Morgan Stanley’s 126% Bond-Trading Surge Is Electric

(Bloomberg Opinion) -- Wall Street’s bond traders deserve a lot of credit for an impressive earnings season for the biggest U.S. banks. After all, fixed-income trading revenue easily blew past analysts’ estimates across the board.

But shareholders might want to show some respect to the machines, too.

Consider Morgan Stanley, which reported earnings on Thursday that were so impressive that its shares soared 7.6% when the stock market opened, the biggest intraday gain since November 2016. The bank, with a smaller fixed-income, currency and commodities desk than the likes of Bank of America Corp., Citigroup Inc., JPMorgan Chase & Co. and Goldman Sachs Group Inc., posted a whopping 126% increase in FICC trading revenue in the fourth quarter, the biggest of any of the companies reporting this week. Even before Morgan Stanley’s release, Wall Street was looking at the largest surge in fixed-income trading revenue in more than eight years.

Now, an important part of the fixed-income trading story is that at this time a year ago, banks were reeling from sharp declines in FICC revenue — Morgan Stanley most of all. So a comeback was hardly unexpected. Still, the fact that bond traders raced past estimates, building upon a third quarter in which they looked like the MVPs of Wall Street, suggests there could be something more sustainable afoot, particularly given that volatility in U.S. Treasuries did nothing but decline in the final three months of 2019 while credit spreads only squeezed tighter.

The secret sauce might very well be a continued push toward “electronification” in fixed income. It’s become something of a buzzword for Morgan Stanley’s leadership, though analysts on Thursday’s conference call didn’t bring it up. For example, here’s Chief Executive Officer James Gorman in June:

“There's clearly more electronification going on within fixed income. It's becoming a more efficient platform for us. And there's a lot of share moving around the world right now. There's a lot of available share and we've picked up some of that.”

And here’s Daniel Simkowitz, head of investment management at Morgan Stanley, at the Bank of America Merrill Lynch Future of Financials Conference in November:

“Morgan Stanley is a real leader in electronification. If you go back to the equity markets, we're now applying that into the fixed income trading markets. So we have capabilities here to really help us maybe be a leapfrog player in quant in fixed income.”

It’s not just Morgan Stanley, either. Stephen Scherr, chief financial officer at Goldman Sachs, noted in an earnings call a year ago that in fixed income, “there’s an element of platform electronification as a means of which you can drive higher volumes” as bid-offer spreads narrow. And he added that “as we progress the initiative to build out those platforms, we’ll realize greater margin.” Overall, electronification in bond trading is going to be a “big story we’re going to see more of in 2020,” Bloomberg Intelligence senior analyst Alison Williams said.

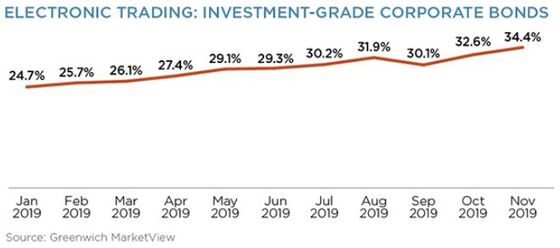

A Greenwich Associates report this week put some numbers to the narrative. It showed that electronic trading in investment-grade corporate bonds rose to 34.4% of daily volume in November, from 24.7% just 10 months earlier. On the one hand, that’s still a relatively modest slice of the market. On the other hand, that suggests more room to run. And more than half of it study participants executed a so-called credit portfolio trade, a strategy pioneered by Goldman Sachs.

“The slow and steady change that has occurred over the past decade will ultimately be seen for the revolution that it brought about,” wrote Kevin McPartland, head of research in Greenwich Associates’ market structure and technology group. “Market uncertainty in 2020 should only help this train accelerate.”

The trend runs parallel to the view of Wells Fargo analyst Mike Mayo, who has been wearing hoodies during television appearances as a way of drawing attention to banks’ investments in technology. Usually, though, he and others are thinking about digital banking and electronic payments.

Fixed-income trading, though, can seem at times to be about as slow to adapt to technological changes as an average retail bank customer. At a U.S. Treasury market conference in September, for instance, panelists including Amherst Pierpont’s Paul Murphy, Cantor Fitzgerald CEO Howard Lutnick, Citadel Securities’s Paul Hamill and Guggenheim Partners CIO Scott Minerd robustly debated whether direct price streaming in bonds was good or bad for the market. My takeaway was that there’s still a feeling among longtime denizens of the bond market that nothing is broken, so nothing needs to change.

The big U.S. banks might feel differently. It’s no secret that investors are scrutinizing the companies’ efficiency goals and how they’re balancing crucial investments with cost containment. To the extent that the banks can squeeze more out of fixed-income trading with electronification — a well that’s effectively run dry in equities — I’d expect they’re going to go for it.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.