New York’s MTA Is Saved Less by Fed and More by Kroll

(Bloomberg Opinion) -- New York’s Metropolitan Transportation Authority became the second municipal-bond issuer to tap the Federal Reserve’s $500 billion emergency lending facility for state and local governments, locking in cheaper borrowing costs than if it had stuck with Wall Street.

But before crediting Fed Chair Jerome Powell and his colleagues for providing the MTA with more affordable funding, the state, city and subway riders alike might want to thank Kroll Bond Rating Agency.

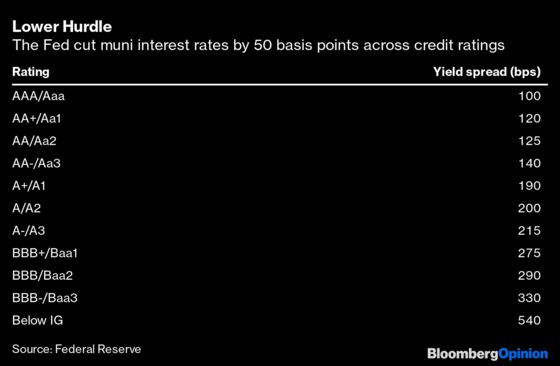

Bloomberg News’s Amanda Albright and Danielle Moran reported that the Fed’s Municipal Liquidity Facility charged a true interest cost of 1.92% to buy the MTA’s $450.7 million of notes, a savings of more than 85 basis points relative to its attempted auction earlier in the public market. Given the pricing scale from the central bank, which was tightened last week by 50 basis points, the MTA’s rate implies it was given a composite rating of A+. That grade requires a 190-basis-point yield spread to overnight index swaps, which are near zero.

According to the Fed’s term sheet, the facility determines pricing for split ratings by calculating an average among grades from “major nationally recognized statistical rating organizations.” And “for purposes of the MLF, ‘major NRSRO’ means S&P Global Ratings, Moody’s Investor Service, Inc., Fitch Ratings, Inc., and Kroll Bond Rating Agency, Inc.”

To put it plainly, including Kroll as one of the four accepted credit-rating companies ended up saving the MTA millions of dollars. While the agency’s transportation revenue bonds are rated BBB+ by S&P, A2 by Moody’s and A+ by Fitch, Kroll assigns them its second-highest grade: AA+. (For context, this is the same rating S&P gives the United States.) Without Kroll’s lift, the MTA would most likely have had to pay 10 to 25 basis points more to borrow from the Fed.

The MTA is the largest U.S. transit system and has been ravaged by the coronavirus shutdowns. It’s now confronting a $16.2 billion deficit related to the pandemic as New Yorkers largely stay away from public transportation. Even after the successful deal with the Fed, MTA Chief Executive Officer Patrick Foye reiterated the need for $12 billion of federal funding in an emailed statement to Bloomberg News. One key feature of the agency is it can’t legally go bankrupt, as I wrote in June, meaning that one way or another, either the federal, state or city government (or all three) will have to pay up. It’s a chief reason Michael Rinaldi, Fitch’s lead analyst on the MTA, stood by its comparatively higher rating relative to S&P and Moody’s.

Kroll, for its part, has the MTA’s AA+ rating on review for downgrade. On the positive side, “management has a strong track record of balancing its operating budget over changing economic cycles and unforeseen events as well as managing complex capital programs designed to improve and expand the system,” analysts wrote in July. Still, “the Covid-19 crisis presents unprecedented challenges to the MTA’s fiscal operations.”

There’s no denying that a AA+ rating seems high for the MTA, given its projected budget gap. But I’m not going to say one grade is right and the other is wrong — they’re opinions, after all. I just come back to what Jim Nadler, president of Kroll, told me several years ago about “the curse of a new rating agency.”

“No one is going to add a fourth rating that is lower,” he said in 2014. “You’ll never see the ones that we turn away or gave lower ratings to.” Years later, it was still struggling to gain widespread traction in the $3.9 trillion muni market.

For the MTA’s sake, it was a good thing Kroll’s analysis came up with a higher rating than its rivals. Without a clear indication that federal funding is on the way, the agency could resort to using the Fed’s facility again. According to the term sheet, the central bank can buy notes up to “20% of the gross revenue as reported in the audited financial statements” for fiscal year 2019. The MTA’s website said it took in about $16.7 billion last year, implying it could borrow roughly $3.3 billion from the Municipal Liquidity Facility in total if necessary.

MTA officials will hope federal aid comes through before it needs to borrow again. Meanwhile, the Fed’s pricing scale is still probably too steep for any other issuers aside from Illinois, which tapped the facility in June. Still, the MTA has shown the Fed’s muni backstop works in cases of extreme stress. In this instance, with an assist from Kroll.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.