(Bloomberg Opinion) -- Price stability is when people stop talking about inflation and their decisions reflect genuine economic factors. It has been a long time since inflation was a talking point but, especially in the United States, it has reentered public debate.

In several advanced economies, evidence of rising input prices and higher output prices reflecting shortages is easy to find. Some of these increases may well prove transitory. For the first time since the 1980s, though, two factors make inflation a serious risk: excessive monetary and fiscal stimulus, and weak political resistance to the threat.

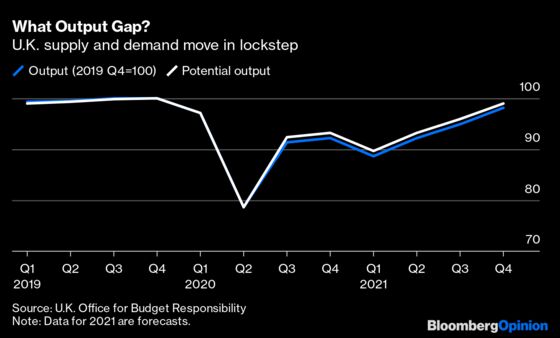

In the U.S., former Treasury Secretary Larry Summers has argued persuasively that fiscal stimulus is excessive. Many economists are reluctant to criticize the Biden stimulus plans because they share his concerns about the country’s social and political problems. But I’ve seen few challenges to the proposition that the degree of stimulus is out of all proportion to the magnitude of any plausible output gap. And the same logic applies to other advanced economies. The chart below shows the unprecedented quarterly fluctuations in output in the U.K. from 2019 through to the end of 2021 (using forecasts from the Office for Budget Responsibility). Those fluctuations — by far the largest since reliable statistics began to be collected — reflect economic lockdowns as the country struggled with Covid-19.

The chart also shows a second line — for the OBR’s estimate of potential output over the same period. What is so striking is that the differences are negligible — the lines move together, reflecting a judgement that the lockdowns affected both demand and supply. This is a sensible view and one that the Bank of England shares. The central bank’s estimate of the output gap is around 1% in the first quarter of 2021, falling to zero in the first quarter of next year. Both find that the output gap at its largest was no more than about 1% of gross domestic product and is expected to diminish over time.

This makes it hard to argue that substantial monetary and fiscal stimulus is required. Although Covid-19 has ravaged our economies, its impact has been on both demand and supply. The case for substantial monetary expansion in March 2020 was couched as a response to “dysfunctional markets.” But the monetary injection was not withdrawn once financial markets were operating normally. The stimulus was then justified in terms of “supporting the economy.” The government did need to support the economy — but substantial monetary stimulus is appropriate only when aggregate demand deviates markedly from aggregate supply.

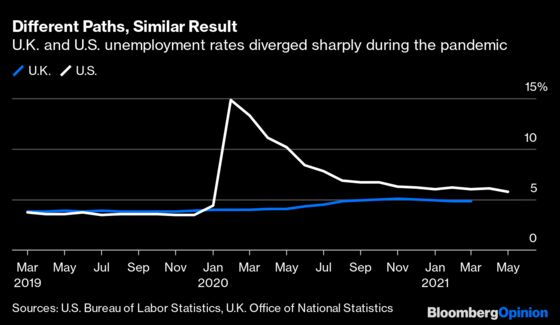

During 2020 and for much of 2021, governments were right to use fiscal policy to prevent a wave of business failures. Many businesses suddenly confronted with a collapse of demand had a viable future once the pandemic could be controlled. The cost of letting them go under and then somehow reviving them would have been enormous. In Europe, governments devised furlough schemes to transfer money from future taxpayers to businesses on condition that companies maintained employment. In the U.S., support took the form of more generous unemployment benefits and subsidies for the worst-affected industries, such as airlines. The difference between these two approaches can be seen in terms of unemployment. The chart below shows that unemployment in the U.S. rose sharply from 3.5% to 15% before falling back again to its current level of 5.8%. U.K. unemployment rose from 4% to only 5.1%, before edging down to 4.8%.

There’s another reason to worry. Support for monetary policy as the way to combat inflationary risks is declining. Over the next few years, governments will probably want to spend more, but won’t want to increase taxes on most citizens. Higher interest rates, or a shrinking of central-bank balance sheets, will make it more difficult for governments to finance their deficits. Inevitably, there’ll be political pressure on central banks to respond slowly to signs of higher inflation.

In turn, central banks have rather painted themselves into a corner, giving the impression that policy will be loose for a long time. The Federal Reserve has been the most explicit about this, but the use of forward guidance by several central banks has been taken as a sign that central banks don’t want to tighten policy for some considerable while. No central bank can know what the appropriate level of interest rates will be a year from now, let alone in 2024. So the risk of either a slow response to signs of higher inflation or a sharp market correction in response to an unexpected tightening — both of which would damage central-bank credibility — are real.

Central-bank independence will be tested over the next few years. And the expansion of central-bank mandates into areas of policy which are naturally the domain of elected politicians — such as targeting unemployment rates of particular groups in society or using monetary-policy tools to combat climate change — will compound the problem. It will be harder for central banks to disappoint governments, even when controlling inflation makes this necessary.

A combination of political pressure to assist in financing budget deficits, promises not to tighten policy too soon, and a growing involvement by central banks in political matters all point to a growing risk that central banks will respond too slowly to higher inflation.

Few remember the inflationary experience of the 1970s. But the fact that inflation is not a problem today doesn’t mean that it isn’t a risk. In the late 1960s, as a student in Cambridge, England, I remember going to lectures from an old man who warned his audience that creeping inflation was a problem we should take seriously. Had he really failed to grasp that Keynesian economics allowed us to combine full employment with low inflation? We ignored him. He was the past and we were the future. That professor was Richard Kahn, John Maynard Keynes’s disciple and confidante, the person credited with inventing the multiplier. He turned out to be right.

We can’t know today if inflation will rise over the next few years. But the prospect of excessive stimulus and weakened central-bank independence should make us nervous.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mervyn King was governor of the Bank of England from 2003 to 2013. He is the Alan Greenspan Professor of Economics at NYU Stern School of Business and professor of law at NYU School of Law, and author (with John Kay) of “Radical Uncertainty: Decision-Making Beyond the Numbers.”

©2021 Bloomberg L.P.