(Bloomberg Opinion) -- Netflix Inc. could be a rising star in the bond market. But it shouldn’t necessarily want to be one just yet.

In the parlance of credit-rating firms, investment-grade companies that are cut to junk are deemed “fallen angels.” The phrase was thrown around frequently before the coronavirus pandemic, given that hundreds of billions of dollars worth of corporate debt was one wrong step away from speculative grade. Unsurprisingly, this year’s economic crisis has tripped up household names such as Ford Motor Co., Kraft Heinz Co. and Macy’s Inc., each of which was flagged as a risk well before anyone knew the term Covid-19. S&P Global Ratings said this week that a record 126 issuers remain potential fallen angels, with 20 facing immediate downgrade pressure.

A lesser-known distinction is the flip side: when a junk-rated company is lifted into the ranks of investment-grade borrowers. Known as “rising stars,” S&P anticipates the fewest such upgrades since at least 1987, when they began tracking the data. Since February, not a single U.S. company has made the leap, which is hardly surprising given the widespread damage to the U.S. economy.

Which brings us to Netflix. Unlike the vast majority of businesses, stay-at-home orders and social distancing have been a boon to its bottom line. For those who missed its second-quarter results last week, the company added a whopping 10.1 million subscribers and produced $899 million in free cash flow — a figure that is normally negative, not positive. The higher-than-expected rate of subscriber growth, coupled with lower costs from a halt in the production of shows, has Netflix on track to potentially post positive free cash flow for the entire year, disproving conventional wisdom that an economic downturn would run out the clock on its debt-fueled content binge.

The company’s cash position was so surprisingly strong that Bloomberg Intelligence’s Stephen Flynn and Suborna Panja suggested in a report this week that by the time Netflix taps the bond market again, it might do so as an investment-grade company. Its leverage is poised to fall further below higher-graded peers like Comcast Corp., while its business model is more resistant to the coronavirus than that of Walt Disney Co. With just $1.2 billion of debt due over the next three years, Netflix could stretch its $7 billion cash haul through 2021 until it reaches steady positive free cash flow — a clean bill of health for bond investors and credit-rating companies alike.

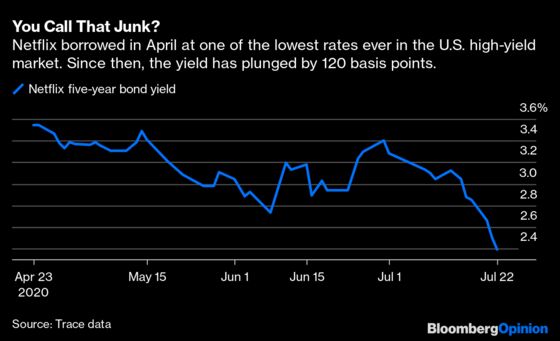

However, it’s not clear that wowing the bond market should be Netflix’s top priority. Of course, all else being equal, having an investment-grade rating is better than not having one. But the company sold $500 million of bonds in April at a yield of 3.625%, one of the lowest rates ever in the U.S. high-yield bond market and just a handful of basis points more than the average yield on a Bloomberg Barclays index of triple-B debt. Those five-year notes traded at a paltry 2.34% this week. Clearly, Netflix has already won over Wall Street, investment grades or not.

The one thing that could derail Netflix’s momentum is if it were seen as falling behind in the streaming race, rather than solidifying its spot at the front of the pack. Netflix, Disney and others with the means are in it for the long haul, for there won’t be one final winner but rather a set of companies that compete in some degree of perpetuity. This will require significant, continuing investment in new content — a finite resource because Covid-19 forced a stop to production.

Netflix’s current advantage is that it has enough programming to roll out this year, which should prevent subscribers from canceling in droves of boredom. One of its latest hits was “The Old Guard,” a sci-fi action movie starring Charlize Theron, which may be one of few big films released by Hollywood this summer as theaters remain closed. A light traditional fall television season may also push more cable customers to try out streaming services. It’s time for the company to push its advantage and build its programming war chest even more, not slow down.

Of course, that’s long been Netflix’s strategy: add new users and largely dismiss its cash bonfire, even as the flames shot as high as $3.3 billion in negative free cash flow in 2019. It has paid off; its shares are up about 50% this year, and it has added nearly 26 million customers in the pandemic so far. The company projects its free cash flow will dip back into negative territory next year as Hollywood gets back to work, though it mentioned that its “need for external financing is diminishing.”

The fact that Netflix could stop issuing junk bonds is likely enough to keep its borrowing costs near record lows for a speculative-grade company. In April 2019, it was fair to doubt Chief Executive Officer Reed Hastings when he said that “our message to debt investors is you better get in soon, because it’s not going to be that much more to go.” That’s a much more realistic scenario now, though it would be a mistake for the company to dismiss cheap financing just because it’s not burning through cash. It’s better to raise money when you can than when you need to.

The peculiarities of this recession may forever change some of the most time-tested, resilient entertainment businesses. Netflix is no longer a place to watch cable reruns. It may turn to licensed content to help bridge the Covid-19 production gap, but it’s a studio in its own right. It has to be, given that its former partners have turned into direct rivals. It would be smart to stay the course, focusing on adding customers and keeping them happy so it maintains its standing as the must-have subscription — the one viewers keep while switching between other supplemental offerings.

Succeed in that strategy, even if it’s costly in the short run, and the coveted “rising star” label will surely follow.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

Tara Lachapelle is a Bloomberg Opinion columnist covering the business of entertainment and telecommunications, as well as broader deals. She previously wrote an M&A column for Bloomberg News.

©2020 Bloomberg L.P.