(Bloomberg Opinion) -- Shopping streets are awash with special offers right now, but the best luxury names never go on sale.

LVMH Moet Hennessy Louis Vuitton SE’s agreement to buy Tiffany for close to $16.5 billion, including assumed net debt, is no Black Friday bargain. The French luxury giant is paying a 37% premium to where the share price stood before Bloomberg News reported the approach in late October.

But Bernard Arnault, LVMH’s founder and chief executive officer, has avoided having to go as far as matching Tiffany shares’ five-year high reached in July 2018 of around $140.

The deal values Tiffany at about 16 times forward Ebitda. That still compares well to the 23-24 times that Bloomberg Intelligence estimated for LVMH’s 2011 purchase of Italian jeweler Bulgari and Swatch’s 2013 acquisition of star-studded diamond-jewelry and luxury-watch maker Harry Winston.

Still, at $135 per share, LVMH will have to apply slightly more polish to the Tiffany diamonds. To make a return on the target’s cost of capital, it will need to expand the jeweler’s annual sales by about 7-8% through 2024. They are currently expected to increase by just 4% in 2021 and 2022. It would also need to elevate margins to about 23-24%, from about 18% currently.

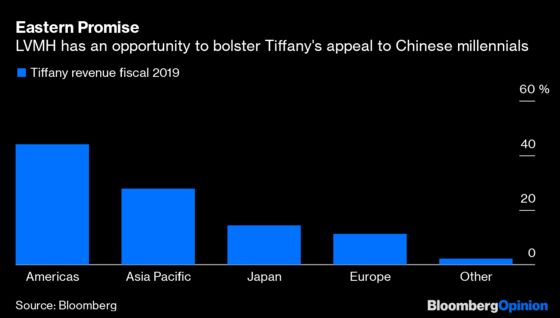

That should be achievable, given LVMH’s scale and track record. Still, it has given little detail on how it plans to turbocharge Tiffany’s appeal to the millennial crowd to revive the allure of times gone by. That’s disappointing. Even if this deal is relatively small for LVMH, which has a market capitalization of about $225 billion, the company still needs to articulate how it will make this pay.

Likely on the agenda, as I wrote last week, is expanding in Asia, where LVMH will be able to secure the best locations for Tiffany, thanks to its clout with landlords. LVMH could also step up the pace of the U.S. company’s product development, backed by its muscular marketing machine. There may also be some synergies in advertising and selling Tiffany’s jewels online, although LVMH didn’t outline any specific savings in its announcement on Monday.

Rivals, particularly Cartier owner Richemont, should be concerned about this new pairing. While Tiffany is best known for its sterling silver ranges, its edgier fine jewelry is not that far from some of Cartier’s collections. A Tiffany emboldened by LVMH design and distribution could be more of a threat.

Having been on the sidelines as LVMH wooed and won over Tiffany, the Swiss luxury goods maker, whose other brands include Van Cleef & Arpels, and Kering SA, which owns Gucci and Balenciaga, could respond by making acquisitions of their own, or even by considering pursuing a merger with each other.

As for LVMH’s purchase of Tiffany, with no counterbidder, Arnault had the upper hand, and could possibly have held off from raising the offer above the $130 proposed last week. But doing so allowed him to clinch the deal with a dose of goodwill thrown in.

Tiffany would have had a hard job persuading its investors that it could reach the sort of levels being offered by the French luxury group without some kind of sustained takeover interest from LVMH or elsewhere. And yet even that may have been difficult if the U.S., which accounted for more than 40% of Tiffany’s sales in its most recent financial year, is truly hit by a slowdown.

The sweetened bid was enough for LVMH to secure a recommendation, and make absolutely certain that no rival could intervene.

In this bling saga, each side emerges with a holiday gift, tied with a Tiffany bow.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.