(Bloomberg Opinion) -- Two potential initial public offerings highlight the stiffening competitive pressure on London as a venue for raising capital. Post-Brexit, it may no longer be the natural choice for European companies. And it’s still struggling to catch up with the U.S. as a favored arena for technology and biotech firms.

CVC Capital Partners is leaning towards listing on the Amsterdam exchange if market conditions enable it to proceed with an IPO, the Financial Times reported. That may make sense for CVC, one of Europe’s largest buyout firms. But there’s no doubting it’s a setback for London.

The recent private-equity related floats in London have performed poorly. Bridgepoint Group Plc is down about 15% since its July debut, while Petershill Partners Plc has dropped nearly 30% since its September stock sale. While shares in the main U.S.-listed buyout firms have also been weak, they haven’t fared as badly. Moreover, Bridgepoint’s decision not to disclose what its senior ranks earn from investment-fund performance fees, combined with some jumbo signing bonuses for non-executive directors, have made it a lightning rod for corporate-governance concerns.

The standard bearers for listed European private equity — EQT AB and Partners Group Holding AG – are on the exchanges of Sweden and Switzerland, respectively. And within Europe, Amsterdam has been at pains to establish itself as the neutral venue post-Brexit, a home to companies regardless of domicile and sector. On that, it’s arguably made more headway than either Paris or Frankfurt.

London may have to let CVC go and take it on the chin. There are bigger listings to worry about — notably microchip designer ARM Ltd., now being prepared for IPO by parent Softbank Group Corp. after a sale to chipmaker Nvidia Corp. was blocked on competition grounds. Softbank founder Masayoshi Son has earmarked Nasdaq for the deal. But that’s not been formalized just yet, and U.K. lawmakers are keen to see ARM regain its former British listing.

The transatlantic debate for Softbank is simple. Let ARM jostle with its failed suitor for investor attention in New York, with that market’s broader audience of technology investors and analysts. Or capitalize on the scarcity value of tech companies on the London bourse, whose largest constituents are predominantly mature, low-growth income stocks.

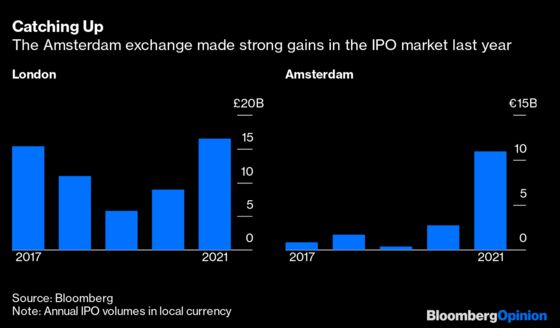

In 2021, London had its best year for IPOs in more than a decade, with 17 billion pounds ($22 billion) raised. Amsterdam IPOs garnered just 11 billion euros ($12 billion). Russia’s invasion of Ukraine has halted capital-raising activities. Whenever the new-issues market reopens, London Stock Exchange Group Plc clearly cannot afford any complacency, and the choices facing CVC and Softbank neatly encapsulate the strategic challenge it faces. A resurgent Amsterdam may prove more attractive to firms that want to build both financial and political capital in Europe; technology and biotech firms may yet prefer to join the U.S. crowd than become U.K. national champions.

The U.K.’s listing regime is currently undergoing a radical overhaul designed to attract more companies, supposedly taking advantage of Brexit. But there’s only so much the City can do to make London feel like home.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2022 Bloomberg L.P.