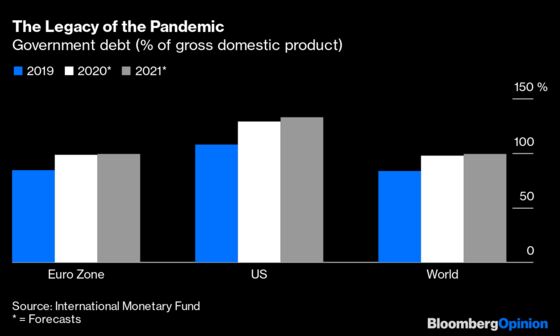

(Bloomberg Opinion) -- Just like clothes and food, macroeconomics has its fashions. The latest is for public debt. From the OECD to the International Monetary Fund, global organizations that traditionally supported fiscal restraint have become much more relaxed about sovereign borrowing.

The argument is that debt sustainability is less of a problem if central banks keep interest rates ultra-low. Governments should ditch old fetishes, such as the ratio between debt and gross domestic product, and concentrate on more meaningful measures like interest payments as a percentage of GDP. You can see the appeal. Look at Greece, where a change in borrowing costs and loan maturities has made a huge debt pile seem manageable.

However, this latest macroeconomic fad is based on one crucial assumption: that inflation will stay subdued, letting central bankers continue with low rates and big asset purchases. That’s a pretty big thing to rely on. Any sustained rise in inflation might prompt the U.S. Federal Reserve and its global peers to tighten monetary policy, in order to hit their inflation targets. Investor attention would then shift back to traditional — much less comforting — measures such as debt-to-GDP ratios, raising the prospect of financial instability.

Economic history is dotted with iron laws that didn’t endure. In the 1960s, governments were convinced of the stable relationship between inflation and unemployment — known as the “Phillips curve.” Politicians assumed they could simply pick a point on this curve depending on whether they preferred to protect jobs or keep prices in check. One consequence was the so-called “stop and go” policies, whereby governments engaged in a succession of stimulus and austerity as they sought to navigate this trade-off. It took Milton Friedman’s landmark 1967 address at the “American Economic Association” and the stagflation of the 1970s to show things weren’t so simple. Today’s economists treat the Phillips curve with caution.

Another example is the “great moderation” of the 1990s and 2000s, when policy makers in advanced economies believed they’d tamed the business cycle permanently. Some credited the establishment of independent central banks with inflation targets, which in theory anchored price rise expectations and prevented governments from overheating the economy.

It turned out there were other more subtle factors governing rich-world inflation, including globalization, the technology revolution and China’s entry to the World Trade Organization. The 2008 financial crisis and the great recession killed off any claims about an end to “boom and and bust.”

Many economists will, as ever, claim that this time is different. They offer various explanations of why inflation will be permanently low or negative, including: technology’s moderating effect on prices; the deflationary impact of an ageing society; and the role of inequality in constraining overall spending. Evidence since the 2008 crisis supports those who are unworried by inflation spikes. Central banks have engaged in unprecedented stimulus, which critics feared would trigger hyperinflation. But they’re still struggling to lift inflation toward its typical target of about 2%.

However, one cannot assume that the near future will be like the recent past. The post-pandemic world will offer a first test of whether low inflation is here to stay. As demand surges, supply constraints continue to bite and companies tries to rebuild their profits, we may see a reemergence of price pressures.

There are powerful forces going in the opposite direction, too, such as the large number of people who’ll lose their jobs or suffer wage cuts. But inflation may not be gone forever. In the euro zone, core inflation — excluding volatile items such as food and energy — jumped to 1.4% in January, its highest in more than five years (though this was largely due to temporary factors). In the U.S., President Joe Biden’s proposed $1.9tn stimulus program has spooked some economists, including former Treasury Secretary Larry Summers and Olivier Blanchard, the IMF’s former chief economist, who are worried about its inflationary consequences.

In theory, inflation need not be a bad thing for public debt. Accelerating prices have helped governments tackle previous debt mountains because they push up tax revenues, while what is owed remains fixed in nominal terms. Nations will also benefit from the favorable debt structures they built during years of disinflation. This includes low rates, longer maturities and a large portion of sovereign debt held by sovereign banks.

And yet, this ignores financial market dynamics. As inflation returns, it’s easy to imagine investors rushing for the exit as they try to avoid bond losses. If debt-to-GDP does become voguish again, things could look ugly. Central banks wouldn’t be able to intervene, in fear of compromising their commitment to inflation targeting.

There are two things for policy makers to consider here. The first is the quality of government spending. Politicians must do all they can to support their economies as the pandemic rages on. Even after they’ve rolled out their vaccination programs, states should keep the help coming, especially for families that have suffered the most. However, as Italian prime minister-in-waiting Mario Draghi, said last summer, there are “good” and “bad” debts, since some wisely targeted spending programs do much more to lift a country’s long-run growth rate. Countries who’ve used their borrowings unproductively will struggle if instability returns.

The second thing for central banks to think about is their own position. In the U.S. the Fed has made clear that it’s willing to tolerate periods of higher inflation, which could help lessen fears of sudden monetary tightening. The European Central Bank is in the middle of a strategy review, and will need to ask itself this same question. Just because you promise that you’ll ignore higher inflation doesn’t mean the market will believe you. But the Fed is right to set out what it thinks. Any change in central bank priorities needs to be communicated promptly.

We are indeed living through a revolution in macroeconomics, but facts will change one day. Governments and central banks must prepare.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2021 Bloomberg L.P.