For the Luxury Crowd, SPACs and Suits Are So This Season

(Bloomberg Opinion) -- Luxury deals are so this season.

On Tuesday, LVMH Moet Hennessy Louis Vuitton SE, the world’s biggest luxury company, said it would buy 60% of Off-White, the streetwear label founded by Virgil Abloh, the creative director of Louis Vuitton’s menswear line.

A day earlier, Ermenegildo Zegna, the 111-year-old Italian fashion house, announced that it would list in New York via a $3.2 billion deal with a special purpose acquisition company, or SPAC, whose chairman is Sergio Ermotti, the former chief executive officer at UBS Group AG.

Two days, two very different transactions. But both say something about the business of bling. Luxury groups big and small are repositioning themselves in an industry reshaped by the pandemic.

Amid the crisis, power brands, such as LVMH’s Louis Vuitton and Christian Dior, as well as Hermes International, have thrived, as consumers put their lockdown savings toward more expensive iconic products.

For LVMH, taking a stake in Off-White for an undisclosed sum is about strengthening its ties with Abloh. He has helped turbocharge Louis Vuitton, making it more contemporary and inclusive. LVMH doesn’t want to lose that halo effect.

The company said the partnership will not be limited to clothing and accessories. That’s important because prior to the pandemic, luxury groups were starting to offer up more experiences. As economies open up, they will once more want to capture a slice of the spending on travel and fine dining. Imagine: Abloh could help LVMH launch Gen Z-friendly brands in furniture, drinks, jewelry and hospitality.

Smaller houses have found pandemic life much more demanding, however. One main challenge is standing out in a crowded market, where expensive digital and social media engagement is imperative.

Zegna saw sales fall 23% in 2020, to just more than 1 billion euros ($1.2 billion), creating a 45 million-euro net loss. The menswear brand has also faced a battle in trying to pivot from its trademark top-end suits to more casual styles.

It is not alone in trying to reposition itself. Prada SpA and Burberry Group Plc are in the midst of turnarounds. Fellow Italian house Salvatore Ferragamo SpA recently poached Burberry CEO Marco Gobbetti to spearhead its revival. Even Moncler SpA, one of the most successful names outside of a conglomerate, has become a consolidator itself.

Smaller brands often have little choice but to sell out, either to one of the big luxury groups or to private equity. (Etro SpA, another Italian fashion house, just sold a majority stake to L Catterton, the buyout fund backed by LVMH.) For privately owned or family-controlled businesses, Zegna’s deal offers another option to tap into investor cash while the founders retain a majority stake. And with many SPACs hunting for targets, this route could prove more lucrative too.

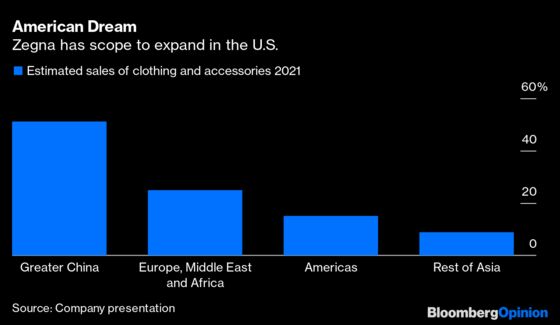

Listing via a blank-check company provides acquisition currency and greater visibility in the U.S., where the group wants to expand. Zegna currently generates more than 50% of its clothing and accessories sales from China. Roughly half of the $880 million proceeds from the deal will be used to develop the business, both in clothing and accessories, and in the division that supplies other luxury groups.

Of course, there are risks along the way for both LVMH and Zegna.

For LVMH, it is simply that Abloh loses his cool factor. The Off-White deal has parallels with LVMH’s 1997 purchase of a majority stake in Marc Jacobs’ eponymous label, when the American designer became creative director of Louis Vuitton. But after determining the direction of fashion in the 1990s and early 2000s, the Marc Jacobs brand lost its way. For the past few years, LVMH has been trying to improve its performance.

But the conglomerate is expected to generate sales of almost 60 billion euros this year. The stake in Off-White and investment in any subsequent ventures with Abloh remains a tiny bet.

That’s not the case for smaller groups trying to reinvent themselves.

For Zegna, the danger is that its pivot to casual wear, which has so far made good progress, stalls. This would hurt its broader sales and profit targets, as well as jeopardize its goal to have more than half of the brand’s sales of clothing and accessories from leisurewear.

There is one risk that unites both of these companies at opposite ends of the luxury spectrum: What if the high-end market slows?

The industry has benefited from so-called revenge spending, as consumers in China and the U.S. have diverted the money they would have spent on vacations to premier watches and handbags. The tapering of lockdowns means shoppers now have more calls on their cash.

As LVMH and Zegna bet on bold new looks, they need the bling bubble to stay strong or deflate slowly, rather than burst.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2021 Bloomberg L.P.