(Bloomberg Opinion) -- When the coronavirus pandemic struck the U.S. in early March, among the first reported casualties was the $3.9 trillion market for states and local governments.

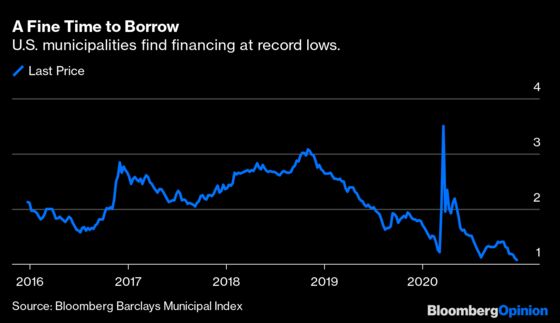

The yield on municipal debt sold by almost 2,000 borrowers with more than 55,000 outstanding securities hovered at 1.14%, the lowest since at least 1979, when the Bloomberg Barclays U.S. Municipal Index began compiling data. But panic suddenly seized investors, and prices suffered their biggest weekly decline in 33 years, with insurers MBIA Inc. and Assured Guaranty losing more than a quarter of their value.

“This is the worst that I have seen in terms of market reaction and illiquidity in my career,” Christopher Brigati, head of municipal trading at Advisors Asset Management Inc., told Bloomberg News. “It's not unlike the 2008-09 financial crisis, but worse.”

That was then. During the ensuing nine months, Congress struggled to provide a second relief package amid resurgent Covid-19 cases and deaths. This was partly because President Donald Trump and Republican senators resisted giving money to the most populous Democratic-led states, such as California, Colorado, Illinois, New Jersey and New York, which they assailed as mismanaged. These governments still arranged the most tax-exempt financing in 10 years at a cost that was the lowest in at least four decades.

No doubt the bonanza for governors, mayors and bondholders during the worsening national peril was made possible by the Federal Reserve lowering its benchmark interest rate barely above zero and the Fed's Municipal Liquidity Facility (MLF), which was set up in the pandemic as a backstop to immediate municipal borrowing. Investors stampeded back into the market, pushing the borrowing cost to 1.08%, the record low.

Anyone in a 28% tax bracket who purchased municipal bonds on March 23 when the yield on the Bloomberg Barclays municipal index surged to 3.53% has a tax equivalent total return (income plus appreciation) of 19.1%. That's because the market remains close to the record-low yield of 1.08% it hit on Dec. 21. Investors who snapped up bonds sold by Illinois and New Jersey have equivalent total returns of 24.6% and 22.2%, respectively, according to data compiled by Bloomberg. A basket of all types of U.S. debt returned just 6% when benchmark U.S. Treasuries were little changed.

Recent history suggests states and local governments, with or without federal assistance, will reap the benefits of low yields at the moment when they need money most. The relative borrowing cost for Illinois, which, at $137 billion, has among the worst levels of unfunded pension liabilities in the nation, narrowed to 50 basis points at the beginning of the year compared with the rest of the U.S., continuing a decade-long trend of historically low-cost financing. The spread has since narrowed to a level that is 10 basis points below the five-year average.

Even during the March turmoil, Illinois was poised to borrow well below the 4.78% it was forced to pay in 2008. It now has 17,000 outstanding municipal securities totaling $82 billion with an average coupon of 4.3% that can be called, or refinanced, at lower rates.

Sure enough, Chicago's O'Hare International Airport in September sold $1.2 billion of revenue bonds maturing in 2039, yielding 1.9% currently. New Jersey State Transportation Trust last month sold $1.5 billion of revenue bonds due in 2050 and yielding 3%. Proceeds from the sale will be used to fund various transportation improvements. Denver City & County Airport sold $629 million of securities maturing in 2035, yielding 2.6%. Proceeds will be used refinance existing debt at lower rates.

All told, states and local governments this year will match or exceed the decade-high $478 billion of new offerings in 2016. That's because the appetite for tax-exempt securities shows no signs of abating when the yield on municipal debt remains relatively high.

The largest exchange-traded fund investing in municipal bonds, iShares National Muni Bond ETF, issued almost 170 million shares, a record since its inception in 2007. During the second quarter, when yields plummeted from the Covid-19 peak, more than $1.5 billion flowed into fund.

To be sure, some of the market's incentives are about to go away if the Trump administration gets its way. Treasury Secretary Steven Mnuchin's decision to end the Fed’s MLF — approved earlier this year under the federal CARES Act — could increase risks for many borrowers.

“New Jersey knows this better than most,” Elizabeth Maher Muoio, the state's treasurer, wrote earlier this month. “On the same day that Secretary Mnuchin announced his refusal to extend the deadline for this emergency lending program,” the state sold general obligation bonds yielding less than 1.95% and providing $4.28 billion of proceeds. “While we ultimately did not need to use the MLF, the facility's presence served to stabilize the municipal market in the months leading up to New Jersey's bond sale, allowing us to obtain the extremely favorable rates we received.”

(With assistance from Shin Pei and Rick Bialos.)

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew A. Winkler is Co-founder of Bloomberg News (1990) and Editor-in-Chief Emeritus; Bloomberg Opinion Columnist since 2015; Co-founder of Bloomberg Business Journalism Diversity Program in 2017. During his 25 years as Editor-in-Chief, Bloomberg News was a three-time finalist and winner of the Pulitzer Prize for Explanatory Reporting and received numerous George Polk, Gerald Loeb, Overseas Press Club and Society of Professional Journalists and Editors (Sabew) awards.

©2020 Bloomberg L.P.