(Bloomberg Opinion) -- The troubled Italian lender Banca Monte dei Paschi di Siena SpA took another big step in its long path to redemption last week by selling subordinated debt for the second time in six months. An 8% coupon is expensive for the world’s oldest bank, but it can hardly complain given its years of troubles.

Even though the yield is enticing, investors are still taking a gamble. They will doubtless have been encouraged by expectations that the Italian state will have their backs. Rome owns 68% of Paschi and there’s a fourth bailout on its way for the lender.

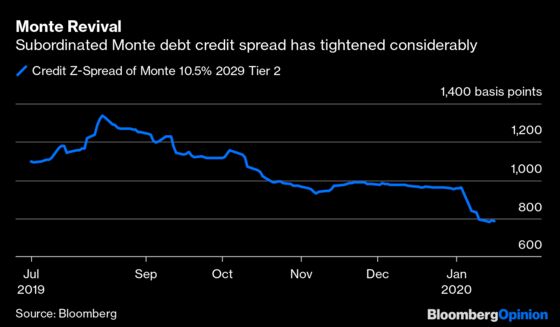

The general environment for investing in Italian banks is a bit better too. Another lender, Banco BPM SpA, issued some perpetual hybrid debt on Tuesday. Paschi is deeply into junk territory yet it managed to raise a chunky 400 million euros ($444 million). This was one-third bigger than a similar 10-year Tier 2 issue in July, and at a much lower cost than the 10.5% coupon it had to offer then. It was more than twice subscribed and the yield has tightened modestly since launch.

Monte Paschi’s debt coordinators showed a fair amount of skill with last week’s sale, amid another record start to bond issuance this year. Only days ago, the bank told shareholders it will have to take a big hit to profit after writing down deferred tax assets.

Still, for Monte Paschi it’s very helpful that the state aid just keeps coming. The bet by bond investors that Rome will keep doing whatever it takes may be a winning one.

Reeling from an acquisition that drained it of cash just as markets peaked in 2007, Paschi has had to turn to its government three times already to replenish its capital as losses on bad loans piled up. The last round, in 2017, saw Italy effectively take over the lender while pledging to exit by 2021 under terms agreed with the European Union.

The bank has made progress in cleaning up its balance sheet, but a ratio of non-performing loans of about 12.5% targeted for year-end and sluggish revenue render Paschi virtually untouchable for would-be partners. Luckily, as in the past, Italian taxpayers are on hand. Italy is in talks with Brussels to allow state-backed debt manager Amco to buy more than 10 billion euros of Paschi’s soured loans, a move that would reduce its bad debt ratio to below 5%, according to Morgan Stanley analysts.

You can never be certain about Monte Paschi, a bank that hid losses with complex derivatives and was found by the European Central Bank to have inadequate governance and financial controls as recently as 2017. But another round of aid might make it look more attractive to rivals. Bond markets clearly find it palatable.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2020 Bloomberg L.P.