(Bloomberg Opinion) -- More than three years after the Brexit referendum left investors with $23 billion trapped in seven U.K. real estate funds, holders of another property portfolio have discovered that when their right to daily redemptions meets the reality of hard-to-sell assets, their money can become a hostage to illiquidity.

M&G Plc on Wednesday said it’s freezing a 2.5 billion-pound ($3.3 billion) property fund after it suffered “unusually high and sustained outflows” at a time when the looming election and the prospect of Britain finally leaving the European Union “have made it difficult for us to sell commercial property.”

With investors in Neil Woodford’s flagship fund still locked in almost six months after he halted redemptions, the U.K. regulators will surely have to act. The measures introduced by the Financial Conduct Authority in September — ordering fund managers to suspend redemptions if there’s “material uncertainty” about the value of 20% or more of a funds’ real estate holdings — clearly have not gone far enough.

Of course there’s room for debate about what distinguishes a liquid security from an illiquid one. And no one wants to bar retail investors from participating in the higher returns that come with an illiquidity premium. But property is clearly beyond the bright and shining line of what counts as an easy-to-sell asset, wherever you choose to draw it.

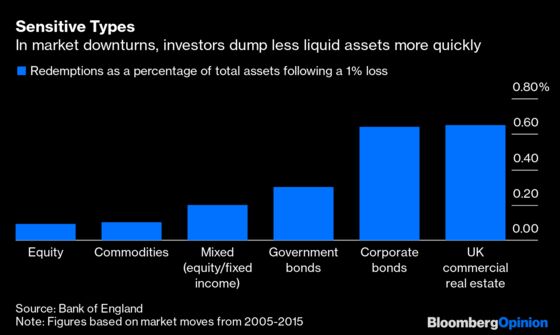

And peer pressure just doesn’t cut it as a good excuse for maintaining the status quo, even if it’s a plausible explanation for why we are where we are today. As Bank of England Deputy Governor Jon Cunliffe explained in July, “It’s not clear how strong consumer demand for absolute daily liquidity is. But if everyone else in the market is offering it, it’s difficult for one fund not to offer it.”

It’s time he and his colleagues came up with a solution. There is one possible way to address that issue, at least as far as property funds are concerned. Regulators could oblige real estate portfolio managers to switch to less-frequent redemptions — once a quarter, for example, holders would have the right to redeem their investments, with their cash returning to them at the end of the three months.

If the promise of daily liquidity for assets that are hard to sell is “built on a lie,” as Bank of England Mark Carney said in June, then it’s time for the overseers of finance to inject a dose of truth and reality into the market — before more investors find their nest eggs imprisoned.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.