(Bloomberg Opinion) -- Occidental Peteroleum Corp. is offering you the chance of a lifetime: to be just like Warren Buffett.

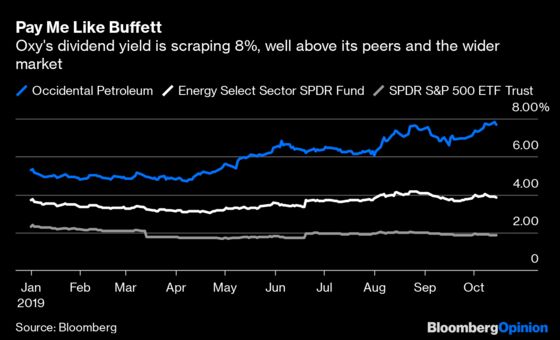

Oxy’s stock yields 7.7% and hit 7.9% at one point on Monday. That is roughly four times what the S&P 500 pays. More importantly, it is within a whisker of 8% — the yield Oxy now also pays to one Berkshire Hathaway Inc. These two things are not unrelated.

Recall that Oxy won this year’s battle for Anadarko Petroleum Corp. by outbidding Chevron Corp., partly with the aid of $10 billion from Berkshire. This came with the usual payday-loan accoutrements of that high yield, a takeout premium and warrants. Buffett’s cash also helped Oxy avoid putting the deal to its own shareholders — although many appear to have voted it down anyway, in a manner of speaking:

Oxy’s stint in the doghouse partly reflects fear, with oil dropping just as Oxy’s debt ballooned. For at least the next year or so, the equity story looks yoked to the twists and turns of the trade war, which is as unsettling as it sounds.

More importantly, though, Oxy’s bet on Anadarko has put it at loggerheads with what investors want from oil companies these days.

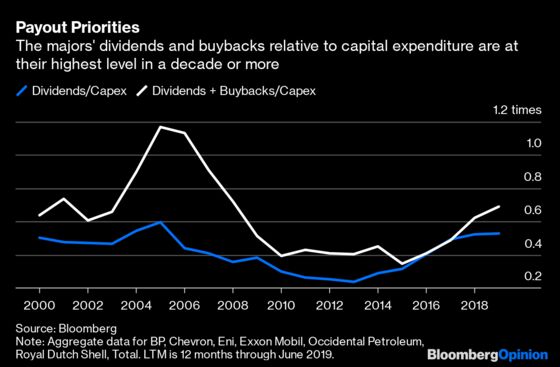

What do they want? Dividends. More to the point, investors have reset the parameters of what’s acceptable in terms of how oil companies apportion cash flow. Poor returns on prior investment by the industry plus concerns about a looming peak in oil demand add up to investors wanting more of that cash directed into their own pockets rather than into drilling budgets. Oil majors have adjusted accordingly:

Broadly, there are three claimants on cash flow: the company (capex), creditors (interest and principal) and shareholders (dividends). The sector zeitgeist is to minimize the first two to make more room for the latter.

Oxy was an exemplar of this, but the Anadarko deal has changed the equation. Even allowing for disposals announced so far and a joint-venture payment from Ecopetrol SA, pro forma net debt has virtually tripled from Oxy’s standalone level. The extra leverage will haunt Oxy if 2020 turns out to be bad for oil prices – and based on the market’s remarkably sanguine reaction to the recent attack on Saudi Arabia, it might well be.

To counter this, Oxy says a round of oil-price hedging means it can cover its dividend if West Texas Intermediate crude oil averages in the low $40s per barrel next year (it’s averaged about $57 so far in 2019). By 2021, Oxy says, it could break even at $40 a barrel without hedging as various efficiencies kick in. Consensus forecasts compiled by Bloomberg show Oxy generating just over $3 billion of free cash flow in 2020 versus a pro forma dividend payment (assuming it stays flat) of just over $2.8 billion.

The caveat to this resilience case is that it would mean Oxy cutting back on capex to “maintenance” levels, implying little or no growth. Oxy raised its guidance for third-quarter production by 3% on Tuesday morning, which is positive. But if weak oil prices portend a flat line for the next year or so, then investors’ demand for that high dividend yield wouldn’t be going anywhere.

The added fixed costs of higher interest payments and the Berkshire dividend have made Oxy more of a levered play on oil prices at a time when the latter look lifeless. Oxy’s most recent earnings presentation emphasized billions of excess cash (and growth) in 2021 if oil averages $60 or $70 a barrel. In the meantime, though, a big chunk of any value from the Anadarko deal accrues to Buffett. Of the $2 billion of annual pre-tax cost savings (“synergies”) from the deal, $800 million goes post-tax to servicing those preferreds. Indeed, factor in the warrants and take-out premium, plus the $1 billion break-up fee paid to Chevron — along with some other assumptions — and while Oxy’s legacy shareholders get 50% of the net present value of the synergies, Berkshire takes 40%.

Oxy expects another $1.5 billion of capex synergies from the Anadarko deal, although this figure came with lower growth guidance so the actual gain in value is less clear, especially if the budget gets slashed toward maintenance levels in the near term.

An earnings call is due in three weeks, and Oxy will need to double down on the reassurance it gave in early August. Progress on disposals to cut debt would help. An obvious choice is the stake in Western Gas Partners LP inherited from Anadarko. But this hasn’t materialized yet, and the value of the common units held in Western Gas has dropped by $1.9 billion since the bidding for Anadarko got underway in April. Absent that, details on alternative candidates are needed.

Perhaps more importantly, Oxy must make a robust case for synergies coming through sooner rather than later. The current narrative of resilience and leverage to higher oil prices offers some defense against worries about the dividend’s sustainability. However, the oil-price option gets little traction in the current environment where investors are focused on cash today rather than theoretical windfalls tomorrow. Having tilted the cash flow math toward interest and those Buffett payments, Oxy is in a race to show something tangible for its own shareholders coming through from this deal. Looking at that dividend yield, they require some convincing.

Assumespreferreds are redeemed for 105% of face value on the 10th anniversary of the deal and all dividends have been paid in full with no accruals. Warrants valued at $542 million using the Bloomberg options calculator as of August 9, 2019 (day of Anadarko acquisition's completion) and assumed to convert to a pro forma stake in Oxy of 8.1%. Tax rate of 21% and cash flows discounted at 10%.

Anadarko's legacy shareholders get just under 10%.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.