Napping Spanish Dealmaker Nears The End of Its Siesta

(Bloomberg Opinion) -- Is Telefonica SA ready to return to its acquisitive ways? Almost.

Since Jose Maria Alvarez-Pallete was promoted from operations chief to the joint chief executive and chairman role in 2016, the focus at Spain’s former national carrier has been debt reduction. And quite rightly, too – he inherited one of the biggest debt piles in Europe.

He has sold businesses in Latin America, stakes in the cell towers unit, and other businesses not considered central, raising at least 2.5 billion euros ($2.8 billion), according to data compiled by Bloomberg. Operating income before depreciation and amortization, the company’s preferred earnings measure, hit 8.7 billion euros in the first six months of this year, up 12% from three years ago. Net debt has fallen below 40 billion euros for the first time in more than a decade.

But historically Telefonica has been a voracious acquirer. In the decade before Alvarez-Pallete took the reins, it spent some 26 billion euros investing in operators from Brazil to Italy. And that excludes its majority-owned subsidiary Telefonica Deutschland AG’s 8.6-billion-euro acquisition of KPN NV’s German operations in 2013.

While acquisitions on that sort of scale would still ask a lot from investors, there’s the possibility of some smaller deals. Changes in the telecoms landscape have made Telefonica’s debt pile more acceptable: the trajectory of its biggest rivals mean it looks a lot more frugal.

That’s because the dealmaking of two other European telecoms giants, Vodafone Group Plc and Deutsche Telekom AG, has stretched their debt exposure to levels similar to those of Telefonica. Vodafone is awaiting the completion of its 18.4 billion-euro acquisition of Liberty Global Plc’s German and Eastern European operations, while Deutsche Telekom is hoping its U.S. unit’s $57.8 billion deal for Sprint Corp. secures regulatory approval soon.

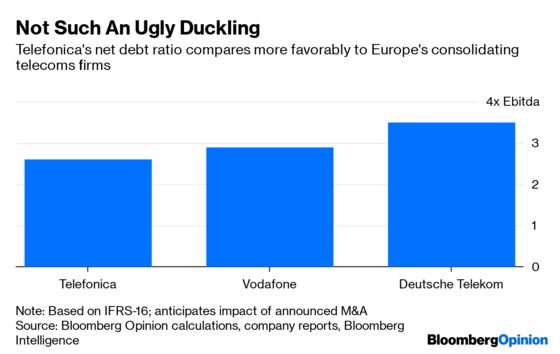

Although the Spanish firm hasn’t yet reported its net debt ratios according to the most recent accounting standards, it’s likely to be somewhere close to 2.8 times Ebitda. That’s below Vodafone’s 2.9 times, and similar to the level around which Bloomberg Intelligence analyst Aidan Cheslin expects Deutsche Telekom to land following the Sprint takeover. And Telefonica’s capital costs are less than Vodafone’s.

Assuming that the Spanish firm’s debt pile continues to shrink as we head towards 2020, it could feasibly start looking at deals in adjacent markets where it would be easy to execute operational synergies. Investment bankers would also love a tie-up with Liberty’s U.K. cable business, Virgin Media, but it’s hard to see how Telefonica could be the consolidator in such a deal without some very creative financing. Portugal’s NOS SGPS S.A., with a market capitalization of some 3 billion euros, might be more in the realms of possibility.

For his part, Alvarez-Pallete seemed to indicate that Telefonica is ready to end the era of divestments. The firm no longer needs to sell businesses solely to reduce its debt pile, he intimated to analysts in a conference call on Thursday. Perhaps he's ready to return to the consolidator role.

The company probably isn’t there just yet. But it’s likely to have the firepower in the not too distant future if it maintains the current path.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.