French Billionaire Might Prefer Cartier to Tiffany

(Bloomberg Opinion) -- Ever since LVMH Moet Hennessy Louis Vuitton SE said it was walking away from Tiffany & Co., the question has been why?

The obvious answer is that LVMH chairman Bernard Arnault is trying to shave the $16 billion purchase price that now looks too high given the damage inflicted on the luxury industry by Covid-19. But saving a couple of billion dollars is a rounding error to a company with a market capitalization of about $240 billion. It could hardly be worth getting dragged into an acrimonious fight.

Another possibility is that he’s interested in pursuing alternative opportunities. One recurring scenario among the market speculation is that LVMH could look to make a bid for Cartier-owner Cie Financiere Richemont SA.

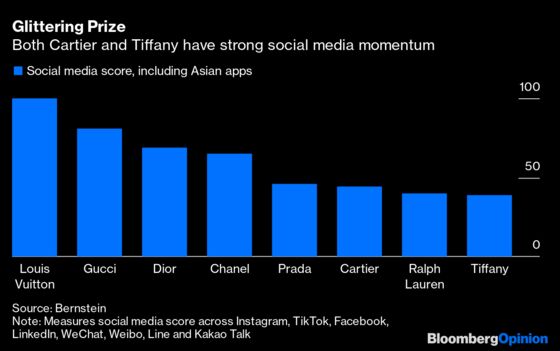

LVMH needs to bulk up in the faster-growing jewelry market, where it lacks scale — that’s why it struck the deal with Tiffany in the first place. Richemont is currently the world’s biggest branded jeweler by market share, according to Bloomberg Intelligence. And it’s not just thanks to Cartier, which has gained a strong following among millennials. Richemont also owns Van Cleef & Arpels.

Unlike Tiffany, Richemont is not a pure jeweler. It has a sizeable watch business, as well as pen-maker Montblanc and a collection of fashion-and-accessories brands including Chloe and Dunhill. And then there is Yoox Net-a-Porter, a luxury online retailer.

Richemont would be a much bigger acquisition for LVMH than Tiffany, giving Arnault an even more dominant position in luxury. Annual sales of the combined group would be four times that of nearest rival, Gucci-owner Kering SA.

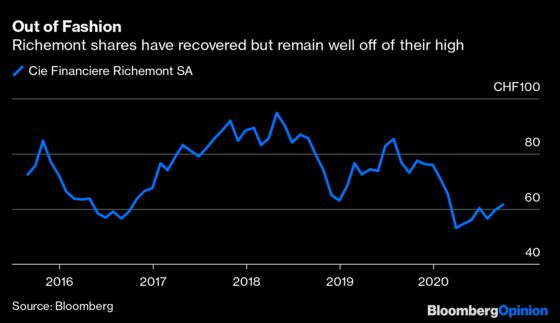

A deal of this size isn’t impossible for LVMH. The Geneva-based Richemont has a market capitalization of about 35 billion Swiss francs ($38 billion). Assuming the 30% premium that investors would typically expect, that would mean an offer price of about 45.5 billion francs, equivalent to about three times the price of Tiffany. Even at this level LVMH’s net debt at the end of 2021 would still be less than 2.5 times the estimated Ebitda for the combined group.

Its temping to think that LVMH could do both deals. But that isn’t practical, primarily because it would likely have to pay a bigger premium than that 30% for Richemont. After all, Richemont’s chairman, Johann Rupert, is going to need some persuading to sell when the stock is still relatively depressed. He holds 10% of the equity and 51% of the voting rights. He insisted in May that the company had no intention of merging or being acquired. What’s more, his 33-year-old son Anton joined the board in 2017, paving the way for a possible handover to the next generation.

To convince him, LVMH would have to pay more. It could afford a 60% premium in a cash-only bid and still keep the leverage ratio below 3 times. And that’s before any disposals. While YNAP has underperformed, it could still be worth about $6 billion because online shopping is booming and tech stocks have been soaring.

Alternatively, LVMH could offer a mixture of cash and shares. That would enable Rupert to participate in the potential upside brought by bringing the two luxury conglomerates together.

Of course, all this is academic right now. LVMH must first convince a U.S. court to release it from its Tiffany engagement. A hearing is set for early next year.

Immediately falling into the arms of another bride after that might look more like something from a trashy reality TV show than the rarefied world of luxury. Arnault’s reputation may suffer. But as with securing the most favorable terms for Tiffany, he has a duty to his shareholders to get the best prize. If that is the owner of Cartier, then it’s a risk worth taking.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2020 Bloomberg L.P.