Low Rates and Low Inflation? Not Always on Main Street

(Bloomberg Opinion) -- For those in finance and finance-related industries, it’s easy to get lured into sweeping generalizations about the state of the American economy. I can’t begin to estimate how many times I’ve heard some iteration of “the U.S. consumer remains strong,” or “stubbornly low inflation,” or “it’s a great time to be a borrower with rock-bottom interest rates.”

So I give a lot of credit to Bloomberg News’s Christopher Maloney and Adam Tempkin for shattering that boilerplate with an article this week about the boom in online installment loans. Provocatively titled “America’s Middle Class Is Getting Hooked on Debt With 100% Rates,” it undercuts much of Wall Street’s assumptions about life across the country.

Are all American consumers really that strong? Perhaps not, judging by how subprime borrowers owe some $50 billion on installment products. Is inflation frustratingly low? Maybe by historical averages, but in the 10 years through 2018, crucial budget items for middle-class households like home prices, medical care and college tuition have soared at a much faster pace than average incomes, potentially driving people to alternative credit providers. And as for those ultra-low interest rates so often bandied about?

Enter the online installment loan, aimed in part at a fast expanding group of ‘near-prime’ borrowers -- those with bad, but not terrible, credit -- with limited access to traditional banking options.

Ranging anywhere from $100 to $10,000 or more, they quickly became so popular that many alternative credit providers soon began generating the bulk of their revenue from installment rather than payday loans.

…

For subprime lender Enova International Inc., outstanding installment loans averaged $2,123 in the second quarter, versus $420 for short-term products, according to a recent regulatory filing.

Larger loans have allowed many installment lenders to charge interest rates well in the triple digits. In many states, Enova’s NetCredit platform offers annual percentage rates between 34% and 155%.

That number — 155% — is stunningly high. Granted, it’s not as if online installment loans are necessarily the first type of debt incurred by Americans, nor are they a particularly large share of obligations. Total household debt reached a record $13.86 trillion in the second quarter, according to data from the Federal Reserve Bank of New York. More than two-thirds of that is mortgages, while loans for college and automobiles are consuming ever-larger shares of balance sheets.

Still, triple-digit interest costs are unthinkable for individuals, corporations or governments with pristine credit. The Bankrate.com 30-year fixed mortgage lending rate fell earlier this month to 3.68%, not far from the all-time low of 3.32% in September 2016. Deere & Co. set a record in September for the lowest-yielding 30-year investment-grade corporate debt, at 2.877%. Even though the yield on the longest-dated U.S. Treasuries dropped to an unprecedented low in late August, President Donald Trump is imploring the Fed to emulate Europe and Japan and drop interest rates below zero.

For those relying on installment loans, the concept of being paid to borrow money surely sounds like an alternate reality. California has actually taken measures to cap the interest rate on loans between $2,500 and $10,000 — to 36% plus the fed funds rate. Compared with an annual percentage rate of more than 100%, I guess that’s a borrower-friendly move.

It’s always risky to draw broad conclusions about household credit trends. The sevenfold increase in online installment loan volume since 2014, for instance, can mean two things, depending on your worldview. For those with a gloomy take on the U.S. economy, it’s a sign of how the working class has been forced to take on onerous debt to keep up with their higher cost of living. For the more optimistic onlookers, it indicates that individuals with marginal credit scores are confident enough in their financial position to borrow, even if they’re still locked out from traditional banks. In the words of Jonathan Walker, who heads Elevate Credit Inc.’s Center for the New Middle Class, “there has been a lot of innovation to meet the consumer where they are.”

Similarly, the New York Fed’s data has a mix of good and bad economic news. On the bright side, 95.6% of households were current on their debt payments in the second quarter, the largest share since 2006. However, those considered “severely derogatory” on payments made up almost half of all delinquencies, the largest share ever. My conclusion was that in the current economy, you either have the money to pay back what you owe or you don’t.

But even that might be too simplistic. Looking out over the coming years, some analysts suggest FICO credit scores from Fair Isaac Corp. have been artificially boosted over the past decade and overstate how many borrowers could pay back what they owe in an economic downturn. Online installment loans are among the debt most vulnerable to inflated scores. So are credit cards — and card issuers ramped up the percentage of loans they expect will never be repaid in the first quarter to a seven-year high of 3.82%. The so-called charge-off rate has since come down to 3.33%.

Perhaps some credit is due to Fed Chair Jerome Powell, who is widely expected on Wednesday to announce the central bank’s third interest-rate cut since July. He has reiterated at every opportunity that he and other officials are acting as they see fit to sustain the economic expansion, with a focus on funneling the benefits of a strong labor market and rising wage growth to people who have missed out thus far. They’ve kept the U.S. economy chugging along.

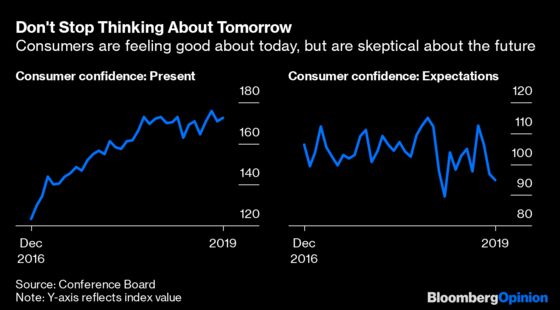

And yet it feels as if the economy remains at a crossroads. Conference Board data released on Tuesday showed that U.S. consumers are as confident about their current situation as they have been in the past 19 years, while their outlook for the future is the most dour since January.

Layer that cautious macro view on top of the more micro elements of household debt balances, including the surge in online installment loans, and an image begins to emerge of a precarious situation for a swath of Americans. It’s a picture of the economy that Wall Street too often blurs out.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.