Muni Bonds Go Wild. Could 1% 10-Year Yields Be Far Behind?

(Bloomberg Opinion) -- The $3.8 trillion U.S. municipal bond market, sometimes called a sleepy asset class, has been partying awfully hard lately.

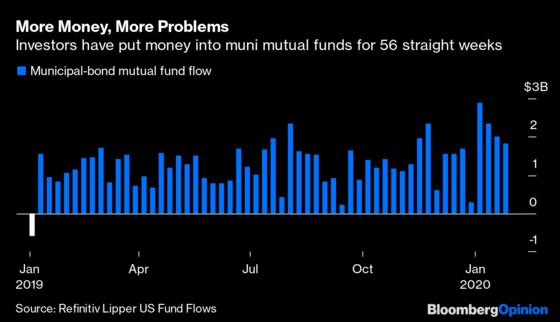

Consider that investors poured $1.8 billion into muni mutual funds in the week through Jan. 29, the 56th consecutive week of inflows, according to Refinitiv Lipper US Fund Flows data. Then, on Jan. 31, the biggest high-yield muni exchange-traded fund, the VanEck Vectors High-Yield Municipal Index ETF, drew in $150.2 million, the largest one-day increase in assets since inception in 2009. The amount of state and local debt on the books of Wall Street banks has dwindled to the least since late 2014. Overall, the market returned 1.8% in January, its strongest month in six years.

That sort of performance is astounding, especially when considering the difference between January 2014 and last month. Because of the “taper tantrum” that started in mid-2013, benchmark triple-A muni yields climbed to 3% by the end of the year. That gave them some room to fall as the calendar turned. By contrast, triple-A munis ended 2019 at 1.48%, barely off their record lows. In theory, they had little room to run.

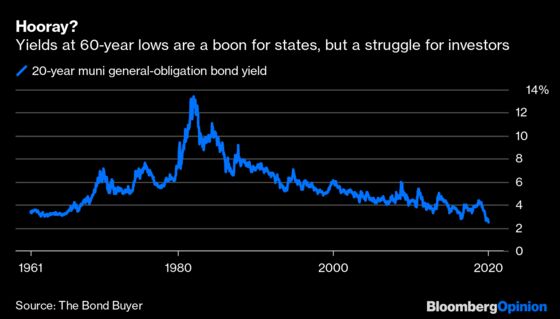

Instead, the spreading coronavirus and ensuing flight to haven assets caused munis to rally anew. The yield on top-rated 10-year debt fell to 1.18% on Jan. 31, the lowest since Bloomberg Valuation data begin in 2009, while yields on 10-year New York State general obligation bonds dropped even lower, to 1.09%. According to the Bond Buyer’s 20-year index of general-obligation bonds, the oldest gauge of the tax-exempt securities market, yields are the lowest since the mid-1950s. “That is insane,” one fund manager said.

Yes, it is insane. With the benchmark 10-year Treasury yield fluctuating around 1.5%, not far from its all-time low of 1.32%, fund managers and strategists are frequently asked whether they see 1% or 2% next. For munis, 1% is already close to becoming reality in what could be a harbinger for American investors.

Because interest on most state and local debt is exempt from income taxes, investors have historically accepted lower interest rates for munis than they have for Treasuries. For those in the top federal marginal tax bracket of 37%, a tax-free yield of 1.18% is equivalent to 1.87% on a taxable bond. In that sense, triple-A munis are still a better deal than Treasuries, though worse than top-rated U.S. corporate bonds, which yield about 2.3%.

The curious part of this relentless rally is that many muni investors fit the stereotype of those who would balk at psychological yield levels. Unlike, for example, traders who aim to front-run the European Central Bank by buying negative-yielding debt and selling it at an even-higher price, state and local obligations are often held until maturity by investors looking to cut down on their tax bills. Maybe they have become accustomed to yields below 2%, but less than 1% could be a bridge too far.

Most likely, muni investors are falling into the typical pattern of chasing returns rather than taking note of prevailing yield levels. The Bloomberg Barclays Municipal Bond Index has gained in every month but one since November 2018, which of course neatly lines up with the streak of mutual-fund inflows. “The ongoing intense, prolonged rally, has led to gluttonous demand for tax-exempt paper, which has engendered strong performance, and is leading to more gluttonous demand,” Citigroup Inc. analysts wrote this week in a report that suggested munis could gain about 8% in 2020.

While there’s nothing obvious on the horizon that would cause a jump in benchmark yields, certain relative-value metrics at least suggest the market has been stretched to its limits.

The traditional way to measure the relative attractiveness of munis is to divide tax-free yields by those of Treasuries. When that ratio is lower, it means munis are comparatively more expensive. That gauge for 10-year debt dipped to 72% last month, about the lowest in at least two decades. The ratio for 30-year bonds set a record low on Jan. 8.

Even a generic spread analysis tells a similar story. Ten-year Treasuries yielded 51 basis points more than similar maturity munis in mid-January, the most since July. Triple-A corporate bonds yielded 123 basis points more than triple-A munis on Jan. 8, the most since August. The fact that ratios have risen and spreads have narrowed in recent weeks shows munis have underperformed during the coronavirus-inspired risk-off push.

That’s at least some reprieve for a group of investors who haven’t exactly hid their exasperation. “Where’s the point where it stops making sense?” Debra Crovicz, a managing director at Chilton Investment Co., asked Bloomberg News’s Fola Akinnibi and Mallika Mitra. “We have the ability to add some corporate or even add some Treasuries as a placeholder, and that’s actually what we’re doing. I’ve been waiting for the market to give us a chance to buy at more attractive levels.”

As bond investors know all too well, though, waiting can be costly. As I wrote last week, many Wall Street strategists felt that a 1.6% yield on 10-year Treasuries was too low, given the economic backdrop. Yields haven’t managed to climb back to that mark in three trading sessions. So anyone who bought at that level is looking at a profit.

Those who bought munis in January could experience a similar rally beyond expectations. As of now, states and cities are poised to issue $13 billion of debt in the next 30 days. But investors will get back $38 billion in February just from principal and interest payments on bonds they currently own, Bloomberg News’s Martin Z. Braun reported this week, meaning reinvesting that cash would be enough to cover potential supply almost three times over. It’s telling when money managers groan about money: “It’s been really, really difficult.”

Whatever the endgame in the coming months, it probably won’t be pretty for investors. The best-performing part of the tax-free market, unsurprisingly, has been the longest-dated bonds rated below investment grade — in other words, those most sensitive to rising interest rates and most at risk of defaulting if the economic outlook sours. Some investors are trying to lock in better value by ditching tax-exempt debt altogether: Taxable munis returned 4.2% in January, the second-best month dating back to 2011. And benchmark muni yields are just a haven retreat away from 1%, providing lower income streams and a smaller buffer against rising interest rates or inflation.

Of course, the other way to look at this is that states and cities can lock in historically cheap rates for infrastructure projects or for refinancing existing obligations. That matters much more than the federal government’s borrowing costs, given that local officials don’t have the luxury of running budget deficits, huge or otherwise. I’ve even suggested that if used judiciously, shoring up public retirement systems with pension-obligation bonds might make sense for some states with yields this low.

For the health of the market, though, it feels as if munis need a breather. Going this far, this fast, is always risky for an asset class, particularly one that’s proved to be susceptible to small shifts in sentiment. Staying on cruise control would be just fine for investors and issuers alike.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.