(Bloomberg Opinion) -- Marks & Spencer Group Plc showed off its key looks for the autumn winter season this week. It is aiming to woo shoppers with 1970s-inspired prints, jewel toned blouses and tailored coats. But the high street stalwart has gone out of fashion with investors. Its shares are set to fall out of the FTSE 100 index for the first time in 35 years.

As a bellwether for the British retail industry, M&S’s demotion underlines the dire condition of the U.K.’s store groups. But for the seller of Percy Pig sweets to cashmere sweaters, it isn't the disaster it might first appear to be.

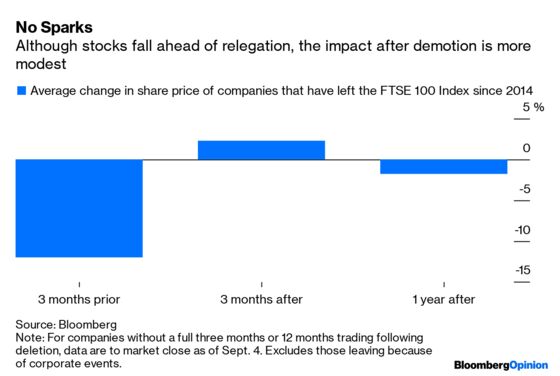

Its shares have fallen 33% over the past year, and at about 190 pence are close to their level at the depths of the financial crisis.

Any further decline in the M&S share price precipitated by the relegation would be unwelcome to its army of individual investors, which own about 20% of the stock.

But a fall out of the FTSE 100 would get the demotion over with. Talk of M&S’s demise wouldn’t keep coming round every quarter that M&S was on the cusp. That would at least give Chairman Archie Norman and his team a break from one pressure.

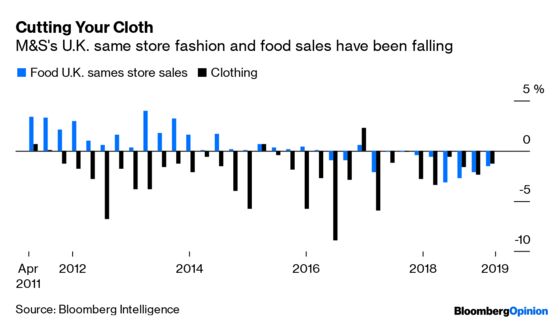

And they have plenty of others to contend with. The clothing market remains extremely difficult. Analysts at Goldman Sachs expect a 3% decline in same-store U.K. clothing and home furnishing sales in M&S’s fiscal first half. Like-for-like food sales, they forecast, will be flat.

Meanwhile, M&S must make a go of its joint venture with Ocado Plc, after buying half of the online retailer’s U.K. division for up to 750 million pounds ($916 million). Norman wants to double M&S’s food sales over the next five years or so to about 12 billion pounds – but he has to convince customers to switch from Ocado products currently supplied by Waitrose to alternatives from M&S.

If the share price is hit further by the demotion from the FTSE 100, then it could finally force the company to consider splitting up its food and clothing operations. With profits from both divisions under pressure, and undemanding retail multiples, there’s little value to be gained from a break-up right now. But if Norman can make a go of the Ocado deal, this should elevate the worth of the food business, making a split more compelling.

The other possibility is that a predator emerges. Bids for Greene King Plc in the U.K. and Metro AG in Germany show that appetite is there for consumer groups. While M&S’s old adversary Philip Green isn’t in a position to pounce, private equity might, particularly if it backed Norman and Justin King – handily, the former Sainsbury boss is a non-executive at the retailer. The group might just also appeal to Amazon.com Inc. But any bidder would have to get comfortable with the risks of both Brexit and M&S’s 9.3 billion pounds of pension liabilities. While the program had a 900 million-pound surplus at March 30, any change of control could see the trustees push a new new owner to inject more funds – possibly as much as 1 billion pounds.

That leaves Norman with grinding out the promised turnaround. He will be hoping M&S’s spell in the FTSE 250 index will be a fleeting trend, rather than a wardrobe staple.

--With assistance from Elaine He.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.