(Bloomberg Opinion) -- “Be greedy when others are fearful” is a classic Warren Buffett aphorism. You might think Spanish bank BBVA SA is pushing the principle too far with its offer to buy all the shares it doesn’t own in its Turkish subsidiary, Türkiye Garanti Bankası.

In truth, however, BBVA already bears all the risks of Garanti in practical terms but is only collecting half the profits.

News out of Turkey hasn’t been great, to say the least. Since BBVA launched the voluntary takeover bid for Garanti in mid-November, the Turkish lira has dropped nearly 30% against the euro and consumer prices soared to a two-decade high of 36% in December. Mainly that’s because President Recep Tayyip Erdogan keeps pushing his unorthodox policy of fighting rampant inflation with interest-rate cuts.

The lira has crashed even though the central bank has sold record amounts of foreign currency from its reserves and pursued other unusual measures to support it. Economic growth is forecast to slow dramatically this year and next, according to the Organization for Economic Cooperation and Development, which predicts things could get worse without big policy changes. One big risk this year is that Turkey needs to raise foreign-currency funding equivalent to 20% of its gross domestic product, according to the OECD.

But while the economic risks are rising, the cost to BBVA of buying the rest of Garanti’s shares has tumbled in euro terms from 2.25 billion euros ($2.6 billion) — when it launched the bid — to 1.64 billion euros on Monday. The offer price is fixed in liras at 12.20 per share.

BBVA sees Turkey as a country with good long-term potential: A young population with little household debt offers great prospects for a bank. BBVA still expects annual revenue growth rates from Garanti in the high teens. Analysts at Jefferies reckon it will be slightly slower than that. But for a European bank, even the less optimistic view is not to be sniffed at.

There is really little difference if things go off the rails whether BBVA owns all of Garanti or just the 49.75% that it holds today. If the Turkish economy got so bad that Garanti needed to be propped up, the Spanish lender might have to fund a capital injection alone anyway. Local shareholders would likely be pressed for cash. With a core capital ratio of 13.2%, that’s some way off.

BBVA already has to consolidate all Garanti’s assets into its group accounts but it isn’t allowed to count all of the equity provided by local shareholders toward its own capital ratio. This means it needs to put more capital behind Garanti’s business than its ownership implies.

The big risk for Garanti is that Turkey’s economy really tanks and leads to heavy losses from bad loans. In the most extreme scenario, those could burn through Garanti’s capital. But even in the worst case, BBVA could in theory walk away and lose no more than the value of its equity investment. If it fully owned Garanti, that would cost a few billion euros — painful for sure but not a disaster: BBVA is planning a 3.5 billion-euro share buyback this year, and it has 4.6 billion euro in spare capital on top of that.

The reason it could walk away is that BBVA – like Banco Santander and HSBC – has an unusual structure. It is a collection of separately capitalized and self-funding subsidiaries. Most big multinational banks aren’t built like this: They are single groups with all their capital in the same place. Single-entity banks are more efficient in some ways than banks like BBVA. But the tradeoff is BBVA’s different businesses are quarantined from each other.

In practice, however, BBVA’s ability to cut loose from Garanti is probably limited, according to Benjie Creelan-Sandford, an analyst at Jefferies. Clients in other countries where it operates would be shocked, and other regulators might look for ways to ensure BBVA wouldn’t do the same in their backyards.

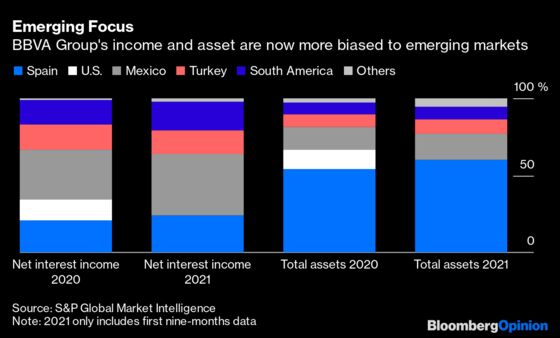

BBVA has become more focused on emerging markets since selling its U.S. arm to PNC Financial for nearly $12 billion last year. More than one-third of its assets and about three-quarters of its net interest income are from Turkey, Mexico and South America, according to S&P Global Market Intelligence. The balance is mostly from Spain.

Taking over Garanti fully won’t change BBVA’s risk profile much — its emerging-market focus is partly why its stock has underperformed other European banks recently — but will boost its earnings by about 14% this year.

It’s ironic that global investors are averse to emerging markets while they are happily throwing money at blank-check companies, crypto assets and digital pictures of apes. For specialists like BBVA there are reasons to be fearful, but with its existing exposure to Turkey, BBVA might as well be greedy too.

More From This Writer and Others at Bloomberg Opinion:

- Purges Are Just Another Day at the Office in Turkey: Daniel Moss

- Erdogan's Dangerous Obsession With Low Rates: Bobby Ghosh

- Turkey Can’t Take Much More of Currency Crisis: Mohamed El-Erian

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2022 Bloomberg L.P.