Junk Bonds Prove to Be a Shelter From the Rates Storm

(Bloomberg Opinion) -- The junk-bond market has never offered such low yields. And yet, it might just be the best place for fixed-income investors to ride out the tumult in U.S. Treasuries.

To grasp this, it’s crucial to understand exactly what kind of protection high-yield bonds provide. They don’t insulate investors much from stock-market swoons. I wrote in October 2018 that “Junk Bonds Aren’t Going to Save You,” and indeed the average yield spread jumped about 170 basis points in two months as equities tumbled, saddling speculative-grade debt owners with their worst quarterly loss in more than three years. Treasuries, meanwhile, had their best quarter since early 2016.

The current market is profoundly different. Most notably, Treasuries are swinging wildly: The benchmark 10-year yield surged 14 basis points last Thursday, dropped almost 12 basis points the next day, then after a brief respite jumped 10 basis points on Wednesday. Long-term Treasuries have lost more than 10% already in 2021 and are easily on pace for their worst yearly performance ever as traders anticipate a boom in economic growth and inflation.

Junk bonds are primed to shine in that scenario, at least relative to other fixed-income securities, even if their average yield is little more than 4%.

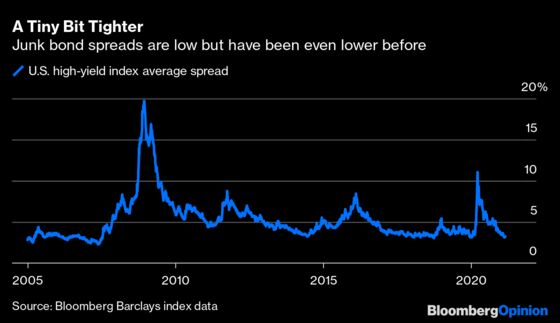

For starters, even if absolute yields look paltry, speculative-grade bonds have had tighter credit spreads in the past. In May 2007, the average spread on the Bloomberg Barclays U.S. High Yield Index was just 233 basis points, an all-time low. There’s another 90 basis points of narrowing to go from current levels to take out that record.

It’s reasonable to expect investors will reach further for yield in speculative-grade bonds. Already, the yield differential between double-A and single-A rated U.S. corporate debt is near an all-time low, as is the spread between what Citigroup Inc. strategists deem “solid” triple-B securities and those rated single-A. The proverbial juice has been squeezed entirely out of the investment-grade market.

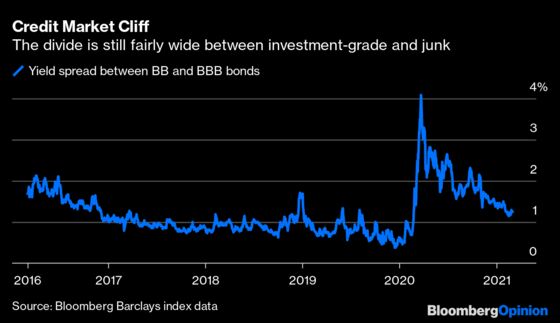

However, there’s still a notable cliff between triple-B and double-B corporate bonds, representing the difference between investment-grade and junk. That gap is 133 basis points — at the end of 2019, it was only 38 basis points, drawing the scrutiny of investors including Jeffrey Gundlach, DoubleLine Capital’s chief investment officer.

Again, if the U.S. is moving into a period of robust economic growth, above and beyond where it was in 2019, this spread could easily narrow further. Perhaps 38 basis points is a bit too extreme (as Gundlach noted), but at the very least fallen angels that are sensitive to economic conditions, like Carnival Corp., Ford Motor Co. and Macy’s Inc., should continue to garner strong demand for their bonds. Meanwhile, higher inflation helps alleviate debt burdens broadly.

Perhaps the clearest sign that high-yield bonds are something of a haven is this: New deals have been off the charts in 2021, and the market hasn’t flinched. Bloomberg News’s Gowri Gurumurthy reported that U.S. junk-bond sales set a first-quarter record on Tuesday and are closing in on the fourth-busiest quarter of all time. It’s all the more impressive given that high-yield funds have experienced three consecutive weeks of outflows that have grown steadily in size, according to Refinitiv Lipper data.

Not everyone is convinced that junk bonds can keep up their hot streak. Bloomberg’s Sebastian Boyd noted that high-yield credit strategy pioneer Marty Fridson, chief investment officer at Lehmann Livian Fridson Advisors, has turned underweight on junk versus investment grade after the latest market swings. Fridson cites the spread between the two as tighter than the level he considers a trigger. Individual investors also appear to be buying the dip in investment-grade, adding almost $9 billion to high-grade bond funds in the past two weeks alone.

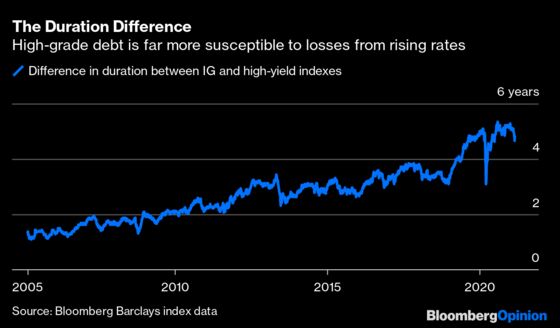

This kind of rotation runs the risk of missing a critical difference between investment-grade and high-yield corporate bonds: their duration, or the sensitivity to a given rise in interest rates. The average duration of the Bloomberg Barclays high-yield index is 3.78 years, lower than the average over the past decade. By contrast, the average duration of the investment-grade index is 8.59 years, just below an all-time high. The difference between the two is almost five years, close to the widest differential ever amid a growing chasm over the past two decades.

To put it bluntly, this chart indicates that investment-grade corporate bonds will get clobbered relative to junk debt when Treasury yields rise. That’s exactly what has happened: High-grade securities have lost 3.2% in 2021 while high-yield ones are up 1%. The key point: These losses have mounted even though investment-grade spreads have tightened to near-record lows. In the current market, duration risk needs to be top-of-mind for fixed-income investors. It’s certainly part of the reason floating-rate notes (with virtually no such risk) are growing more popular.

This kind of duration-inspired rout is precisely what the “Sherman Ratio,” which I called the bond market’s scariest gauge in January, was warning about. At the time, it was still anyone’s guess whether interest rates could take off from their suppressed levels. While longer-term Treasury yields are lower than their peaks from last week, Wednesday’s lurch higher suggests the shakeout isn’t over just yet.

That makes junk bonds, with their comparatively short duration and still-somewhat-lofty spreads to investment-grade debt, look like a potential way to escape the whipsawing trade in Treasuries. Of course, if higher rates take a toll on risk assets as they did in late 2018, speculative-grade debt won’t be immune — the iShares iBoxx High Yield Corporate Bond exchange-traded fund fell the most in five months last Thursday as equities tumbled.

But if the storm is confined to Treasuries, high-yield looks as good a place as any in the bond market to take shelter.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2021 Bloomberg L.P.