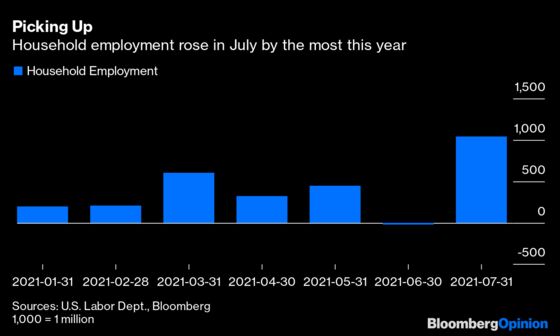

The Most Important Number of the Week Is 1.04 Million

(Bloomberg Opinion) -- President Joe Biden went on television Friday to declare that the better-than-expected 943,000 gain in jobs during July shows that his economic policies are working. Regardless of whether that’s true, Biden was selling himself short.

The number that Biden should have touted was 1.04 million, which is the increase in jobs in the Labor Department’s household survey, not the smaller rise in the narrower nonfarm payrolls. The household survey’s showing was its best this year, blowing away the previous high in March by more than 400,000 jobs. The reason this number is so important is because it captures the self-employed and part-timers not included in the broader nonfarm payrolls count.

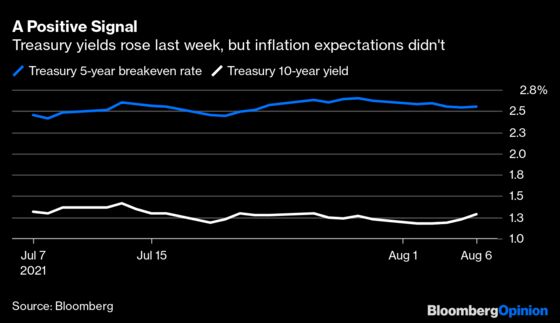

Some economists and strategists such as Ben Emons at Medley Global Advisors credited the household number with moving financial markets, though perhaps not in the way most would expect. Yes, government bond yields rose, capping the first weekly increase in benchmark 10-year Treasury yields since June. But the reason wasn’t necessarily because investors believe the economy is on the cusp of overheating and sparking even faster inflation that the Federal Reserve would have trouble containing.

For proof, consider breakeven rates on five-year Treasury notes, a measure of what traders expect the rate of inflation to be over the life of the securities. Those rates were little changed Friday at 2.55%, some 10 basis points lower than where they ended the prior week and comfortably below the highs this year of about 2.77% in mid-May.

To Emons, the combination of higher yields and lower inflation expectations is a clear indication that markets are pricing in an economy benefiting from higher productivity that supports growth without sparking bigger gains in consumer and producer prices. If true, then higher productivity rates should ease concern that the recent spike in inflation measures is more than transitory. They should also act as a bulwark against the negative economic effects of the rapidly spreading delta variant of Covid-19.

This can be seen in the stock performance of smaller companies, which have underperformed in recent months because they are perceived to have less safeguards against faster inflation and could take the brunt of any impact that the delta variant delivers to the economy. And yet, the Russell 2000 Index of smaller company shares jumped 0.53% on Friday, three times the gain of the Standard & Poor’s 500 Index.

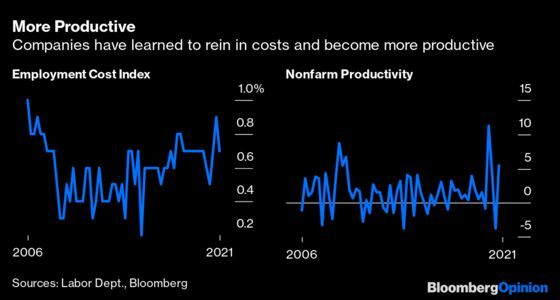

Signs of higher productivity have been there for anyone to see, as my Bloomberg Opinion colleague and economist A. Gary Shilling has pointed out. From the second quarter of 2020 to the first quarter of 2021, labor productivity in the nonfinancial corporate sector jumped 5.3% while hourly compensation rose just 2.0%. Real, or inflation-adjusted, gross domestic product is rising faster than payroll employment. This means that businesses are offsetting gains in employee compensation in part through the lower overall labor costs that come from enhanced productivity.

The economy has seemed to defy conventional wisdom at every step during the pandemic. Did anyone really expect that the worst recession since the Great Depression would only last two months? Did anyone really expect corporate profits to return to record levels as quick as they have? Or the stock market’s performance? So is it crazy to think that the huge gains we’re seeing in jobs won’t translate into higher secular inflation rates because companies have been forced to become more productive? Crazier things have happened.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.