(Bloomberg Opinion) -- China’s most ubiquitous company is hiding one of its most valuable assets. That needs to change.

Tencent Holdings Ltd., best known for the WeChat messenger that almost everyone in the country uses, has a growing fintech business. But it’s getting overshadowed by the games and social media divisions. By spinning it off into a new company, with a move to a separate listing, management could unlock as much as $230 billion in value. That would make the entity China’s fourth-largest listed company and the world’s sixth-biggest financial services firm.

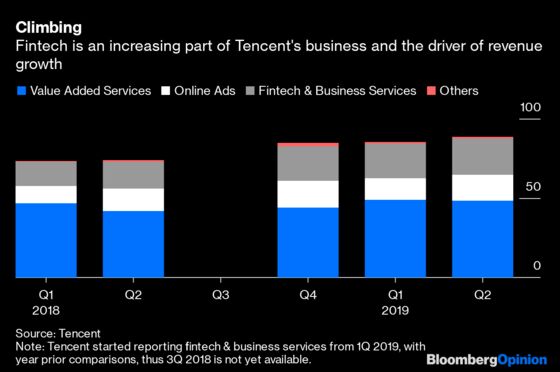

Such a move could help Tencent retake some of the limelight that it’s about to share with Alibaba Group Holding Ltd. once that company lists in Hong Kong. Alibaba’s fintech unit, Ant Financial Services Group, already functions as a separate business with the e-commerce giant holding a 33% stake. At Tencent, fintech and business services accounted for 26% of revenue last quarter. The Shenzhen-based company is due to report third-quarter earnings late Wednesday.

I estimate that revenue from Tencent’s fintech business grew in excess of 70% last year. The vast majority of that was payments. Yet Tencent also offers other products such as wealth management and has a 30% stake in WeBank, China’s first online-only bank, which was founded five years ago. Data on its fintech profits are hard to ascertain, yet information disclosed by Alibaba shows that Ant Financial was unprofitable last year, so Tencent could be in a similar boat.

That’s not necessarily a bad thing. The two rivals are startups in the classic sense, using fast revenue growth driven by marketing and incentives to gain ground fast. A major reason why both have lost money in recent years is due to low take rates, the commissions received from processing payments, because they’ve offered discounts to consumers and merchants.

A turnaround could be near, Sanford C Bernstein senior analyst David Dai wrote in a recent series on China’s fintech sector. He estimates that a maturing market will ease cut-throat competition and allow both companies to take a greater share of the money that sloshes through their payments platforms.

As a result, Tencent’s payment business (TenPay) alone could be worth $137 billion, compared to $127 billion for Ant’s AliPay, the Bernstein team figures. HSBC Holdings Plc uses two methodologies to come up with an estimated value of around $128 billion. Throw in the other products, and Bernstein calculates a base-case valuation for Tencent’s fintech unit of $160 billion, going as high as $230 billion. This indicates that 40% to 58% of Tencent’s current market cap is locked up in this hitherto hidden division. Bernstein has a base case of $210 billion for Ant, reaching as high as $320 billion.

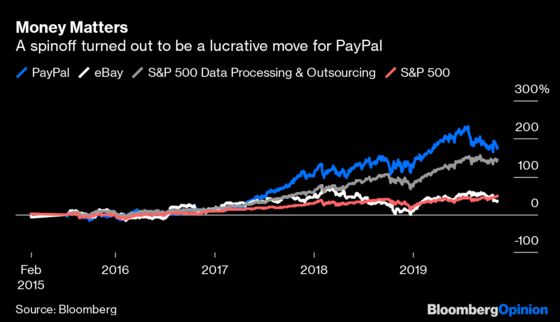

Payments spinoffs have proven to be lucrative in the past. EBay Inc. proved it with PayPal Holdings Inc. in 2015, with the latter posting a 177% normalized return since then, outpacing the 145% rise in the S&P Data Processing sub-index which includes Visa Inc. and Mastercard Inc. PayPal also trounced both eBay (35%) and the S&P 500 (49%). Square Inc., another payments provider, has been one of the hottest stocks of the past decade, returning more than 590% since its initial public offering in 2015.

A more recent example comes from India, where Walmart Inc. is reported to be spinning off payments business PhonePe from local e-commerce company Flipkart Group, which it acquired last year. That transaction could turn a $20.8 billion startup into two unicorns with a combined value of more than $30 billion.

Tencent doesn’t need to rush to list this fintech unit. Appetite for mega IPOs is likely to be satiated by Alibaba’s Hong Kong listing and that of Saudi Aramco over the next few months. And there’s a long runway of big startups ready for their moment in the sun. By merely making it a separate entity, management can signal intent and allow investors to start re-rating Tencent’s stock accordingly.

An offering may not even be necessary, since Tencent is already sitting on more cash than it needs. Instead, the company could distribute shares in Tencent Fintech to existing shareholders, and then directly list the stock. That’s similar to the approach advocated by activist investor Dan Loeb for a Sony Corp. split.

Tencent is sitting on a bright light in this fintech unit. Time to let it shine.

The "others" category includes fintech, cloud, film & TV. Tencent noted that fintech is the major component and gave a figure for cloudbut not content.

HSBC Approach 1: valuation per user. Approach 2: Using Tencent operating margins applied to its payments business, then comparing to peers.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.