Madame Tussauds Displays the Appeal of Private Ownership

(Bloomberg Opinion) -- Shareholders in Merlin Entertainments Plc are poised to exit the theme park.

The company that operates Legoland resorts and Madame Tussauds wax museum has agreed to a 4.8 billion pound ($6.1 billion) joint bid from Blackstone Group LP, the family behind the Lego empire, and Canadian pension fund CPPIB.

The offer continues the trend for private equity groups to buy back the businesses that they once owned, and are languishing in public markets. The descendants of Lego founder Ole Kirk Christiansen sold a share of their stake in Merlin to Blackstone in 2005, and the company was listed in London in 2013. The family has held a stake throughout, and it now stands at almost 30%.

Companies that are unloved in the stock market make good targets for a second bite of the cherry by the private equity firms that were previous owners. They know the businesses well. Add in the fact that buyout funds have more money than they know what to do with, and you have deals for U.K. satellite company Inmarsat Plc and Swedish building materials group Ahlsell AB.

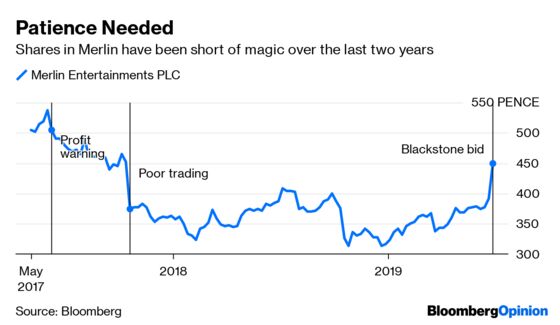

The 455 pence per share offer for Merlin represents a 15% premium to the closing share price on Thursday, and looks fair. It is around the level the stock was were trading at before a lackluster trading update in Oct. 2017, when demand for the company’s attractions was dented by nervousness about terrorism and the first signs of the U.K. consumer slowdown. The shares have traded lower ever since. They rose 14% on Friday, to just below the offer price.

As for the buyers, it’s hard to see what they can do differently. Having come from private equity ownership, the company is already pretty efficiently run. There isn’t scope for big cost cuts. Current management will continue.

What will be change is how patient investors will be. Blackstone is making the investment from its long-term fund, which typically has a time horizon of at least ten to 15 years. In private hands there’s scope for owners to allow ample time for investments to pay off, a point made by activist investor ValueAct Capital, which has a 9.3% stake. Merlin has spent about 1 billion pounds over the past three years developing its attractions, but the potential benefit from this has not been reflected in earnings, or the share price.

The new owners are betting that the investments the company is currently making will ultimately generate returns. At that point, the Merlin can achieve an appropriate evaluation in public markets.

There is one wild card: a combination with Whitbread Plc, which has been mooted by some analysts. The company is focused on hotels now that it has shed its Costa Coffee chain. It wants to expand internationally, and Merlin’s global reach would help. Merlin, meanwhile, is building accommodation in its attractions. Whitbread would bring an experienced operator, plus potential synergies.

The large number of hotels that the group would own outside of Merlin’s attractions is a significant stumbling block, and makes a deal a stretch.

But with the potential for Whitbread to come under pressure to bolster returns from its hotel division, Merlin’s new owners should consider the combination as another route to create value from the buyout.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.