(Bloomberg Opinion) -- Haven’t we seen this play before?

NIO Inc., a Chinese electric-vehicle maker that was talked up as a potential Tesla Inc.-killer before its $1.15 billion initial public offering last year, is falling apart before our eyes.

The stock fell 20% in the U.S. on Tuesday after the company reported a 3.29 billion yuan ($462 million) net loss in the second quarter on a gross margin of minus 33%. Those sorts of figures make Elon Musk’s company look like a staid and sensible investment.

What’s most striking is that NIO is racking up these massive losses in spite of a business model that in theory ought to be far more efficient than conventional carmaking. In that sense, the better comparison isn’t Tesla, but WeWork – a company that pitched itself as a radically different technology play, only to be brought down to earth by the humdrum nature of operating in the real world.

One thing that makes NIO unusual is that, as my colleague Anjani Trivedi has explained, it doesn’t actually make cars. Instead it takes 45,000 yuan deposits from customers, provides a drive-train, and contracts out the rest of the build process to Anhui Jianghuai Automobile Group Corp. On top of that, it doesn’t have a dealership network, instead selling cars through an app and a web of slick WeWork-style clubs, known as NIO Houses.

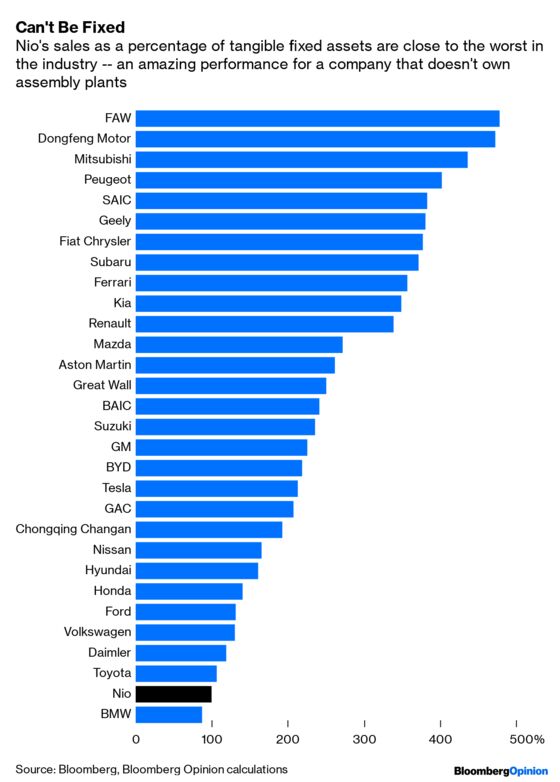

In principle, that could result in efficient deployment of capital, but things start to look dicey when theory comes up against the reality of NIO’s spending habits. If you compare revenue over the past year to NIO’s tangible fixed assets, it has some of the worst capital efficiency in the global car industry. For a company that doesn’t own assembly plants, that’s a heroically bad performance.

What’s going wrong? For starters, contract manufacturing isn’t as efficient as you might think. Even excluding the costs associated with recalling almost a fifth of the cars NIO has sold due to battery fires and overheating, the gross margin on vehicles was minus 4% in the second quarter.

The real problems show up below the gross profit level, though. Given retail prices of around 450,000 yuan for the flagship ES8, the numbers are astonishing. Per-car R&D came to an additional 366,000 yuan; sales, general & administrative costs were 400,000 yuan on top of that. Together with its cost of sales, NIO is shelling out around 1.27 million yuan each for a vehicle that sells for barely a third as much.

If anything, that situation is likely to get worse in the months ahead. NIO’s answer to the Tesla Model 3 – a car aimed at a more mass-market audience, with a lower price that erodes what little margin its costlier predecessors could claim – went on sale in June in the form of the ES6, with prices starting at 360,000 yuan. Government subsidies that amounted to 67,500 yuan per car last year have been staged down to 11,520 yuan. The result is that an ES6 bought now is only marginally cheaper than a fancier ES8 purchased last year.

How can NIO turn this around? R&D should be treated as a down payment on future sales, so it’s to be expected that it makes up an oversize share of costs at the startup stage. The same can’t be said of SG&A, though. You could buy a very nice car for the roughly $57,000 of overhead on each vehicle sold in the second quarter. Based on 2018’s annual results only about a fifth of that is going on marketing (another expense that might be abnormally high at the startup stage).

Eye-watering staff costs are a standout. NIO spent 4.11 billion yuan last year paying a workforce that reached 9,900 people in January. That averages out at compensation of 415,000 yuan per employee, more than three times the average white-collar salary in China’s tier-one cities. Plans to cut headcount to a target of 7,800 next week look like moving around the deckchairs on the Titanic.

NIO’s unique selling point has always been that it could provide luxury electric vehicles in China at a price well below foreign SUV competitors. The problem is, the discount doesn’t appear to come from operational efficiencies, but from losing money on every car.

The overhead is so immense that even were NIO to slash costs far more drastically than it’s anticipating and increase volumes dramatically – a bold bet, given the weakness in China’s car market and the reputational hit from its battery recall – there’s no clear path to profit. In the meantime, premium electric SUVs such as Daimler AG’s EQC and Volkswagen AG’s Audi e-tron will come to the market within months.

Like WeWork, NIO was never really the capital-efficient technology company it purported to be. Instead, it was a brief attempt to carve out a space in the middle of the market by the very old-fashioned technique of selling at a loss. The crash could now be coming sooner rather than later.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.