(Bloomberg Opinion) -- Warren Buffett is credited with that old saying about receding tides and embarrassed skinny-dippers. In Occidental Petroleum Corp.’s case, the lack of swimwear is one problem, but so is the anchor tied around its ankle. Part of that anchor is the old sage himself.

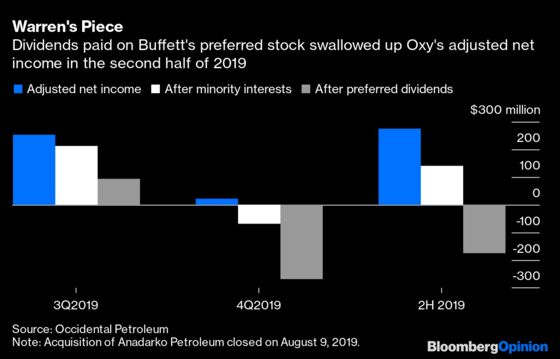

Oxy, as it is known, just reported results for its first full quarter since acquiring Anadarko Petroleum Corp. In that bruising takeover battle against Chevron Corp., Berkshire Hathaway Inc. provided a crucial $10 billion check allowing Oxy to avoid a shareholder vote. It came at a steep cost of, among other goodies, an 8% preferred dividend. As it turns out, that was more than enough to swallow Oxy’s adjusted net income for the second half of 2019 before any of it could trickle down to the commoners.

Buffett didn’t get rich by giving stuff away, so the fact Oxy went to him in the first place signaled just how far it was stretching. Back then, things looked dicey already on the trade-war front. But in early 2020, Oxy finds that not only has the tide gone out, it has gone way out, similar to what happens just before a tsunami floods back in. The tsunami is the coronavirus crisis, swamping an already fragile oil and gas market.

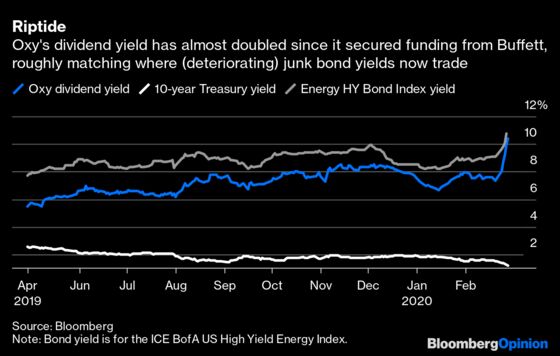

A few numbers tell the story. Oil traded at almost $66 a barrel when Oxy entered the fray for Anadarko; it has since dropped to about $45. When Oxy CEO Vicki Hollub made her fateful flight to Omaha, Nebraska, the 10-year Treasury yield was just over 2.5%, Oxy’s stock yielded about 5.5%, and high-yielding energy bonds paid about 7.75%.

Now Treasuries yield less than 1.2%, so the spread Buffett earns from Oxy, about 5.5% when the deal was struck, is closing in on 7%. Oxy’s own dividend yield, which used to be lower than Buffett’s preferred, spiked as high as 10.7% on Friday morning, roughly where the energy high-yield index ended Thursday.

As of Friday lunchtime in New York, Oxy’s dividend yield was 10.2% and its stock was at its lowest level since early 2009 (not a period remembered with great fondness).

The market is treating the dividend like a distressed credit. Even using Oxy’s adjusted figure for cash from operations before extraordinary charges and working capital, free cash flow in the fourth quarter was less than $60 million, not enough to cover the $149 million paid out on preferreds, let alone the $700 million or so in common dividends.

As a result of the deal, Oxy’s interest and dividend obligations have risen from just under $750 million a quarter to more like $1.25 billion ($200 million of that is Buffett’s). Including guided capex, Oxy needs an Ebitda run-rate of about $2.6 billion a quarter to cover all this from cash flow. Consensus estimates average about $2.9 billion a quarter this year, and Oxy has further asset sales to come, as well as more cost savings to realize from the deal (although at least some of the latter should be in consensus forecasts already). This implies Oxy can cover its obligations based on current observations, but with little left over to cut into net debt — now $35 billion, versus $8.5 billion at the end of June. That will rely mostly on disposals for now, although Oxy says it can also cut capex further if necessary, albeit at the expense of growth.

This position is all too familiar in the energy sector. To buy Oxy now is to bet it can reap savings and realize prices on disposals that will offset the headwinds in the oil and gas market — although, as several questions on Friday morning’s call addressed, the risk around disposals has increased as oil prices have tanked. Alternatively, it’s a straight bet oil prices will rebound once pandemic fear passes. The company’s well-timed hedging of 2020 production helps. And unit costs in the upstream business, especially in the U.S., have declined dramatically already since last summer, providing credibility on the synergies story. But chipping away at that debt may be a grueling process.

This is a bigger issue than just where oil prices will eventually wash out in 2020. In the same week Oxy reported these results, energy stocks’ weighting in the S&P 500 dropped below that of utilities for the first time ever. Generalist investors were abandoning the sector long before troubling news reports began emanating from China. They were put off by weak governance and high leverage, plus they’re no longer buying the traditional option on oil-price increases.

The Anadarko deal, and how it was done, ticked all these penalty boxes, piling obligations onto Oxy’s cash flow just before oil prices slumped. While some hedge funds may be willing to rent the stock for short-term bets, Oxy needs to rebuild enough trust to tempt value investors back in from the thinned-out generalist crowd. That’s tough in general, and even harder when infection updates keep crossing the wires. Sure, no one could foresee the coronavirus outbreak. But Oxy’s been through enough cycles to know oil is no stranger to black swans.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.