(Bloomberg Opinion) -- It's a subject that just won't go away: Should the U.S. Treasury issue 100-year bonds?

With yields on 30-year U.S. bonds below 2% and much of the yield curve inverted, the conditions for issuing such debt couldn't be more favorable. So it’s no surprise that Treasury Secretary Steven Mnuchin is once again talking up the possibility. In an interview Wednesday, he said issuing ultra-long U.S. bonds is “under very serious consideration.”

But what about the buyers?

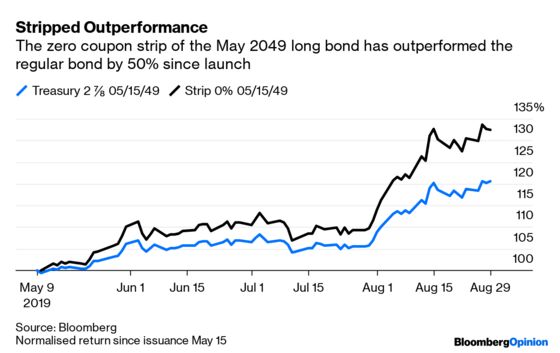

The answer may lie in the Strips market, in which dealers separate the coupon stream of a U.S. Treasury bond away from the final repayment principal, selling both pieces of the debt as separate securities. A 100-year Strip would have the longest possible duration (a measure of sensitivity to changes in interest rates) and be the most aggressive way of taking on interest-rate risk. The attraction of ultra-long maturities with very low coupons is that they offer bond investors huge exposure to positive convexity that is, their prices rise more sharply when yields fall than they decline when yields rise. The flip side, of course, is that if yields rise, the downside is considerable. But in a broad portfolio, this is manageable.

If there was a commitment from the U.S. Treasury to regular issuance of ultra-long bonds, it would drive liquidity and help create substantial investor demand. It could even help re-steepen the now super-flat yield curve that is heightening fears of an impending recession. But it would certainly change how interest-rate risk is traded and create a range of new hedging options.

For many investors, it makes little sense to invest in a long-dated bond that yields little more – and in some cases even less – than shorter-dated securities. But for pension funds and insurers, it’s all about finding assets with a longer duration to match against their liabilities. This is where Strips come in.

Stripping a 30-year of its coupon stream to create a principal-only security maximizes the duration to its final maturity, giving it similar characteristics to a 50-year or longer coupon-paying bond. For example, Canada’s 2.75% bond due in 2064 has a duration of about 30 years - the same as the 2049 U.S. Treasury strip. So why bother issuing 40-, 50- or even 100-year bonds if there is already a workable solution? The answer to that seems to be the rapacious demand for duration if yields continue to fall.

Of course, it’s hard to determine how sustainable the demand will be for ultra-long debt at yields this low. There is little point undertaking a seismic shift if it turns into an illiquid backwater ruining what is the most liquid fixed-income market globally. But the big risk is that century bonds suck demand away from the the benchmark 30-year long bond. That has long been the main bone of contention from the primary dealers (official market makers) that compromise the bulk of the Treasury Borrowing Advisory Committee.

The U.S. has long blown hot and cold on the subject of extending maturities beyond 30 years, the current longest maturity. As it is, issuance of this debt has been stepped up, and in turn reduced, many times. Following the financial crisis, the Federal Reserve's bond-buying programs took several approaches, one of which was a $400 billion purchase specifically of the longest maturities called "Operation Twist" between September 2011 and December 2012. It’s one of the main factors explaining why the yield curve is currently so flat.

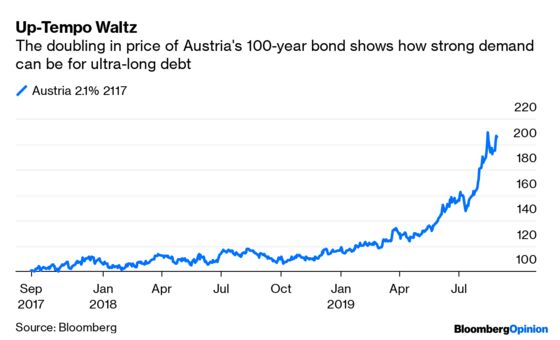

In Europe, the hunt for duration is so intense that it has enabled Austria, Belgium, Ireland and soon possibly Sweden to issue 100-year securities, but these have mostly been single issues. The U.S. Treasury bond market is the benchmark reference for most global bond markets. It cannot afford illiquidity or sideshows.

There needs to be a regular calendar issuance, and of sufficient size, to create a liquid market for U.S. ultra-long debt (and one big enough to support the creation of Strips). That means issuance at least twice a year – if not quarterly – of at least $5 billion to create a proper curve. It took a long time to create a viable market for inflation-linked U.S Treasury bonds (known as TIPS), but this is now an integral part of how investors manage exposure. A committed approach could lead to a significant shift in the way bonds are traded – and a new market for the new normal of ultra-low yields.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.