Fake Meat, Coffee or Sparkling Water? Nestle’s Next Moves Matter

(Bloomberg Opinion) -- Nestle SA Chief Executive Officer Mark Schneider is in a good spot. He’s on the verge of capping what he set out to do when he became the Swiss food behemoth’s first outside leader for almost 100 years.

Nestle is on track to meet its target for operating margin a year early. Its organic sales growth goal for next year looks attainable. And on Thursday the company unveiled plans to return another $20 billion to shareholders by 2022. That is unless it can find better ways to spend some of the money on acquisitions.

The latest buyback comes just as the last $20 billion capital return — announced in June 2017 — is being completed.

The German-American CEO took over in January 2017 with the aim of making changes. He received a blessing in disguise that June, when activist investor Dan Loeb’s Third Point bought a stake and started agitating for change, giving Schneider the license to move quickly.

Under pressure from Loeb, he has changed up of 9% of Nestle’s the portfolio so far, in line with his plan to trade 10% of it by the end of 2020. He has sold off the U.S. confectionery business, the Gerber life assurance unit and most recently the dermatology arm, all for better-than-expected prices.

And he has made canny acquisitions, including spending $7 billion for the rights to market Starbucks Corp. products outside of its cafes, which is helping drive growth in Nestle’s coffee unit. Adding Sweet Earth, which makes meat substitutes, also looks smart given the boom in plant-based protein products.

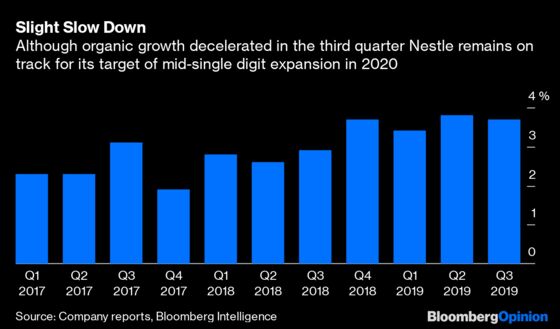

Combined, the moves mean Nestle is on track to meet the low end of the target for full-year underlying operating margin of between 17.5% and 18.5% in 2020, a year early. Organic growth in the mid-single digits by 2020 looks possible, too. Nestle forecasts about 3.5% expansion in 2019.

But from here, life gets tougher. Obvious disposals have been made, although Schneider could go further in pruning parts of the U.S. frozen food business, which includes Hot Pockets and DiGiorno pizzas, and its joint ventures in chilled dairy, cereals and ice cream.

The decision to no longer run the challenged waters arm as a separate business and instead integrate it into Nestle’s three main geographic regions indicates that that business won’t come up for sale in its entirety.

Nestle believes its range of waters, which include the Perrier and S.Pellegrino brands, are capable of delivering strong growth, thanks to demand in emerging markets and the trend for health and wellness in developed regions. But staying so committed to the business looks like a rare strategic misstep, given the pressures on the lower end of the market and growing environmental awareness.

As for further acquisitions, more bolt-ons that take Nestle into nascent but potentially fast-growing consumer categories along the lines of fake meat, look likely given the creation of a unit to bolster expansion both within the group and outside of it.

There is one portfolio change that seems to remain stubbornly out of Schneider’s plans: selling Nestle’s 32 billion–euro ($35.6 billion) stake in L’Oreal SA, the world’s biggest maker of beauty products.

Loeb has been pressing to offload it. Nestle doesn’t need the money, and would prefer to link any change to a big strategic move. But there is merit in considering the disposal. Concern is rising about a slow-down in luxury demand in China, something that has been buoying L’Oreal’s premium cosmetics brands. Meanwhile, the U.S. make-up market looks more challenging after a boom. If conditions deteriorate, Nestle may have missed the best chance to extract maximum value.

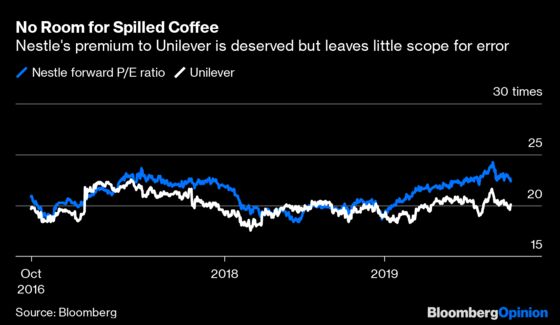

And it can’t afford any slip ups. The shares have risen 44% since Schneider arrived in January 2017, and trade at a forward price earnings ratio of 22 times. While the premium to Unilever NV is deserved, at this elevated valuation, there is less room for error than when Schneider walked in to shake up what was then a lumbering food giant.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.