(Bloomberg Opinion) -- In periods of distress, it’s sometimes better to eschew the comforts of companionship and go it alone.

Renault SA’s board postponed a decision Tuesday on Fiat Chrysler Automobiles NV’s proposed 50-50 merger after meeting resistance from Nissan Motor Co. Last week, Jean-Dominique Senard, the man tapped to lead the combined Fiat-Renault, visited Tokyo to sell the benefits of the deal to the French carmaker’s alliance partner. The plan would create the world’s third-largest automaker.

Both companies have made efforts to keep embattled Nissan in the mix, but what does the Japanese carmaker get out of this? Under the initial proposal, synergies of around 1 billion euros ($1.1 billion) are estimated to accrue to Nissan and Mitsubishi Motors Corp., which have shared an alliance with Renault for two decades. Nissan would have one nominee on the board of the post-merger company. Its 15% stake in Renault would be diluted to 7.5% of the combined entity, though this would come with voting rights, unlike currently. The deal would also dilute the French state’s control over Renault and therefore Nissan, easing a source of friction.

Nissan has appeared to be on the fence. After meeting Senard, CEO Hiroto Saikawa said “we want to see specifically where they will come from” on the potential benefits to the Japanese company. Nissan didn’t consider the merger a “minus” and would watch developments carefully, he said.

Saikawa has been cool on deeper ties with the French carmaker since the Carlos Ghosn saga opened questions over the future of the alliance. In Nissan’s latest earnings call, the CEO said he and Senard had different views on the relationship their companies should have.

The truth is that neither closer ties with Renault nor being part of a bigger Fiat-Renault combination will produce much value for Nissan, now or in the future. Nestling between these two giants may allow the Japanese automaker to bumble along for a while longer; it might also be able to leverage some economies of scale around the globe. These benefits are largely theoretical, though, and are counteracted by the considerable execution risk in combining companies of such size.

Nissan has its own problems to worry about, without becoming embroiled in a complex cross-border merger. Its core business has been a shambles. Global production slumped 10% in April and sales were down 5%. Profits are shrinking along with margins. In the aftermath of Ghosn’s exit, the company’s governance structure and track record are looking in need of urgent review. Nissan’s handling of the situation and of its business have led to severe destruction of shareholder value.

In the key market of China, Nissan has been doing better than Renault or Fiat Chrysler. While the company has lagged Japanese peers, it has about 6% of the market, helped by its Qashqai and Kicks models. That compares with less than 1% for Fiat Chrysler and even less than that for Renault. The Japanese carmaker may benefit from a recent decision by the Chinese government to extend license plate quotas for internal combustion engines in areas where Nissan is strong. Meanwhile, its Sylphy model has performed well in a market where industry sales are dropping rapidly.

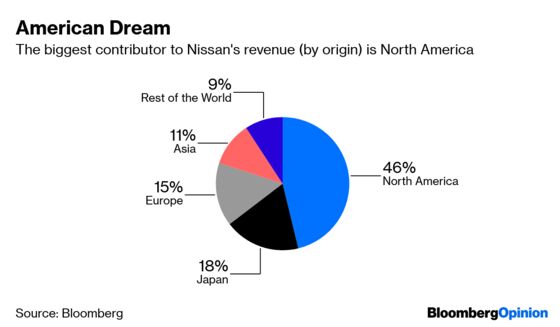

Fiat Chrysler will want to bring together operations in North America, where its models include Ram pickups and Wranglers. That will be complicated and the outcome is likely to be inefficient. North America accounts for the biggest share of Nissan’s revenue, though the company has been struggling there, having adopted an aggressive and expensive U.S. strategy pinned on sales incentives. Customers have been buying Nissan cars for the discounts rather than the brand or features, executives acknowledged in a recent earnings call. U.S. tariffs on Mexico are an added difficulty.

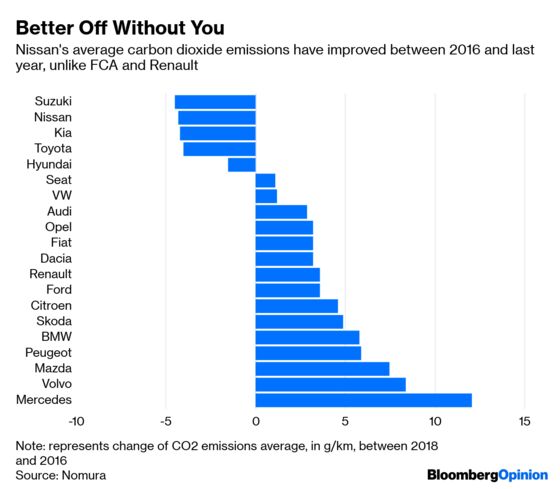

In Europe, Nissan probably has more to offer Renault and Fiat Chrysler than the other way around. While its operations are likely to be hurt by Brexit and the company is reining in production, the average carbon dioxide emissions of its fleets are lower and have been coming down. By contrast, performance at Renault and Fiat Chrysler has worsened since 2016, making it harder and more expensive for the companies to comply with new regulations. For Fiat Chrysler, the benefits of shared technology and bringing down emission compliance payments could account for as much as half of its share of savings from the 5 billion euros annual run rate of synergies resulting from the merger, according to analysts at Morgan Stanley. Nissan, meanwhile, also has contenders in the race for electrification, such as the Leaf and Sylphy.

With all these issues, does Nissan need the added complexity or the extended political and regulatory drama that a Fiat-Renault merger is likely to entail? Nissan needs to run a far leaner business, focused on the very areas that risk being cannibalized in a merger or deeper alliance. The company risks being left in a state of paralysis if it’s sucked further into this process.

Nissan has been through a rescue once before: The benefits of the Renault partnership have largely run their course and, 20 years on, the company hasn’t been able to extricate itself. Getting tied up in another knotty situation is the last thing it needs.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.