(Bloomberg Opinion) -- An advertisement showing in U.K. cinemas currently shows a boy hesitating to kiss a female zombie. “But I’m kinda hot,” she says, popping chewing gum into her mouth before they lock lips — and her arm drops off. The finance community has a similarly conflicted relationship with Libor, the reference interest rates for everything from mortgages to car loans to corporate debt. This makes it likely that the benchmarks will survive beyond their planned termination date.

The current plan is for Libor to wink out of existence by the end of 2021. Changes in the wholesale funding market mean it’s no longer based on actual transactions between banks. The Financial Conduct Authority is adamant that the U.K. finance industry should shift to using the Sterling Overnight Interbank Average rate (known as Sonia). In other jurisdictions, including the U.S. and the euro area, regulators are implementing replacements.

But with a bit more than two years to go, a combination of complacency, complexity and inertia is keeping Libor very much alive.

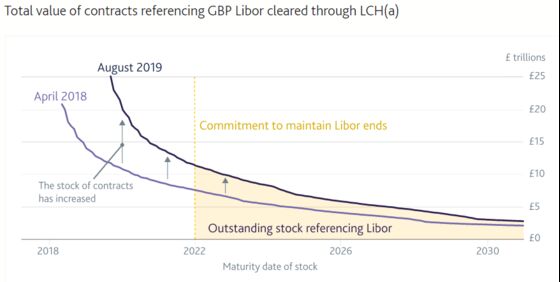

The Bank of England’s “Bank Overground” blog pointed out recently that the value of sterling swap contracts referencing Libor is increasing rather than decreasing, according to data compiled by LCH Ltd., the derivatives clearing house.

The value of contracts that extend beyond Libor’s mooted end date has increased since April 2018, and stands currently at more than 10 trillion pounds ($12 trillion), as the chart above shows. Even by 2026, more than 5 trillion pounds of Libor swaps will still be outstanding. “Use of Libor remains widespread, and this poses risks to market stability,” the Bank of England blog says.

There has been some progress in moving financial products to the regulators’ recommended replacement. Earlier this month, Royal Bank of Scotland Group Plc’s NatWest unit switched the reference rate on an existing loan to South West Water to Sonia. In July, the same bank made the first new loan based on Sonia, to National Express Group Plc.

Of course, some of the warnings about the need to accelerate away from Libor are self-serving. Consultants and lawyers will make money from offering expensive advice on the transition; it’s in their interests to emphasize the dangers.

But the sheer volume of outstanding notes around the world still tied to Libor and expiring after 2021 — as much as $864 billion, the International Capital Markets Association estimated earlier this year — leaves many financiers skeptical that the regulators will carry out their threat to kill off the benchmarks as planned.

A survey published last month by consulting company Accenture Plc showed 23% of respondents expect Libor to survive past its current death date. The poll of 177 global banks, asset managers and companies showed just 18% of the respondents described their shift away from the benchmarks as “mature,” with only one-fifth saying they were “operationally ready.”

Regulators face a tough choice. If Libor wins a stay of execution, there will be even less pressure to switch away from the old reference rates. But if they stick to their guns, billions of dollars and euros and pounds of contracts will come untethered as the interest rates on which their payments are based disappear.

That risk is too big to ignore. Sure, Libor is flawed and outdated and probably beyond redemption. But with less than 27 months to go, the finance industry needs more time to come to terms with its demise. Let Libor live on. Sometimes even a zombie can be hard to resist.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.