(Bloomberg Opinion) -- It’s generally accepted that one of the keys to a healthy economy is a robust banking system. For some reason, though, central banks seem intent on doing everything in their power to make it as hard as possible for banks around the world to thrive. And so now, as they embark on a fresh round of monetary policy easing to combat the global synchronized slowdown, here’s hoping they find ways to actually spur the economy without penalizing the institutions that are the key to their success.

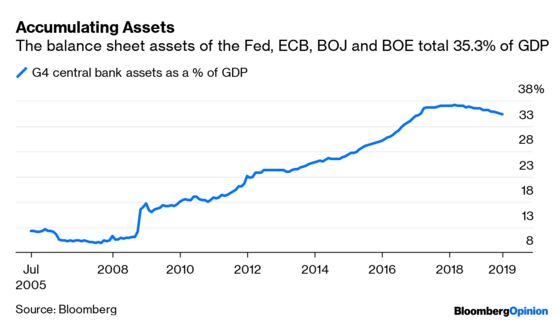

It’s been a decade since the global financial crisis, and despite years of zero or even negative interest rates and trillions of dollars pumped into the world’s financial system through bond and other asset purchases, central banks are now talking about having to double down. That’s even after the collective balance-sheet assets of the Federal Reserve, European Central Bank, Bank of Japan and Bank of England have expanded to 35.3% of their countries’ total GDP from about 10% in 2008, according to data compiled by Bloomberg.

Such talk has contributed to the expansion of negative-yielding debt around the world to more than $16 trillion and caused yield curves to invert. Rates on government debt globally with seven to 10 years left to maturity are on average 30 basis points below those due in one to three years, steadily expanding from no difference back in March 2018, ICE bond indexes show.

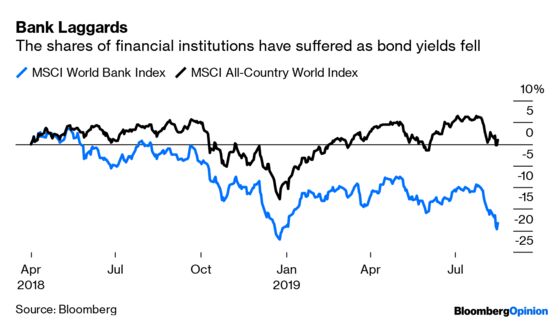

And therein lies the problem for the banking industry, which makes its money by borrowing at low short-term rates and lending the proceeds at higher long-term ones, pocketing the difference. Since the global yield curve inverted 16 months ago, the MSCI World Bank Index has dropped 18%, compared with a small increase of 1% for the broad MSCI All-County World Index of equities. It’s probably no coincidence that when the curve was positive and widening in 2012 and 2013, the bank gauge posted better than 20% annual gains as the global economy was expanding at a 3.5% rate and getting stronger.

What central banks don’t seem to realize is that the problem isn’t that interest rates aren’t low enough. No government, company or individual is saying that credit is too expensive or too hard to obtain. If anything, the issue is on the demand side of the equation. The latest National Federation of Independent Business’s monthly index of sentiment among U.S. small businesses that was released last week included a special question, which asked participants whether a 100 basis-point reduction in borrowing costs would change their capital spending plans over the next 12 months. Only 12% said "yes," while 21% said "no" and 24% said they weren’t sure. Another 43% said they "were not planning on borrowing money."

Interest rates in the euro zone have effectively been at zero since 2014, and yet the IMF projects its economy will expand by an anemic 1.3% this year and 1.6% in 2020. European Central Bank Governing Council member Olli Rehn told the Wall Street Journal on Thursday that the solution is for his colleagues to come up with an “impactful and significant” stimulus package at their next monetary policy meeting in September. Meanwhile, in Germany, the government of the euro zone’s largest economy is preparing fiscal stimulus measures, similar to the bonuses granted in the 2009 crisis, that could be triggered by a deep recession. In reaction, bank stocks in Europe rose on Monday even as bond yields in the euro zone jumped.

It remains to be seen how creative ECB policy makers will get, but the banking analysts at Morgan Stanley say any program that comes with lower rates of even, say, 20 basis points “combined with tiered deposit rates would provide a 5% EPS headwind.” “The lower the ECB pushes rates, the more difficult it will be for banks to remain profitable,” the firm’s strategists wrote in a research report Friday. They also cited research from the National Bureau of Economic Research, which gets to declare when U.S. recessions start and end. The group recently presented a paper at the Federal Reserve Bank of Chicago, asserting that when a central bank’s balance sheet is as large as it is in the euro zone, “a cut in the policy rate into negative territory is actually mildly contractionary.” This is because the negative impact on the banking system outweighs the benefits of lower rates.

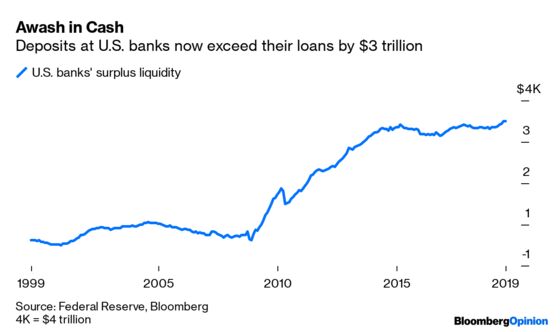

There’s another side effect of low or even negative rates, which is that economists are starting to believe they have the unintended consequence of boosting savings rates as consumers sock away even more of their earnings to make up for lost interest income. At a recent 8.1%, the personal savings rate in the U.S. is double what it was heading into the financial crisis, when the target federal funds rate was 5.25%. That can also be seen in the amount of excess liquidity at U.S. banks, defined as deposits minus loans, which Fed data show has surged to $3 trillion from about $250 billion in 2008.

The banking industry doesn’t engender a lot of sympathy, nor does it deserve any for its role in fostering the abuses and excesses that led to the financial crisis. And nobody is saying that central banks should promote policies that nurture risky behavior. But there’s something to be said for setting monetary policy in a manner that promotes a healthy banking industry rather than hinders its growth.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.