British Tech Giant's $8.8 Billion Case of Indigestion

(Bloomberg Opinion) -- Britain’s once biggest software company had eyes bigger than its tummy.

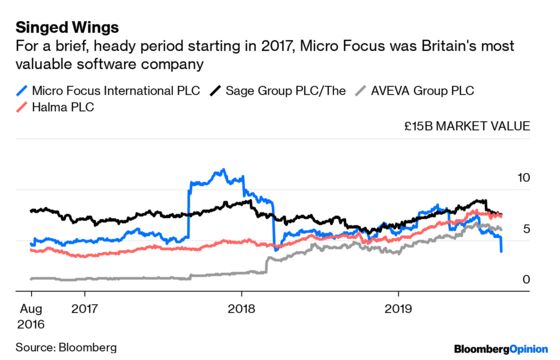

Micro Focus International Plc acquired part of Hewlett Packard Enterprise Co.’s software assets in an $8.8 billion deal in 2017, trebling its headcount in the process. On Thursday, the British company cut its revenue forecast for the second time in as many years.

Sales will fall as much as 8% this year, compared to the company’s earlier estimate of as much as 6%. The stock dropped 34%, dragging Micro Focus’s market capitalization down to 4 billion pounds ($4.9 billion), below its level before the takeover.

There’s no obvious solution beyond, well, selling more product. Thursday’s announcement included plans for a strategic review of its operations. The statement made vague allusions to “execution improvements” and “strategic, operational and financial alternatives”.

That wording seems to encompass the prospect of a private equity-backed buyout. Micro Focus is certainly cheap now: it trades at just six times forward earnings. But given Chairman Kevin Loosemore’s approach to generating shareholder returns, it’s unclear exactly how going private might improve the business.

Since taking over as chairman in 2011, Loosemore has grown Ebitda more than eight-fold by acquiring legacy software companies, dramatically cutting costs and cross-selling products. This strategy appears to leave little room for a private equity buyer to take similar steps. A leveraged buyout of a shrinking business, whose costs have theoretically already been cut to the bone, would require some considerable strategic vision.

The primary benefit of shelter from the capital markets might be to increase investment in research and development, potentially allowing the company to re-emerge in five years’ time with a compelling growth story. That would not only be a major gamble, but a significant strategic shift.

With the existing strategy, improvement needs to come from the sales side, and that’s something that benefits from greater scale. On that basis, carving the company up and selling off its constituent pieces would seem counter-intuitive, since it would reduce said scale.

In the 12 years before the HPE acquisition, Micro Focus boasted annual compound shareholder returns of almost 30%. In the two years since, the compound return has been a negative 14%. It’s hard to see the escape route from this trajectory.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.