Lying Flat Can Be a Winning Investment Strategy Too

(Bloomberg Opinion) -- Sometimes, when you try too hard, you lose. But the “lie flat” approach to life, which rejects hard work in favor of doing as little as possible to get by, can even provide profits while reducing your stress.

As the year draws to a close, the number crunchers are left struggling to explain to their investors why they missed out on trades that generated big wins for those who were more laid-back when it came to due diligence. But no one said life was fair.

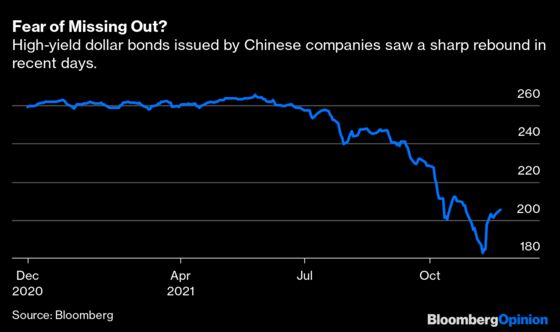

Take China Evergrande Group, the world’s most indebted real estate developer. Distressed-debt funds flocked to buy its bonds in late September, even as more conservative investors, such as pension funds and insurers, distanced themselves. After all, Beijing made it clear there would be no bailout for the company, and high-yield dollar bonds issued by Chinese companies had their worst selloff in at least a decade.

That turned out to be a pretty good trade. Evergrande has not defaulted, and chairman Hui Ka Yan used $1.1 billion of his own money to repay investors. The $2 billion bond due in March has climbed to about 32 cents on the dollar from 26 cents at the end of September.

Let’s not kid ourselves. Buyers didn’t do extensive credit research — in fact, they would probably have run the other way if they had. Consider the notes issued by Evergrande’s main onshore subsidiary, Hengda Real Estate. Rather than an outright guarantee, these bonds only have “keepwell clauses” — essentially handshake agreements. They are the lightest of all covenants. Evergrande is not obliged to repay.

“I am betting for this thing to get settled out of court, like via a low-price tender offer, a debt-to-equity swap, or whatever,” an investor in the Hengda bond told the Financial Times. This investor is already up about 30% in the last month. And if Hengda paid its 6.5% coupon next month, he could be looking at a total return of about 70% by year-end.

This laid-back attitude towards investing is now permeating the entire marketplace. In mid-October, Kaisa Group Holdings Ltd., China’s second-largest high-yield dollar bond issuer after Evergrande, saw its notes rebound the day after the developer missed interest payments. (It has a 30-day grace period.) At less than 30 cents on the dollar, it was better than a lottery ticket.

In a way, doubling down — and looking to catch a break — with the year winding down is a sensible response to a very unpleasant 2021. Since February, the most popular long positions held by hedge funds globally has lagged the S&P 500 by 16 percentage points, exceeding the 2015-2016 period as the worst on record, data compiled by Goldman Sachs Group Inc. show.

In China, many young people are choosing to “lie flat” — a movement born with a tweet in April that has swept the nation and even prompted criticism from President Xi Jinping — because their economic reality has become too complex to make sense of. It’s the same in the corporate world. Good luck trying to conduct thorough credit analysis on property developers. From buying land to construction and sales, every step is an opportunity to squeeze in hidden debt; sometimes even the company insiders do not know how much they owe. The same thing goes for Beijing’s big tech crackdown: Do you have a window into President Xi’s thinking? Even top spies at the Biden administration don’t.

By now, due diligence on Chinese companies is almost pointless. Investors might as well give up and lie flat too, dipping in when assets look cheap. Because you never know. Sometimes you just get lucky.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2021 Bloomberg L.P.