Central Banks Can't Create Negative Rates by Themselves

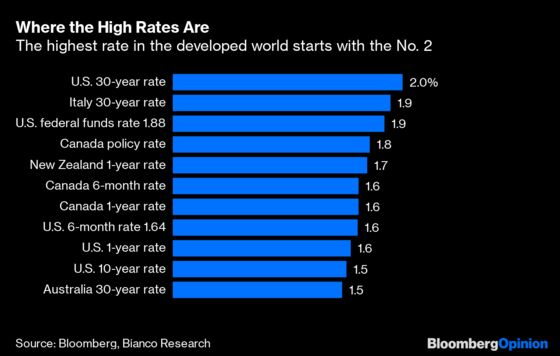

(Bloomberg Opinion) -- It’s been a decade since the worst financial crisis since the Great Depression, and yet here we are in a world where the highest government bond yield starts with the number “2.” Among the world’s major developed economies, only the English speaking countries – the U.S., U.K., Canada, New Zealand and Australia - still have monetary policy rates above zero. But there is more to low yields than monetary policy rates, and those factors are likely to stay in place for an extended period.

The following table shows the highest interest rates culled from the 20 largest developed countries from the policy rate to the 30-year bond. Over 200 interest rates were considered and the only one to yield above 2% is the 30-year U.S. Treasury bond at 2.04%. Never has the highest yield among these countries been so low.

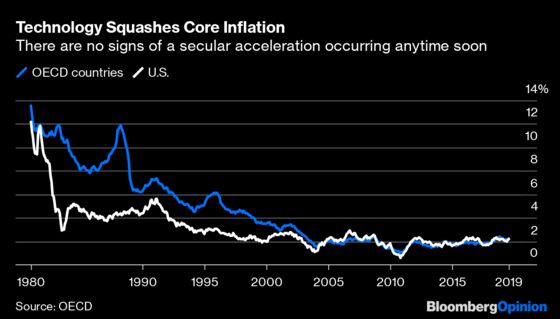

Start with technology, whose effect has been to make companies more efficient and competitive on prices. So much so that core inflation is considered high if it reaches a 2% rate. Think about how smart phones have reduced the need to buy a separate camera or other devices, websites that make searching for a job or seeking qualified job candidates far more efficient, or the falling price of computing power enabling Charles Schwab Corp., E*Trade Financial Corp., and TD Ameritrade Holding Corp. to announce last week that they are eliminating commissions.

Core inflation has been low and stable for 15 years and shows no signs of a secular acceleration anytime soon. Low rates of inflation mean interest rates should be in the low single digits. Without a serious return of developed world inflation, which has not been the case for almost 25 years, gone are the days of 4% to 6% yields without a crisis, like the one in Europe’s government debt market around 2012.

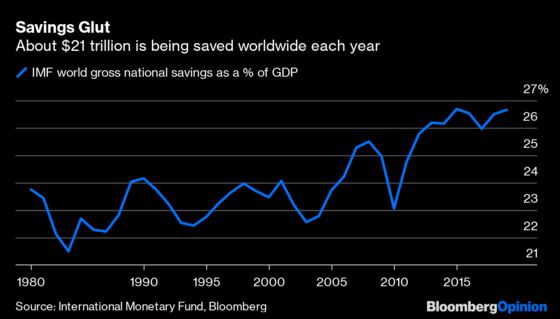

Next is the global savings glut, a phrase coined by former Federal Reserve Chairman Ben S. Bernanke in 2005. As populations age, they have a propensity to save. This is shown by the following chart from the International Monetary Fund. Note that prior to 2005, the global saving rate was never above 24.5%. Since then, it’s only been lower during the panic of 2009. The rate equaled its record high of 26.7% in 2018. This works out to roughly $21 trillion saved every year. Since many seek to match the investments in their savings to their life expectancies, they tend buy bonds.

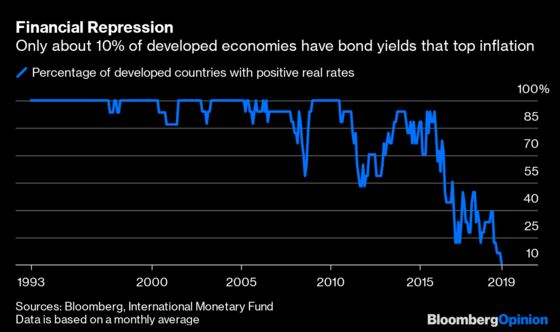

The savings glut is leading to massive bond buying that is resulting in yields dropping below the inflation rate nearly everywhere in the developed world. How unusual is this? As the next chart shows, it is unprecedented in the last quarter century. Only two countries in the developed world have real 10-year yields above zero: Portugal and Italy. Everywhere else, older people are buying bonds and driving yields below the technology-inspired depression in the inflation rate. Demographics tells us the developed world is not running out of old people anytime soon. The savings glut will continue.

The two factors above alone should be enough to make investors understand that the fair value for developed world yields now start with a “1” or “0,” but two other factors are driving yields even lower, and into negative territory.

One is the global flight-to-quality. As the world economy slows, the natural reaction is to allocate into safe fixed-income securities. Look no further than last week’s reaction to the poor manufacturing data in the U.S. Bonds rallied and equities slid. Yes, flight-to-quality is a cyclical factor that is present when the concern is about a slowing world economy. So, expect this factor to come and go over time. Right now, though, it is “coming.” This flight-to-quality has created to much demand for bonds that the amount of negative yielding debt increased by $8 trillion this year to $14 trillion.

Yes, central banks might reverse from their negative interest-rate policies, but that only means developed world rates, without a crisis, will only go up to 1% or maybe 2%. Every future downturn will add back in flight-to-quality buying and negative central bank rates, and down market rates will go again to zero or even lower.

The secular outlook has changed and those applying the thinking from previous economic cycles about inflation and real yields conclude these low yields represent a bubble. They are not considering aging populations that are buying bonds and pushing yields below inflation rates driven lower by advances in technology. Add aggressive central banks willing to take monetary policy rates into negative territory and the standard rules that say bubble have not worked for almost a decade. Don’t expect this to change anytime soon.

The most commonly asked question from U.S. investors is where they can find yield. Unfortunately, for those still hoping for a previous cycle to return, we have bad news, you have it now at 1%. Embrace it and be lucky U.S. yields are not negative - yet.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Jim Bianco is the President and founder of Bianco Research, a provider of data-driven insights into the global economy and financial markets. He may have a stake in the areas he writes about.

©2019 Bloomberg L.P.