(Bloomberg Opinion) -- The demise of Neil Woodford, booted from managing his eponymous fund after almost two years of monthly withdrawals led to redemptions being suspended, bangs another nail into the coffin of active asset management. Given the data, it’s hard to feel much sympathy for him or his industry.

Link Fund Solutions, the fund’s administrator, said on Tuesday it was hiring Blackrock Inc. to liquidate the portfolio. Woodford’s reaction suggests he’s still in denial: “This was Link’s decision and one I cannot accept, nor believe, is in the long-term interests of LF Woodford Equity Income Fund investors.”

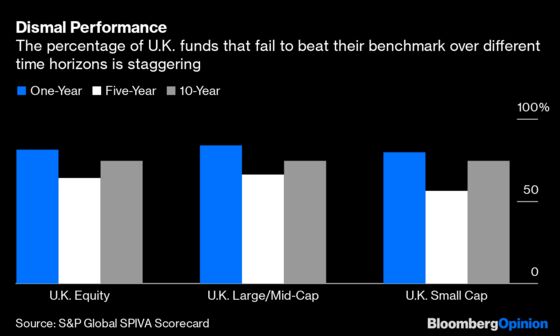

The stark truth is that stock-pickers have failed to justify their fees in recent years, failing to beat the benchmarks against which their performance is measured. As data compiled by S&P Global show, 90% of active funds across Europe delivered inferior returns to their index-tracking competitors in the year to June. British funds didn’t do much better, with more than half of them beaten by their benchmarks over one-, five- and 10-year periods.

What about the argument that stock market performance has been unusually buoyant in recent years and that times are about to get tougher, providing an environment in which the true worth of stock-pickers will shine through? Here’s what Andrew Innes of S&P has to say:

“The steep declines across equity markets in late 2018 were accompanied by broad under-performance across many active funds in Europe. This defied conventional belief that active managers tend to have an advantage in volatile markets. Despite markets improving in the first half of 2019, active managers were generally not able to make up for lost ground.”

So it’s not just Woodford — who made his name successfully running funds at Invesco Ltd. before striking out on his own — who’s been found wanting. Dismal returns in recent years prompted him to shift more capital into smaller stocks; and their relative lack of liquidity tripped him up when too many investors demanded their money back at once, leading to his fund being gated in June.

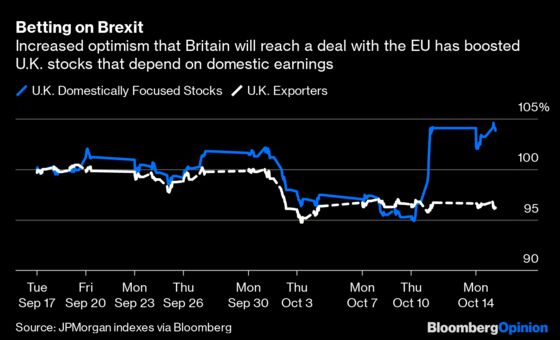

As (poor) luck would have it, Woodford’s ousting comes just as his faith in battered stocks dependent on the U.K. economy starts to come good:

But it’s too little, too late. Woodford will probably be ousted too from his listed investment vehicle, Woodford Patient Capital Trust, which is trading at an all-time low. His storied rise and fall is a terrible advertisement for the alleged benefits of active management. The sellers of exchange-traded funds, index trackers and other low-cost passive products will be rubbing their hands in glee.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.