Neil Woodford's Star Implodes in a Liquidity Crunch

(Bloomberg Opinion) -- All political lives end in failure, Conservative politician Enoch Powell once remarked. Neil Woodford’s decision to freeze his flagship equity fund suggests stock pickers will struggle to escape a similar fate in the era of passive funds and computer-enhanced trading strategies.

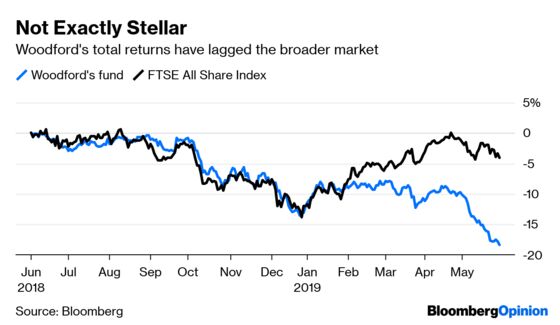

Late on Monday, Woodford’s firm announced that it was stopping investors from withdrawing money from the LF Woodford Equity Income Fund. The pool had shrunk by 560 million pounds ($709 million) last month as the value of its holdings dropped and investors headed for the door. The decision leaves about 3.8 billion pounds trapped in a woefully underperforming portfolio.

It wasn’t Woodford’s over-optimism about the U.K.’s economic performance after Brexit and focus on domestically concentrated stocks that he regarded as unjustifiably unloved that proved to be his undoing. Yes, the 41 percent slump in shares of Kier Group Plc following a profit warning on Monday will have been painful – Woodford owned about 10 percent of the British construction company – but it wasn’t terminal.

The bigger problem was his fondness for illiquid stakes in closely held companies. As outflows mounted, he struggled to liquidate those holdings to meet redemption requests.

As the value of Woodford’s listed equities shrank, the proportion of his fund allocated to unlisted investments clearly risked breaching the Financial Conduct Authority’s 10 percent limit on such hard-to-sell, hard-to-value holdings. Hopefully, the regulator has been on top of the situation throughout the star fund manager’s fall from grace.

But some fancy footwork in March involving the transfer of some of the fund’s unlisted holdings to the Woodford Patient Capital Trust, which in turn is part of the equity fund’s portfolio, raised eyebrows at the time. Similarly, Woodford’s listing of his fund’s shares in biotech company BenevolentAI on the Guernsey International Stock Exchange – with no free float – and similar listings of tech company Ombu Group Ltd. and Industrial Heat, look like financial engineering that plays fast and loose with the definition of what counts as a liquid investment.

Woodford isn’t the first fund manager to struggle to cope with investor outflows in a less-than-liquid portfolio. In the wake of the June 2016 vote for Britain to leave the European Union, seven U.K. property funds with about 18 billion pounds of assets were forced to suspend trading amid a wave of redemption requests from spooked investors. Swiss fund manager GAM Holding AG has spent almost a year unwinding its Absolute Return Fund after it suspended portfolio manager Tim Haywood in mid-2018.

Woodford’s move leaves at least one of his backers licking its wounds. Kent County Council, which had 255 million pounds of its pension plan invested with him at the end of last year, was scheduled to decide whether to pull that money on June 21, Financial News reported last month. Instead, the council met on Friday and decided to withdraw its cash, according to the Financial Times. It’s not clear whether the U.K. council managed to get out of the fund before the gates came down.

Kent had about 5.8 billion pounds in its pension program at the end of last year, and 135,000 members. Why a local authority chose to risk a substantial chunk of its assets in a concentrated strategy such as the one Woodford was running – a quarter of his fund was invested in just five stocks at the end of April, including almost 13 percent in U.K. homebuilders Barratt Developments Plc and Taylor Wimpey Plc – might well end up being a question for regulators.

Woodford’s efforts to rejig his illiquid investments bought him some time, but not enough. His enthusiasm for U.K.-focused companies may yet turn out to be justified. But as John Maynard Keynes opined, “the market can stay irrational longer than you can remain solvent.”

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.