Trump’s $2,000 Stimulus Checks Are a Big Mistake

Family incomes are not down much from Covid-19, and there is a risk of overheating the economy, writes Larry Summers.

(Bloomberg Opinion) -- The attack I made on Bloomberg Television on the idea of universal $2,000 checks as a Covid-19 response has lit up the Twittersphere, so I think it worthwhile to be clear about what I am arguing.

Certainly, I am not opposing stimulus or favoring austerity. For years I have been making the secular stagnation case for more expansionary fiscal policy, and I have often remarked over the last couple of months that “not passing fiscal stimulus is like not wearing a mask at a large indoor gathering — an insane risk.” And both in the immediate term, and on a permanent basis, I am all for strengthening the social safety net with measures such as enlarged Supplemental Nutrition Assistance Program benefits or an expanded Earned Income Tax Credit or child tax credit.

There can be no argument that the stimulus bill Congress passed should be implemented immediately, even though it is too late and too little. As I have observed, it fails to support the states and localities as they try to rehire teachers and health-care workers. It does too little to accelerate the availability of the testing necessary to put Covid-19 in the rearview mirror. And its one-month extension of the eviction moratorium and 11-week extension of unemployment insurance are clearly far too short-term.

The issue is whether spending about $600 billion on a one-time tax credit that would be worth $8,000 to a family of four and reach more than 85 percent of taxpayers makes good economic sense. Victims of Covid-19 disruption can and should receive generous targeted support, as should the poor.

The question in assessing universal tax rebates is, what about the vast majority of families who are still working, and whose incomes have not declined or whose pension or Social Security benefits have not been affected by Covid-19? For this group, the pandemic has reduced the ability to spend more than the ability to earn.

The data are striking. Total employee compensation is now running only about $30 billion per month behind the pre-Covid baseline. Measures in the congressional stimulus bill to strengthen unemployment insurance and to support business will add about $150 billion a month to household income in order to replace all this loss.

The question is whether there is a rationale for further tax rebate of more than $200 billion a month over the next quarter. This would represent additional support equal to an additional seven times the loss of household wage and salary income over the next quarter.

Some argue that while $2,000 checks may not be optimal support for the post-Covid economy, taking stimulus from $600 to $2,000 is better than nothing. They need to ask themselves whether they would favor $5,000, or $10,000 — or more. There must be a limiting principle.

One obvious candidate is not overdoing overinsurance. Bringing working families’ income up to benchmark levels is natural. Perhaps bringing them somewhat above benchmark levels makes sense. But further adding to earnings when losses are being replaced seven times over seems hard to justify — especially at a time when pent-up savings totals $1.6 trillion and is rising. If writing universal checks is a good idea, why not do it after household incomes have reverted to normal?

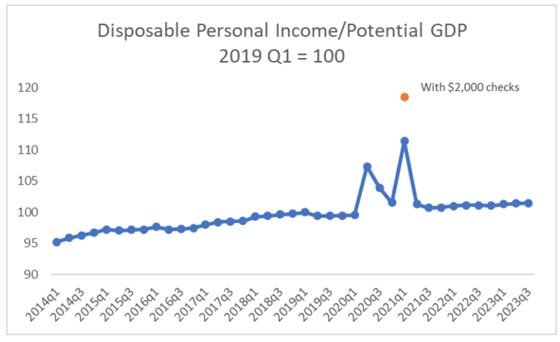

This point is illustrated by the figure below. It shows that because of the legislation passed in 2020, total household income (which takes no account of the stock market) has exceeded normal levels relative to the economy’s potential more or less since the pandemic began. Without new stimulus, things would have normalized in 2021.

But the existing stimulus bill is sufficient to elevate household income relative to the economy’s potential to abnormally high levels — unheard of during an economic downturn. With President Donald Trump’s add-on, we are in completely uncharted territory, with household incomes more than 15% above their normal level relative to economic potential. We frankly have no confident basis for judging how much and how fast this excess, and the pre-existing backlog of saving from the Cares Act, will be spent. There is the possibility of some overheating, particularly if the economy’s potential supply remains constrained by Covid protection measures.

As my recent paper with Jason Furman argues, I am all for a far more expansive approach to fiscal policy. But that does not mean indiscriminate support for universal giveaways at a time when household income losses are being fully replaced and checking account balances (at least as of October) were above pre-Covid levels.

There is no good economic argument for the $2,000 checks, a policy that was not even on the table until the president’s random pronouncement last week. The Democrats seizing this opportunity to pit the president and Senate Majority Leader Mitch McConnell against each other is fair and good politics — but if it leads to actual implementation, it is bad economics. Trump should instead immediately sign the bipartisan relief package that took months to negotiate and avoid a cutoff of unemployment insurance that will plunge millions of the most vulnerable Americans into poverty.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lawrence H. Summers is a Harvard professor and former U.S. Treasury secretary.

©2020 Bloomberg L.P.