(Bloomberg Opinion) -- With almost $13 trillion of bonds in the global debt market yielding less than zero, fund managers are increasingly chasing returns in less liquid assets. The result could be a reduction in the transparency about what portfolios are really worth. Regulators are right to be paying heightened attention to any misadventures in illiquidity.

The decline in interest income available in the global bond market – even on securities that haven’t yet breached the zero bound – is truly staggering. The average yield on the world’s $54 trillion of investment grade debt is a paltry 1.5%, down from 9% at the start of 1990 and about half of its average since then.

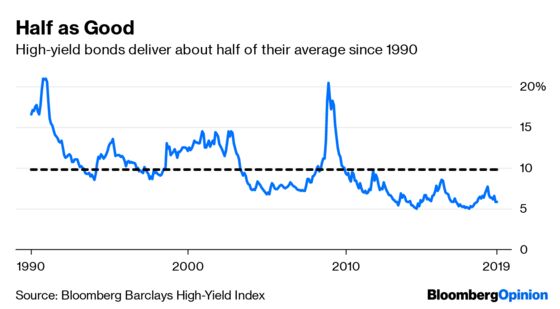

The high-yield debt market looks increasingly misnamed. $2.4 trillion of the low-rated bonds yield less than 6%, down from as much as 21% in 1990 and an average of almost 10% during the past two decades or so.

The world’s stock market, as measured by the MSCI World Index, is within touching distance of a record high – even as the prospect of a synchronized global economic slowdown is forcing central banks to turn on the monetary spigots once again. So investors are understandably a bit nervous about the prospect for further gains in public equities, and are turning increasingly to private markets, which supposedly offer higher rewards in return for less liquidity.

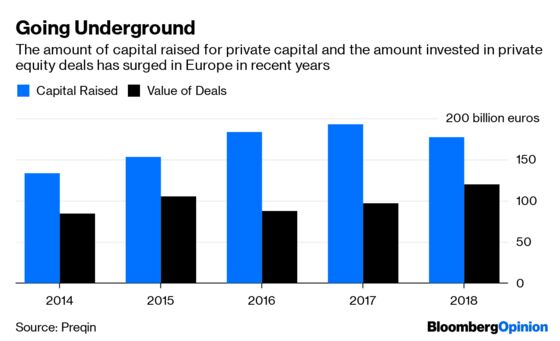

In Europe, private equity is poised to overtake hedge funds as the dominant asset class in the so-called alternatives space, according to a report published earlier this month by Amundi SA, Europe’s biggest independent asset manager, and research firm Preqin. Aggregate investment in private equity has grown by 25% since the end of 2015, reaching 559 billion euros ($628 billion) by the middle of last year.

The total capital allocated to all flavors of private equity last year, including infrastructure, private debt and venture capital, climbed to a record 374 billion euros. And with 56 billion euros raised in Europe for private investments in the first quarter, 2019 is on track to set a fundraising record, the study said.

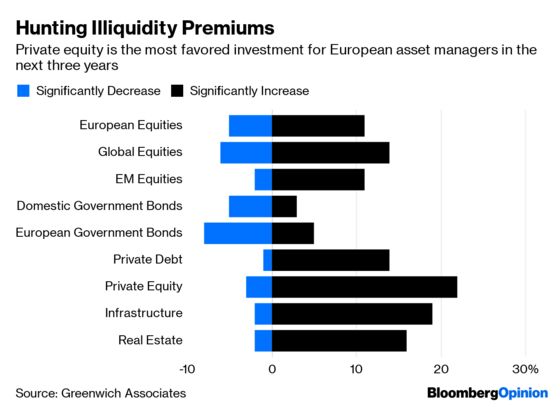

That shift away from public markets shows no signs of stopping. A survey of more than 550 European investment firms published by Greenwich Associates earlier this week shows private equity is the most-favored investment destination in the coming three years. Moreover, the survey showed European institutional investors are twice as likely to hire a new private equity specialist in the coming year as they are to recruit a public equities portfolio manager.

The danger here is that unlisted investments are effectively worth whatever the fund manager says they are – unless and until they have to find a buyer, either voluntarily or compulsorily. And that’s worrying.

“Illiquid assets are not marked to market,” the Greenwich report notes. “As a result, changes in valuation take longer to play out in institutional portfolios, muting quarter-to-quarter volatility in portfolio valuations and funding ratios.”

The pivot toward private markets is an understandable response to the worldwide drop in yields. But higher returns necessarily come by taking on increased risks. Clients and regulators alike should be wary of allowing asset managers too much leeway in the values they assign to unlisted assets. Regulators have every reason to look closely.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.