Looking for a Stock Boost? Just Wait for Earnings Season

(Bloomberg Opinion) -- With first-quarter earnings season about to get underway, many investors are worried that budding economic uncertainty caused by high inflation and Federal Reserve rate increases could jeopardize the recent rebound in U.S. stocks. But historical experience suggests quite the opposite.

Indeed, earnings seasons usually propel stocks to above-average returns, especially during periods of high economic and policy uncertainty. The positive effect has even intensified during the pandemic as the somewhat permanent impairment in confidence has allowed company reports to spark repeated relief rallies in stocks when the results aren’t as bad as feared. Likewise, analysts and companies have erred on the side of caution in both estimates and commentary, allowing for an extraordinary pace of earnings beats to unfold repeatedly in recent quarters. More beats to expectations in turn bring even greater relief, which pushes up stock prices.

Over the past two decades, earnings seasons — defined here as weeks when more than 50 members of the S&P 500 Index report results — have produced stronger-than-average weekly S&P 500 returns. From 2000 to 2022, during the 293 weeks considered part of earnings seasons, the S&P 500 returned a weekly average of 22 basis points, double the weekly average of 11 basis points in non-reporting weeks.

Despite conventional wisdom, fears of an economic slowdown combined with the Fed’s tightening of monetary policy may only intensify the historically positive effect of earnings seasons. Indeed, higher weekly returns during earnings seasons are usually stronger when the Fed is not easing or economic confidence is low or both.

Stock prices obviously rose faster when the Fed expanded its balance sheet than when it took its foot off the gas. However, it might come as a surprise that even when the central bank’s balance sheet wasn’t expanding (mid-2011 through 2012 and late 2014 to late 2019) the S&P 500’s weekly return was more than three times greater during reporting weeks than it was outside of earnings season on both a median and average basis.

Likewise, S&P 500 returns averaged 85 basis points during high reporting weeks in the three recessions since 2000 compared with a loss of 70 basis points in the other weeks of those recessions. And since the pandemic began, earnings seasons have been extraordinarily strong for stocks, with returns more than double those in the average earnings week before Covid-19 emerged. The spread between returns in and out of earnings season has also widened, to an average 27 basis points from 9 basis points in the pre-pandemic years from 2000 to June 2020.

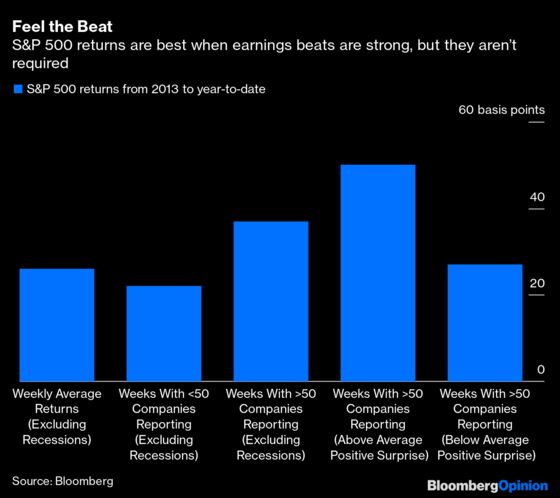

Since the second quarter of 2020, company earnings have significantly beaten analysts’ estimates, with earnings-per-share growth doubling expectations in the quarters since then, most likely turbocharging stocks’ performance during reporting weeks over the past two years. Although it seems unlikely that another high share of expectation beats in the coming earnings season could produce the same result, even a reversion to the normal beat rate or below may not be enough to dampen the earnings season shine; even below-average beat rates have historically resulted in above-average returns for stocks during earnings seasons.

In the years before the pandemic for which data is available on price returns relative to beats and misses (fourth quarter 2013 to fourth quarter 2019), an average of 74% of companies beat analysts’ EPS expectations each quarterly reporting season. In reporting seasons with higher-than-average beat rates, the S&P 500 average return was 50 basis points, compared with 27 basis points during seasons with below-average beat rates.

Quite clearly, strong beats in recent years have amplified the typical positive response to earnings reports at large. The average earnings beat rate rose to 83% from the second quarter of 2020 to the most recent quarter as pandemic fears acted as a vise grip on analysts’ forecasts. Weekly price returns for all weeks since the second quarter of 2020 have averaged 47 basis points, but during earnings season, they have averaged 70 basis points. Returns were strongest when the beat rate was highest, with an 84-basis-point average return accompanying a beat rate of 87% in the second quarter of 2021.

Recent analyst revisions and trends in company guidance suggest the abnormal pandemic-era beat rates and earnings season returns may be coming to a close. In contrast to the pandemic pattern of analysts raising their estimates ahead of the coming earnings season, analysts spent the better part of the first quarter marking down their expectations. Indeed, S&P 500 EPS growth forecasts fell persistently for the first two months of the year only to rise again over the last month as analysts have started to get a better feel for ultimate results of the quarter. Company guidance has likewise reverted to a more normal state in which negative revisions outpace positive ones. However, history shows a more normal earnings environment is still usually kind to stocks. Indeed, most earnings seasons simply offer another reminder that there is some reason for optimism.

More From Other Writers at Bloomberg Opinion:

- If Stocks Don’t Fall, the Fed Needs to Force Them: Bill Dudley

- Ukraine War Hastens Move to Private Markets: Mohamed El-Erian

- Do Rate Hikes Always Hit Growth Stocks? Think Again: Nir Kaissar

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Gina Martin Adams is the global head of portfolio strategy and chief equity strategist for Bloomberg Intelligence. Prior to joining Bloomberg, she was the head of U.S. equity strategy for Wells Fargo Securities.

©2022 Bloomberg L.P.