Fretting About Inflation May Be Just the Cure We Need

(Bloomberg Opinion) -- Inflation is low. So are interest rates. More than $3 trillion of Covid-19 relief spending in 2020 apparently had no negative macroeconomic consequences. So why are a few top economists suddenly worried about the size of the federal budget deficit? Perhaps because they fear a policy regime change.

When most people hear the phrase “regime change,” they think of war. But in macroeconomics, a regime change means that there’s been a shift in the rules by which policymakers make policy. If the Federal Reserve decides that it’s going to cut interest rates because the economy is bad, that’s just business as usual; It’s following the typical rule. But if it decides that the costs of low rates are lower than it thought, and therefore that interest rates should be maintained at a lower level in general, that’s a regime change.

The kind of regime shift that macroeconomists typically worry about the most is if the government becomes more tolerant toward inflation. In a famous 1982 paper, the Nobel-winning economist Thomas Sargent hypothesized that ruinously high inflation is kickstarted when the government decides to run much bigger deficits in perpetuity and the central bank decides to fund these deficits by creating money. Hence, inflation accelerates because there is no longer the expectation that it will ever be controlled.

Conversely, economists Jonathon Hazell, Juan Herreño, Emi Nakamura and Jón Steinsson, looking at the U.S. experience of the 1970s and early 80s, suggested last year that then-chairman Paul Volcker’s interest rate hikes were able to tame inflation precisely because they strongly signaled that the Fed had become permanently less tolerant of rising prices. They write:

If that’s true, it means that inflation will only strike the U.S. if and when people believe that the government is willing to tolerate it — in econ jargon, if inflation expectations become unanchored from the Fed’s official 2% inflation target.

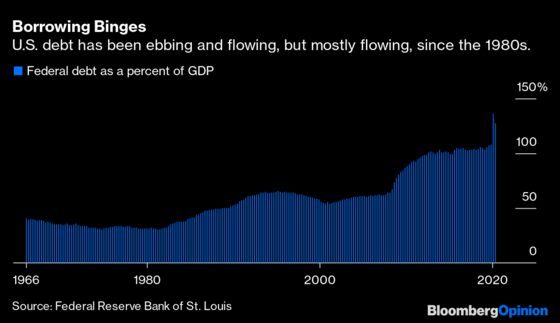

Which brings us to the current situation in the U.S. The government has been racking up quite a bit of debt in recent decades, first as a result of Ronald Reagan’s tax cuts and military buildup, then in response to the Great Recession, and now as a result of Covid-19 relief efforts.

But each of the previous borrowing binges was temporary. The Cold War ended, and Bill Clinton cut deficits. The Great Recession ended, and Barack Obama and the Tea Party Congress worked out a plan (however grudgingly) to raise taxes and slash spending. These episodes of austerity make it seem like there wasn’t really a regime change — the U.S. government was willing to borrow for specific objectives, but would cut it out once those objectives were met. And in fact, inflation never advanced, nor was there significant upward pressure on interest rates.

It seems like Covid-19 ought to be the same. Eventually the pandemic will end, and the need for large deficits will end with it. So why are a few influential macroeconomists, such as Larry Summers and Olivier Blanchard, worried that Joe Biden’s new $1.9 trillion relief bill will cause the country to spiral into inflation, when the even-larger Cares Act Covid relief package didn’t?

Perhaps it’s because they fear that another large spending bill now would signal a political regime change.

Since 1980, federal debt has been on a rising path, but there were always political factors restraining it from growing too quickly. Though Republicans were willing to borrow to fund tax cuts under GOP presidents, they reliably turned into deficit scolds when a Democrat was in the White House. Democrats, in contrast, seemed generally biased toward restraining spending — Clinton balanced the budget in the 90s, and Obama was much more instinctively deficit-hawkish than people realize. This asymmetric, uneasy partisan equilibrium served to restrain the growth of debt somewhat.

But what if that’s all over? Democrats, perhaps realizing that an equilibrium in which only Democratic presidents are deficits hawks favors the GOP, have been signaling that they no longer worry about deficits nearly as much as they used to. Ideas like Modern Monetary Theory — which strongly downplays the risk of government debt — have grown in popularity on the political left. Meanwhile, even as debt has risen, popular concern about it has fallen.

Seeing these developments, economists like Summers and Blanchard might worry that a policy regime change is about to follow — or that the public will believe that one has happened, which would amount to much the same thing. So they might be trying to set themselves up as a counterweight to those who dismiss the importance of deficits, in order to reassure the public that once the Covid-19 crisis ends, leaders will go back to worrying about fiscal prudence.

But given their lack of roles within the Biden administration, economists like Summers and Blanchard might not be the best-positioned to do this. Instead, this is probably a job for the Fed. The central bank should make it clear that if deficit spending leads to substantial inflation — say, over 6% — it will raise interest rates to fight it, even if that means hurting the economy.

That kind of forward guidance would reassure businesspeople and consumers that major inflation isn’t about to be unleashed, and that the Fed is still as responsible a guardian of price stability as it was in the Volcker days. Thus reassured that monetary policy hasn’t undergone a regime change, the public won’t make inflation worries into a self-fulfilling prophecy. And that, in turn, will allow the government to borrow more without the risk of adverse effects.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2021 Bloomberg L.P.