(Bloomberg Opinion) -- Ocado Group Plc is fond of making excuses for disappointing grocery sales growth. In the past, it has blamed everything from a shortage of drivers in the run up to Christmas to its health-conscious customers ordering less juice.

So it was reassuring that the company was able to cope with a devastating fire that destroyed a distribution center in Andover, England in February better than the market had feared. If it had needed an excuse for any of its recent results this disaster would have provided a legitimate one, so the company has done well to minimize the impact.

It said Tuesday the incident shaved 2 percentage points off of retail sales growth in the first half of the financial year to June 2, even though it lost 10% of its delivery capacity.

Ocado maintained its outlook for full-year expansion in its retail sales of between 10% to 15%, and the shares duly rose 10% on the news. This deserves credit because the fire has created a heavy financial toll.

The company took a 99 million pound exceptional charge in the period, primarily from writing off the value of the destroyed assets. Though this will be offset by insurance recoveries, as rebuilding the warehouse will be fully covered, Ocado’s first-half loss rose from 13.6 million pounds to 142.8 million pounds.

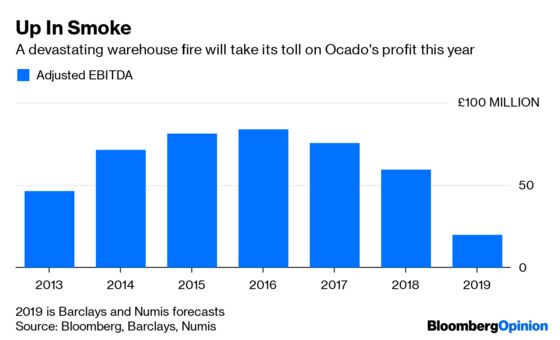

It also cautioned that the fire would reduce its full-year Ebitda by 15 million pounds, while the cost of management incentive plans would cut it by 10 million pounds.

Analysts at Barclays said this implied full-year Ebitda of about 20 million pounds, compared with estimates of about 45 million pounds previously.

This financial impact of the fire is unhelpful, but hardly surprising, given the loss of a state-of-the-art warehouse. Tuesday’s report has presented investors with a lot to chew over, but it adds up to a lot of noise. None of it changes the fundamental investment case for Ocado.

This depends on two things. First, it must also make a success of its new deal with Marks & Spencer Group Plc. That means a seamless replacement of Waitrose, its current partner, with M&S, and migrating customers used to Waitrose products to the new arrangement. This is challenging, though not insurmountable.

Second, it must continue to win contracts to run the online grocery arms of other retailers around the world and convert these into profit. It has certainly racked up the deals over the past year or so. But that is yet to translate into meaningful earnings growth. It will soon receive a 562.5 million pound cash payment from M&S, and this should ease worries about whether it has adequate capital to invest in the new partnerships.

While Ocado’s technology arm is potentially lucrative, it is work in progress. The group is also facing competition from rivals including Today Development Partners, a company co-headed by one of Ocado’s original founders, which has signed a deal with Waitrose.

The shares are up about 45% since confirmation of the M&S partnership. On an enterprise value to forward sales basis, they trade on 4.3 times, putting it ahead of Amazon.com Inc.

Investors are clearly assuming a smooth delivery of its future plans. But as any long-time follower of Ocado knows, with the online supermarket turned tech titan, that is far from guaranteed. Progress is just as likely to get stuck in the warehouse.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.