(Bloomberg Opinion) -- July’s surprisingly strong consumer price data may raise understandable fears that inflation is making a comeback. After all, the Fed is aggressively supporting the economy, Congress has allocated trillions of dollars in fiscal relief, and gold has soared to record highs.

But what's really happening is that pandemic-related supply and demand dynamics are distorting price signals in the short term. While we might get hot inflation prints for a few months, we should expect them to get back to normal as production does the same.

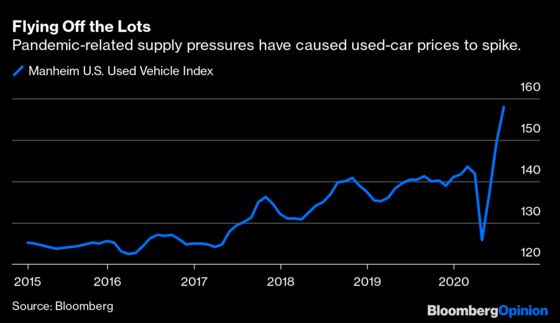

The best example of these dynamics might be in the used vehicle market. Prices of used vehicles, according to the CPI report, rose 2.3% month-over-month in July (they’re still down 0.9% year-over-year). Other measures show prices rising much faster than that. According to Manheim Auctions, the world's largest vehicle reseller, prices rose 5.8% month-over-month in July, and are up 12.5% year-over-year. Auto dealers are reportedly shopping for used vehicles to replenish their supplies, and online used car dealer Carvana Co. noted in its earnings call last week that a shortage of vehicles was hurting performance.

This doesn't mean America is turning into a hyperinflationary failed state where people trade cash for used cars to maintain their purchasing power. Rather, supply and demand for vehicles both crashed in March and April as consumers sheltered in place and factories shut down, and demand has come back faster than supply. For a while auto dealers had enough excess supply to handle that. But as demand continues to normalize while supply lags somewhat, the result has been dwindling inventories and higher prices as dealers scramble to find vehicles to sell to buyers.

A more unusual example of pandemic-related supply shortages is the nation's coinage supply — quarters, dimes, nickels, and pennies. If you've frequented any businesses lately that often transact in cash, you may have noticed signs requesting or requiring exact change because of a coin shortage. The Federal Reserve even recently put out a notice about the situation. It partly stems from bank closures, making it harder for businesses to restock coins after they've paid out change to customers. The country has enough coins to meet the commercial needs of businesses and consumers; the issue is merely one of distribution due to temporary changes brought about by the pandemic.

But not every industry is struggling to match production to demand, which is reason to believe whatever inflation pressure the economy experiences in the short term should abate over time.

Oil remains well-supplied on the global markets; and in fact producers are supplying less than capacity because demand remains depressed due to the pandemic. The price of oil is still down 20% year-over-year. If prices were to rise because of an uptick in oil demand, then the market would be able to supply millions more barrels per day to meet that added demand.

Markets being out of balance is never a good thing, but there are silver linings in some of these production shortages. To the extent we're undersupplied in used vehicles or other markets due to demand recovering more quickly than supply, it means we can count on future production, and the jobs to support that production, as factories reopen and inventories get rebuilt. We've seen some signs of that in recent manufacturing surveys.

And to the extent we've seen large short-term price increases as inventories dwindle, it might mean we'll see a reversal of some of those price increases in the future, lifting consumer buying power later this year or in 2021.

Ultimately, we should be confident any inflation we're experiencing right now is temporary. If Congress or the Fed ends up overdoing it with fiscal or monetary stimulus, then we should be able to see that reflected in the data. It’s something to watch out for, but not a real worry at the moment.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He has been a contributor to the Atlantic and Business Insider.

©2020 Bloomberg L.P.