(Bloomberg Opinion) -- In two and a half years, Nestle SA chief executive Mark Schneider has gone from zero to hero.

An outsider faced with the monumental task of tuning Nestle into consumers’ changing tastes, he initially underwhelmed when he set out his vision for the Swiss group in early 2017.

But since then, he has shown that his aim of steering Nestle between two extremes – top line growth with little profit expansion and the pursuit of fatter margins without the revenue increase to match – is the right one. He’s supplemented this with canny acquisitions and disposals at better-than-expected prices.

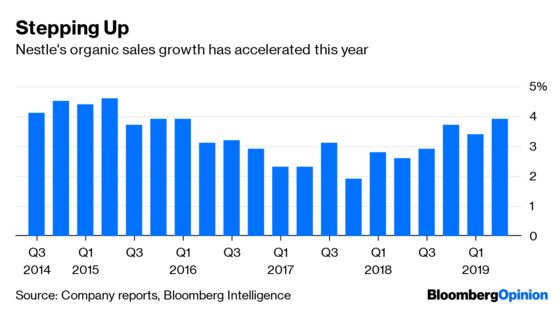

The second quarter of 2019 continued the progress, with organic sales growth of 3.9%, an acceleration from the first three months. The underlying operating margin also rose by a percentage point to 17.1%. The U.S. was particularly strong, helped by Nestle’s focus on coffee, including Nespresso and now the Starbucks brand, along with pet food.

The mystery is why Nestle has kept its guidance for the full year so conservative.

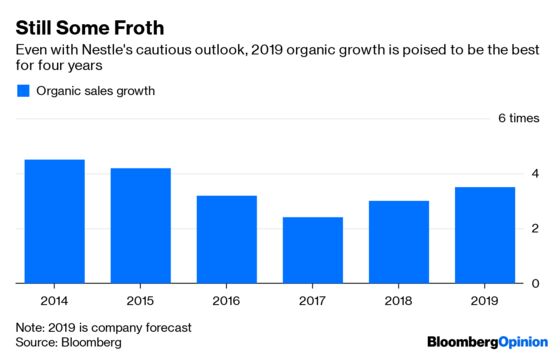

The company forecasts full-year organic sales growth of around 3.5%. Although that would be the best performance since 2015, the consensus of analysts’ forecasts was already for a 3.7% increase, so this looks a bit light.

The full-year operating margin is on track to reach the lower end of the 17.5-18.5% range it wants to achieve in 2020. Though that will enable the company to meet its profitability target a year early, given how impressive the increase was in the first half that doesn't look too ambitious either.

There are reasons why Nestle may want to be cautious.

Firstly, the company was able to raise prices in the first half, particularly in the U.S. It may not be able to achieve the same level of pricing power over the coming months.

Secondly, commodity costs are expected to rise this year. This wasn’t as much of a problem as had been feared in the first half. But an acceleration could crimp the potential for more aggressive margin expansion.

And finally, Nestle faces tough comparisons, particularly in the final quarter, when it enjoyed a bump in organic sales growth.

But perhaps Schneider, who has made the middle course his mantra, just wants to under-promise and over-deliver.

The shares are up 42% since he took over, and reached a record high on Friday.

At this valuation, he can’t afford any stumbles. Activist investor Dan Loeb’s Third Point also continues to be a shareholder. Schneider has done many of the things he was urging, such as improving profitability and overhauling the portfolio, so Loeb can’t have much to complain about right now.

But any downturn in performance would give him scope to agitate for more change. This could include pushing the company harder to offload its stake in L’Oreal SA, something Nestle has long opposed.

Given the uncertainties ahead, Schneider is right to keep his Nespresso coffee lukewarm for now.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.