Opioid Crisis Squeezes Last Air Out of a Stock Bubble

(Bloomberg Opinion) -- The opioid crisis is squeezing the scant remaining air out of one of the biggest stock bubbles in recent years.

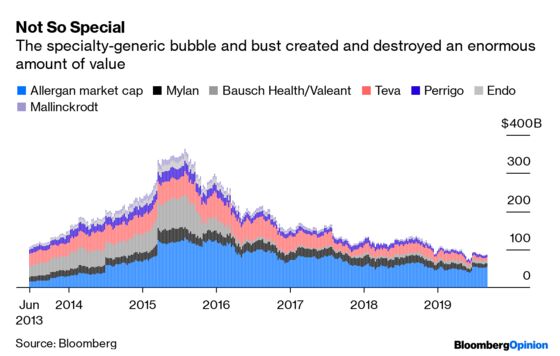

From 2012 to 2015, investors embraced so-called specialty-generic pharmaceutical firms including Endo International PLC, Mallinckrodt PLC and the company formerly known as Valeant Pharmaceuticals (now Bausch Health Cos.). These drugmakers mixed branded medicines with copycat treatments in varying proportions, and often grew via aggressive acquisitions. Analysts and hedge funds hyped the sector in spite of escalating debt loads. At a peak in July 2015, seven of the groups biggest companies were worth a combined $370 billion.

After a report Wednesday that Mallinckrodt has hired restructuring advisers as it faces opioid-related lawsuits and looming liabilities, those same seven are worth about $86 billion; Mallinckrodt alone has seen its market value plunge from a peak of more than $15 billion in 2015 to a mere $134 million today. While only some of the group are exposed the same way Mallinckrodt is to potential losses from opioid litigation, the threat of large settlements and jury awards has accelerated what’s been a steady and at times precipitous decline for the whole group.

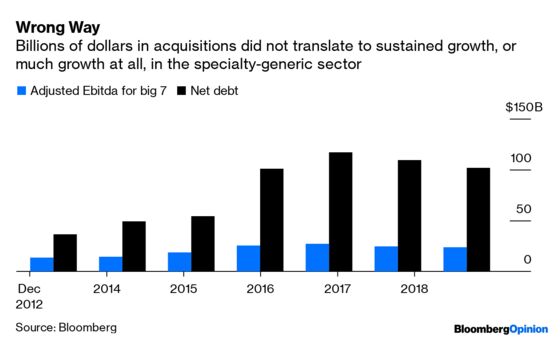

Many of these companies followed a playbook that was tailor-made to attract investors at a time when biopharma sentiment was boisterous. Like traditional drugmakers, they offered the promise of hefty profits, but with far less expensive and risky R&D spending. The idea was that revenue from generic drugs would generate steady cash flow, allowing these companies to acquire specialty drugs from rivals, slash costs, and polish up neglected medicines. And cheap debt enabled lots of significant deals.

Pershing Square’s Bill Ackman declared Valeant an undervalued platform gem in 2015 as he promoted his substantial investment in the firm. The hedge fund investor argued that the company’s durable products and acquisition track record could see its share price pass $500 by 2020. Plenty of companies emulated the strategy as Valeant’s shares soared, or were pushed into unwise and expensive deals in the resulting heated acquisition environment.

Reality bit hard, even for firms that didn’t fully embrace the platform model. It turns out that it’s hard to consistently boost sales of older products, which made up a disproportionate share of even the branded portfolios at these companies. The cost of acquisitions skyrocketed as stock valuations rose, adding to the pressure to perform. The unsurprising result was a cornucopia of allegedly unsavory sales practices, from massive price increases to suspect relationships with pharmacies and price-fixing. Valeant notoriously hiked the prices of two emergency heart medicines by more than 200% and 500% right after acquiring them in 2015; today, Mallinckrodt charges more than $38,000 a vial for a decades-old drug for treating infantile spasms that once cost as little as $40.

Pricing pressures began to crop up not just for branded specialty drugs, but in the previously reliable and growing U.S. generic business. These companies didn’t have the drug pipeline or financial flexibility to react when their products proved less durable and profitable than expected. Shares began to plunge as investors started to realize that the ambitious growth targets throughout the sector weren’t remotely achievable and that massive debt payments loomed.

Opioid liabilities may be the final straw for companies like Mallinckrodt, Endo, and Teva Pharmaceuticals International that have significant exposure to thousands of ongoing lawsuits. The first two especially have flimsy balance sheets left over from their acquisition days and as they look to manage their debts, bankruptcy isn’t out of the question. This unusually large risk is another of the many things that bulls missed when they piled into the sector at inexplicable valuations. Notably, Bausch – the former Valeant – is free of that particular issue and seems to be slowly digging itself out of its hole. Its past heights are out of reach, however, and others may not be as lucky.

The pharmaceutical business is uniquely complicated and exposed to significant, sudden shifts, and within the industry, the specialty-generic sector is uniquely unsuited for high-leverage gambles and ungainly roll-ups – however enticing their appeal. Next time a company comes around to pitch a simple and largely R&D-free path to riches in the drug business, let’s hope investors are wise enough to think twice before jumping in.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.