The Late '10s Were Better for Incomes Than the '90s

(Bloomberg Opinion) -- New Census data show that the six years from 2014 through 2019 were, economically speaking, some of the best in recent American history. The last three years of President Barack Obama’s term and the first three years of President Trump’s brought income gains that probably exceeded even the boom of the late 1990s.

The economy still has some fundamental problems, even before accounting for the impact of the coronavirus pandemic. But the income growth of 2014-19 suggests the underlying engine of the U.S. economy still has the potential to create prosperity for the middle class.

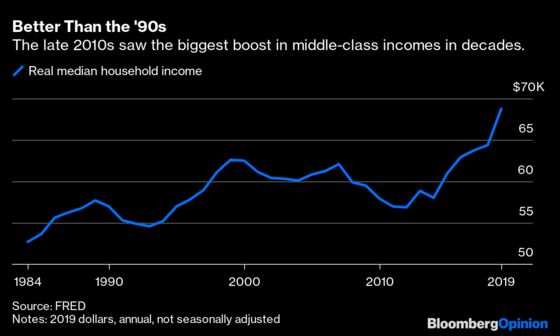

Between 2014 and 2019, the typical U.S. household saw its inflation-adjusted income increase from $58,001 to $68,703 — an 18.5% increase.

That’s even better than the 14.8% increase logged between 1993 and 1999, the go-go years of the technology boom. And in the ‘90s, people got some of that additional income by putting in more hours every year, whereas in the recent boom working hours per employee were effectively constant.

Poverty also fell significantly between 2014 and 2019. Thus, in terms of incomes at the middle and bottom of the distribution, the late 2010s were very good years — perhaps the best since the 1960s. (The one caveat is that the 2019 numbers might be slightly inflated from lower-income people being less willing to answer surveys in the middle of a pandemic.)

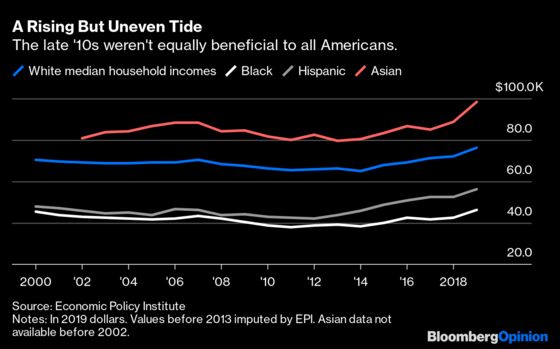

Broken out by race, those gains were not evenly distributed:

Hispanic and Asian Americans posted strong income gains — 22.8% and 21.3%, respectively. The fact that many Hispanic and Asian Americans are the children of immigrants probably helped, as there tend to be big income jumps between first and second generation Americans. White and Black Americans saw more modest gains of 9.9% and 7.8%, respectively. Black Americans, in particular, made barely more in 2019 than they did two decades prior. Shrinking the gap between Black Americans and others remains a pressing task for policy makers.

But the gains for all Americans are still notable when compared to previous economic expansions. The so-called “Bush boom” of the 2000s, in particular, looks anemic in comparison, with overall median income actually falling between 2000 and 2007.

Why was the 2010s expansion so good for the middle class? One reason is probably its length. GDP began to recover from the Great Recession in 2010, and employment began to follow in 2012, but wages remained stagnant until 2014. This lag was probably due to the fact that it takes labor markets some time to tighten up as workers return to work after a recession. The fact that the 2010s expansion was the longest in postwar history meant that even with years of delay, income had six years to grow unimpeded. Workers at the bottom of the income distribution, who are typically the first to be fired and the last to be hired as the business cycle ebbs and flows, are especially dependent on long expansions to raise their incomes. The 2010s recovery stands in contrast to the 2000s boom, which lasted only a few years.

Another reason the 2000s expansion was so anemic was the “China Shock.” China’s abrupt entry into the world trading system glutted the global labor market and probably put downward pressure on wages. But since 2007 or so, China’s increased labor and input costs are evening the playing field in terms of cost-competitiveness; the China Shock is over. That may be helping U.S. incomes to grow a bit faster.

The 2010s demonstrate something very important about the U.S. economy: Its capacity to generate broad-based income gains is still intact. In recent decades, many have come to believe U.S. economic growth only benefits the wealthy. But per capita GDP only grew by about 9.4% total between 2014 and 2019. That means the typical American household’s income actually outpaced the economy itself. And this all happened with slower-than-usual growth in government transfer payments.

In other words, economic growth can still generate prosperity for middle-class and poor Americans. But the circumstances have to be right. Most importantly, the country has to avoid being buffeted by the cruel winds of macroeconomics. Like a well-running car that keeps driving over potholes, the U.S. economy has been hit by the tech bust of 2000, the housing crash of 2008, and the coronavirus disaster of 2020.

It’s not clear the Federal Reserve has the power to prevent or even substantially delay episodes like these, but it should try. The priority should be to keep expansions going for as long as possible — to avoid “taking away the punch bowl” unless inflation is running rampant. The longer the boom, the more of the benefits go to the middle class and poor. Congress can help by tempering its instinct toward fiscal austerity.

Finally, the U.S. government should try to minimize the impact of episodes like the China Shock and coronavirus. Pushing back against Chinese currency undervaluation in the ‘00s might have helped ameliorate wage declines. And wise management of the pandemic would have mitigated the current economic crisis.

Fundamentally, though, the 2010s expansion suggests a vast overhaul of the U.S. economy might not be as necessary as more radical reformers believe. Racial income gaps need to be compressed, inequality needs to be reduced, and threats such as climate change must be averted. But there is much that is right in the U.S. economic system.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2020 Bloomberg L.P.