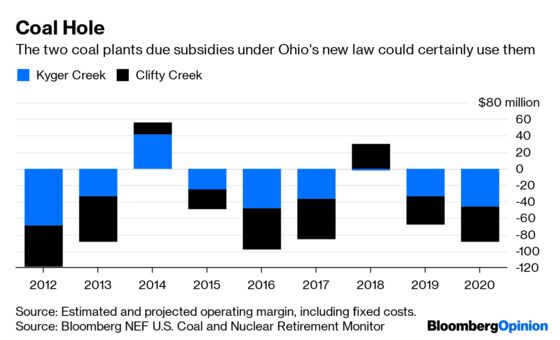

The same goes for the two coal-fired plants – one of which is in Indiana – run by the Ohio Valley Electric Corporation. OVEC is co-owned by a number of power companies including FirstEnergy Corp., AES Corp. and American Electric Power Co. Inc. These two plants, constructed originally to power uranium enrichment for the Atomic Energy Commission, first switched on 64 years ago and their modeled margins look anything but sprightly.

The new law’s language doesn’t make it easy to work out how big the subsidy to OVEC’s plants will be. However, Timothy Fox of ClearView Energy Partners LLC, a D.C.-based analysis firm, estimates it adds up to about $60 million a year between 2020 and 2030 – which compares quite nicely to the average annual $53 million loss from the two plants between 2012 and 2019, as modeled by BloombergNEF.

FirstEnergy, headquartered in Akron, is a clear beneficiary of the law. Having made the spectacularly mistimed acquisition of coal-heavy Allegheny Energy Inc. in early 2011, FirstEnergy saw the economics of generation upended by flat-lining power demand, cheap shale gas and encroaching renewable energy, pushing its merchant-generation business, FirstEnergy Solutions, into bankruptcy.

The Ohio Public Utility Commission has tried to help out with various measures, including my personal favorite, the “Distribution Modernization Rider,” which levied a fixed charge on the good ratepayers of Ohio under the rubric of spiffing up the grid – without actually requiring FirstEnergy to allocate the money to that. The state’s supreme court eventually overturned it, saying “something cannot be an incentive if it does not direct the utility toward a particular desired outcome,” which is tough to argue with, let’s face it.

The new law has had an impact already: Moody’s Investors Service just upgraded the relatively low credit ratings of four of FirstEnergy’s utility subsidiaries.

Its effects won’t end there, though. In drawing money away from renewable energy and efficiency mandates and directing it toward mandates for nuclear and coal plants, HB6 is like the inverse of renewable portfolio standards, using subsidies to extend the life of old technologies rather than encourage new ones. It’s possible to argue that, as a zero-carbon-emissions source of power, it makes sense to subsidize nuclear. But doing that in tandem with measures discouraging energy efficiency and new zero-carbon technologies (where, unlike with nuclear, costs are falling) and subsidize coal plants from the Eisenhower era rather shreds that line of reasoning.

Instead, Ohio appears to be prioritizing both corporate interests and local economic and employment issues. As with towns left bereft by the closure of coal mines, so with power plants further down the supply chain shuttering. With any far-reaching technological disruption – especially one linked to the broad threat of climate change – there is an important role for public policy in alleviating the negative impact on communities dependent on the old paradigm. Yet Ohio’s approach is from the King Canute school of trying to hold back the tide. In the process, it will socialize corporate losses and pollution while stymieing incentives for new projects and energy businesses.

Moreover, it’s an extreme example of a broader trend in the U.S. electricity sector; namely the erosion of wholesale power markets in favor of a panoply of directives that override price signals. “No one is speaking about the implications [of the law] for PJM,” says Fox, referring to the regional power market of which Ohio is a part. The more non-energy-related burdens are placed on power pricing, the tougher it is for those markets to function properly. Consider Energy Secretary Rick Perry’s attempts to subsidize nuclear and coal-fired plants on the spurious grounds of grid stability and national security

While this might read as an argument against renewable portfolio standards, it isn’t. Remember, those are in place in lieu of a more transparent price signal to address the externalities of fossil fuels, such as a carbon tax. The latter could actually help nuclear power plants but would crush the tottering coal industry and the power plants it supplies. Which is why Ohio’s supposed market purists denouncing subsidized wind and solar power prefer instead to simply craft their own subsidies, swapping a vision of sunlit uplands for a mountain of coal.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.