(Bloomberg Opinion) -- It was a big week for financial markets. The S&P 500 Index rebounded from its worst weekly selloff since October to set another record as companies posted better-than-forecast earnings. Yields on U.S. Treasuries continued their slow march higher, with those on the benchmark 10-year note reaching their highest since March as the economy showed signs of improvement. Silver went on a roller-coaster ride as the Redditors took aim at the precious metal.

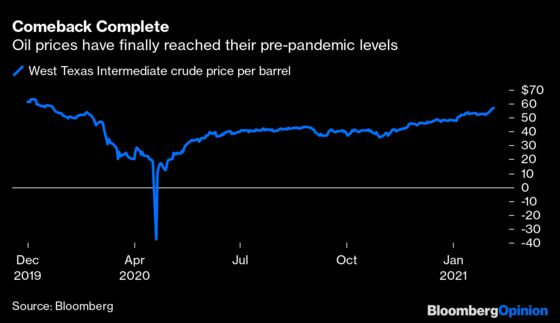

Not to diminish the importance of those moves, but perhaps the more meaningful action was in the oil markets, where the price of West Texas Intermediate crude soared to as high as $57.29 a barrel in intraday trading. Not only was the weekly increase of 9.16% the biggest since early October, but the price has finally recovered all of its pandemic-related losses. The move also comes amid a broader comeback in the markets for raw materials, with the Bloomberg Commodity Index reaching its highest since 2019.

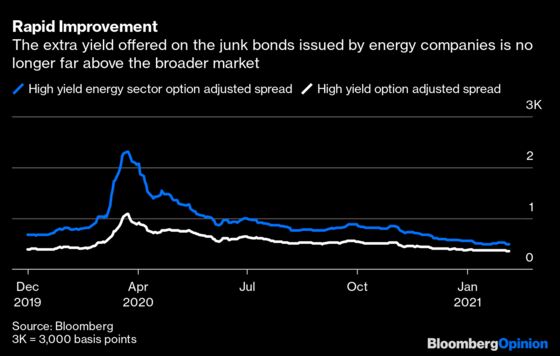

This is significant for a few reasons. The first is that it seems to ratify the moves in other asset classes that suggest the economy is on firmer footing and should only get stronger as President Joe Biden’s $1.9 trillion Covid-19 relief plan moves closer to reality. It will also help bolster the finances of energy-related companies, many of which were thought to be on the cusp of bankruptcy as travel and commuting came to a halt and oil prices collapsed in the early days of the pandemic, even briefly dropping far below zero on one crazy day in April.

As far as the positives go, those are about it. The reality is that there are far too many negative factors surrounding the oil rally to ignore, especially with the economy still needing a tremendous amount of support from the government and Federal Reserve.

Let’s start with the most glaring, which is that rising oil prices have less to do with demand than shrinking supplies. U.S. crude stockpiles fell by more than 4 million barrels last week, to the lowest since March, according to the American Petroleum Institute. At the same time, OPEC and its allies have been able stay true to their supply-cut agreement.

And while mobility has improved from the early days of the pandemic, it’s still muted. The percentage of workers who are back in the office in 10 of the largest U.S. business districts remains just under 25%, which is little changed from the beginning of the pandemic, according to data from Kastle Systems.

Most people remain wary of travel despite the start of vaccinations. American Airlines Group Inc. warned 13,000 employees this week that they could be laid off, many for the second time in six months, because an anticipated summer travel rebound isn’t materializing.

The rising price of oil means those who do venture out of the house are paying more to fill up their tanks. The average price for a gallon of regular-grade gasoline has surged to $2.456 a gallon from last year’s low of $1.768 in April, back to where it was pre-pandemic, according to the American Automobile Association.

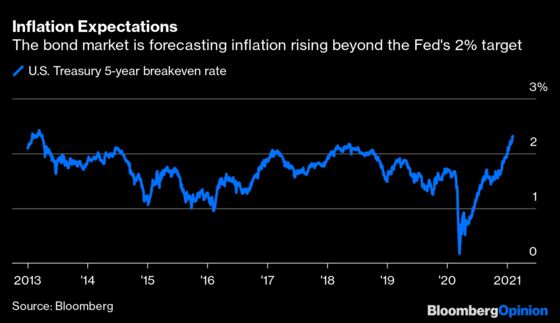

Higher gasoline prices should worry investors because they have the ability to make people think that faster inflation is coming. Breakeven rates on five-year Treasury notes, a measure of what traders expect the rate of inflation to be over the life of the securities, just surged to 2.29%, the highest since early 2013 and well above the Fed’s 2% target for inflation.

If inflation expectations translate into real inflation, it could become a serious problem for the bull market in stocks. The rally in equities has been predicated on the Fed keeping benchmark interest rates near zero well into 2022 while pumping $120 billion into the financial system each month to keep borrowing costs low. So any speculation that faster inflation may prompt the Fed to pull back on its easy money policies sooner than expected could lead investors to rethink the lofty valuations they now assign to equities.

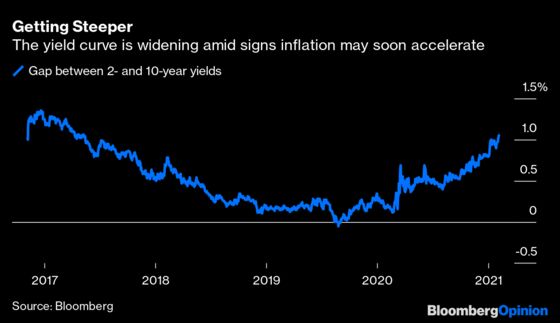

It’s not just one bond market metric that is sending a worrisome signal about faster inflation. The difference between short- and long-term yields, or the yield curve, is at its widest level since 2017. Longer-maturity debt tends to get hit the worst when inflation accelerates because rising consumer prices erode the value of a bond’s fixed payments over time. That’s why investors demand higher yields at the first sign of inflation, causing the yield curve to widen.

In markets, as in life, there can be too much of a good thing. The rally in oil is as good a sign as any that the economy is healing and better days are ahead. But there comes a point when rising prices start to send an ominous signal. It’s impossible to know right now whether the price of oil is near that point, but it’s worth asking some tough questions if the economic and mobility data don’t start showing marked improvement soon.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.