(Bloomberg Opinion) -- Advent calendars are bang on trend right now, and Tiffany & Co. is selling one of the most indulgent ever. For $112,000, lucky recipients can open little blue windows to reveal bangles from its Tiffany T line, delicate floral earrings, silver novelties and perfume.

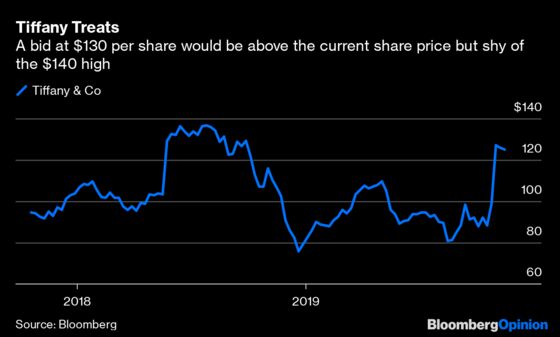

Reflecting the sheer luxury of it all, LVMH Moet Hennessy Louis Vuitton SE has made a revised proposal to buy Tiffany at $130 per share, valuing the U.S. jeweler at about $16 billion including assumed net borrowings.

Its previous approach at $120 per share was too skinny. At the higher level, both sides stand a chance of getting a nice gift in the countdown to the holidays. LVMH should be able to make a return on investment that exceeds the target’s cost of capital. Tiffany investors would receive a 32% premium to the price of the company’s shares before Bloomberg News revealed the initial approach.

At $130 per share, LVMH will probably want to increase Tiffany’s operating profit contribution to around $1.5 billion in order to generate a 7-8% post-tax return. Given the French group’s scale and track record, that’s feasible.

LVMH has more than doubled sales at Bulgari, which it acquired in 2011. But the Italian jeweler is a misleading benchmark: An equivalent feat at Tiffany looks ambitious given that it’s a much bigger company.

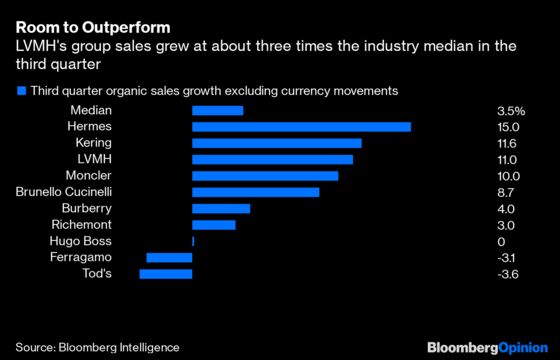

Analysts aren’t anticipating much growth for Tiffany’s sales this year, according to the consensus of Bloomberg estimates, but revenues are expected to increase about 4% in 2021 and 2022. Deborah Aitken of Bloomberg Intelligence puts the long-term growth of the jewelry market at 5% a year. LVMH expanded its overall group sales in the third quarter at about three times the industry median, Aitken notes.

On that basis, it has scope to outperform the jewelry market, too. To achieve this, LVMH would likely accelerate Tiffany’s retail expansion in Asia. With its financial clout, it could also turbocharge product development, and back new styles with more muscular marketing. Meanwhile, it could better fulfill Tiffany’s broader potential in lifestyle segments, such as fragrances and watches.

So a more realistic forecast would be that under LMVH, Tiffany’s sales could grow a bit, but not much faster than the market — say 7% per year. After five years, sales would be 40% higher than this year, or around $6.3 billion.

Margins would have to climb to 23% to hit the profit hurdle. Again, that’s plausible. In the short term, profits could well take a hit, as the new owner invests in products and stores. But with analysts at Royal Bank of Canada estimating Cartier’s operating margin at comfortably over 30%, and Van Cleef & Arpels and Bulgari each in the low-to-mid 20s, there is potential to lift Tiffany’s margin, which is anticipated at near 18% this year.

Each side has something to gain from a transaction. For LVMH, that’s dominating the market for jewelry. For Tiffany, it is avoiding the tricky task of executing a turnaround in a U.S. recession on its own.

The U.S. group’s strategy, including introducing new designs that appeal to younger customers, is a sensible one. But it has yet to deliver fully, and that’s before any sign of a downturn. If its suitor walks away, it would likely struggle to convince investors that it can maintain the share price around current levels without takeover interest. It was trading at $98.55 before LVMH’s approach.

With the two sides entering talks, Tiffany will be pushing for an even higher price. Analysts at HSBC see potential for a deal at $135 per share. LVMH shares fell 1% on Thursday.

But with no signs of a counter bidder emerging right now, LVMH Chief Executive Officer Bernard Arnault has the upper hand. Just because he can afford it doesn’t mean he should be as extravagant as one of those advent calendars.

--With assistance from Chris Hughes.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.