JPMorgan Braces for 450% More Pain from the Coronavirus

(Bloomberg Opinion) -- Last week, JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon gave shareholders his perspective on the coronavirus pandemic and its impact on the U.S. economy. “We assume that it will include a bad recession combined with some kind of financial stress similar to the global financial crisis of 2008,” he wrote.

The biggest U.S. bank backed up Dimon’s outlook with some staggering numbers on Tuesday.

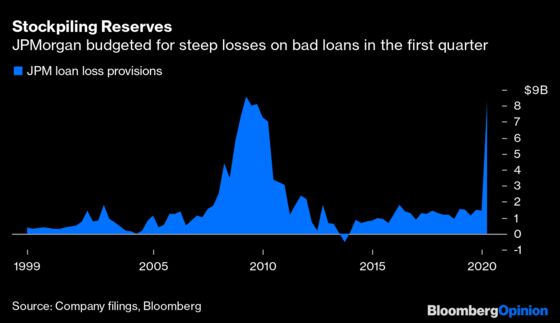

Most prominently, JPMorgan reported a jaw-dropping first-quarter provision for credit losses of $8.3 billion, which compared with the same period in 2019 represents a $6.8 billion increase in dollar terms or a 450% jump in percentage terms. It’s understandable now why Dimon evoked the specter of the 2008 crisis last week — the amount set aside for bad loans is just shy of the bank’s record $8.6 billion at the beginning of 2009.

That kind of headline number sent shockwaves through the rest of JPMorgan’s earnings figures: First-quarter profit dropped for the first time since the end of 2017, to the lowest in more than six years. The bank cut its full-year estimate for net interest income to $55.5 billion from $57 billion. It expects net reserves to build even further in the current quarter, which of course started with much of the U.S. economy shut down.

These are huge expectations for losses, especially considering that JPMorgan’s economic outlook, as detailed by Chief Financial Officer Jennifer Piepszak, is for the unemployment rate to rise “above 10%” and then recover. At this point, it’s very much an open question whether those assumptions will hold. Bloomberg Economics noted last week that jobless claims point to a 15% figure in April “and possibly higher later in the quarter unless the torrent of jobless filings starts to subside.” As each day goes by, that seems increasingly unlikely.

If there’s a silver lining, it might be that JPMorgan can afford to be conservative on setting aside reserves while also extending billions of dollars to companies in crisis because it profited from the unprecedented financial-market volatility in the final weeks of the quarter. The bank brought in $7.23 billion from trading stocks and bonds, the most on record.

JPMorgan also appears to be doing right by its staff. The bank said it’s paying branch employees normally even if they’re working less and will pay up to $1,000 to eligible employees. During a period in which weekly initial jobless claims began smashing through previous records, it’s encouraging to see that Dimon’s famous “fortress balance sheet” is helping to support employees closest to the front lines.

I wrote three months ago that JPMorgan was the king of Wall Street but that it would have a hard time topping its results from 2019. It goes without saying that transitioning from record annual earnings to weathering a controlled economic collapse was not on anyone’s radar.

Early indications suggest that preparing for the worst won’t be limited to JPMorgan. Wells Fargo & Co. also reported first-quarter earnings on Tuesday, setting aside $4 billion for losses on loans and debt, up about 373% from $845 million a year ago. It said it would make a one-time cash payment to roughly 165,000 employees this week. Meanwhile, Wells Fargo Chief Executive Charlie Scharf detailed steps taken to support customers, such as suspending residential property foreclosure sales and deferring or waiving fees. Just because the economy has weakened doesn’t mean the competition for market share is any less intense among the biggest U.S. banks.

Obviously, Wall Street can’t withstand the economic shutdown forever. JPMorgan’s Piepszak warned of potentially “meaningfully higher” provisions for potential loan losses in the months to come because of the coronavirus pandemic. It should be little surprise that one of the main topics of Dimon’s letter last week was that Americans “need a plan to get safely back to work.” The bank’s results look fine in the context of a short-lived spike in joblessness — but what about a longer-than-expected shutdown, with a 20% unemployment rate?

“We know we can handle really, really adverse consequences,” Dimon said on a conference call with analysts. Anything the bank can do to help the country move forward leaves everyone better off, he said. “If we lose a little bit more money in the meantime, so be it.”

If anything, JPMorgan’s earnings at least affirm that this crisis — dubbed the “Great Lockdown” by the International Monetary Fund — is different from 2008. The banks are comparatively well-positioned to absorb body blows from multiple directions and still come out standing.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.